All midcaps are under pressure , Sterlite is not alone…

Q3 FY19 Earnings call scheduled on 24th Jan 2019.

1c16cfb0-4fef-471a-ac5b-a390637fef6b.pdf (390.1 KB)

1 Like

Compelling arguments about the limited real world uses of 5G. While limited inside use is a hinderance, 5G could really bring competition for last mile fiber connectivity. Whether Jio will finish last mile fiberization to 1100 cities before 5G actually becomes a reality remains to be seen. Given the debt on their B/S and idle assets, fiberization is more likely to happen than not.

Even the 5G sites for home broadband will require fiberization, but would save alot of costs for last mile deployment.

“So, mobile gets better latency and the mobile pipe keeps getting fatter. Fixed broadband will get more competition, in some places.”

1 Like

Needing killer apps is one step better. Even without killer app, with 5G, a download can become upto 20 - 100 times faster. If people can download something faster, will they keep quiet and not download anything else. No. On the contrary they shall download many more things they like. So, just a 5G connection shall make the demand for bandwidth explode. Killer apps shall provide the next explosion. Leave alone autonomous cars. Multiplayer gaming/eSports and remote assisted surgeries which shall emerge quickly and shall be real killer apps which need ultra low latency and very fat pipes. And for Ster Tech, the world is the market where these killer apps and many more shall emerge much quicker.

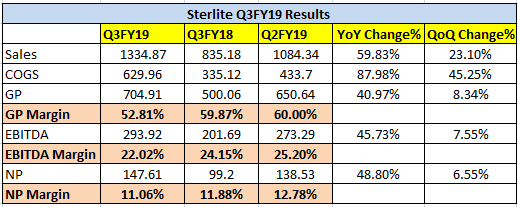

Q3 FY19 results

2 Likes

There is some hit in margins (lower fiber prices as indicated in last few posts) , but I guess that should have been priced in by the market.

I received following note from my broker

· The company has reported revenues at ₹1,335 crore, a growth of 60% over Q3-FY18 .

· The EBITDA for the company stood at ₹304 crore at 22.8% in Q3-FY19 against 25% insame quarter previous year.

· PAT margins stood 10.9% at ₹146 crore in Q3-FY19 against 10.8% at ₹90 crores inQ3-FY18.

· The company’s order book stood at ₹10,231 crore.

· Over all the results are slightly better than our estimates.

1 Like

Just on the concall.

The lower margins are because the service component is higher in this component which has a lower margin. Nothing to do with fiber prices as the company has nothing to do with the spot prices. And they will not catch up on the upside or downside of the spot prices atleast till 2020 end, till their current orders are fully executed.

2 Likes

I was able to attend Q3FY19 earnings call. Below please find my notes. Please verify numbers with the recording as I may have gotten some numbers incorrect.

Concall Notes from Q3FY19 – 1/24/2019

• Expansion plan for optical fiber cable (35mn fkm) to come on board by June 2020.

• Order book stands at 10,231cr.

• Growth has largely come from services business this quarter. Hence, lower EBITDA margin at 23%.

• Revenue split this quarter; Service is ~30% and Product business ~70%. 60% domestic and 40% international.

• Utilization rate at 100%. Order book split remains at 50-50% for services and products.

• China mobile is the largest consumer of optical fiber (30% of the world demand). Tender delayed to current quarter from last November. Postponement has been dampener in market sentiment of prices. Sterlite has been insulated because of long-term contracts.

• 40mn commissioning done for OF. By June 50mn expansion should be done.

• 18mn OFC capacity – running at 100% utilization.

• OF pricing was always close to $8 range. Now it’s coming close to $7.5

• COGS is higher on services business.

• Should be able to maintain 22-23% EBITDA margin.

• Overall demand of OF coming in more than 500mn at global level.

• Current debt stands at 1800cr. CAPEX has been 750cr for current FY.

• Total capex 1500-1600cr + sustainable capex. 80-100cr of sustainable capex.

• Still Sterlite is the only player in India having preform capability.

• Services business will have higher WC requirement than products business. So far no pressure on services work payment.

10 Likes

Usually I have seen OEMs make higher margin on services and lesser on actual product. How come its opposite for these guys ?

1 Like

Strong performance as expected. Road till 700cr annual profit by next year is clear provided strong order book of 10,200cr. Overhang of pledged shares and lower spot prices continue on the stock price.

I also got similar thought, I have knowledge in optical networking industry and services are seen as value addition but don’t have much margins. For example a software update for the network device can be charged to customer, but will be offered near to free to win new device and cable volumes, but in future services will attract more revenues when physical networks are fully deployed, so it’s an important segment.

3 Likes

2 Likes

The results have been fantastic. But stock has lost 10% after that. Is there something wrong in the fundamentals or a change behind this fall? Request for your opinion.

Looks like Sterlite Technologies is being treated like a commodity. China Fiber Optic uptake for for next 6 months is going to be damp.

Sterlite does not sell at spot prices, and they have a good order book of 12K crores. There are not too many suppliers of Fiber optic, unlike say a commodity chemical. Inspite of being a “Speciality Commodity”, it’s trending down. I would be willing to wait and see how low it goes and be a buy (Disclosure: Invested from 265)

hi ,

I think such kind of messages do not create any value.

If one is confident about the company prospect , he would be more happy to buy at lower prices and would expect the prices to fall as much as it can to load it up.

If one is having trading position or want to book out or speculating , he may be more worried with daily movement of prices. This forum encourages more of investing and less of speculation. Even if it is about trading/speculation , one should back it with charts so that it may create some value.

Disc: No Holdings , No Interest

3 Likes

Is there any update on pledged shares in the concall…?

I do understand your point. Reason behind the post was just to know if some change in fundamental which I have missed.

The Management clarified that the pledge is taken for delisting of promoter group company from LSE. Which based on below article has been done. Not sure how long will it take them to repay the loan -

The reason for Monday’s downfall: