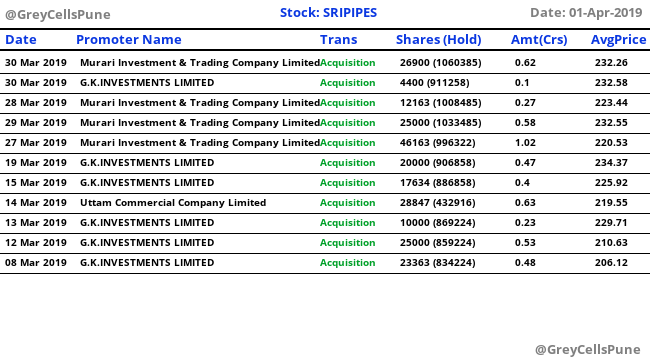

This means promoters(electrosteel group) have pledged their holdings in srikalahasti pipes in order to get limits from the banks , which means if the group is not able to fulfil their obligations the lenders would sell the shares to the tune of 15% of their 41% holding… Rest pledge is non-disposable

1 Like

It seems Srikalahasthi’s balance sheet has been used for Electrosteel Castings Ltd (ECL) bullet debt repayment in FY19.

-

ECL had around Rs 700cr debt repayment in FY19 (Source AR FY18) (Total Debt Rs 1750cr)

-

What was puzzling in September balance sheet is now getting partly clear. Loans have been extended to ECL. As per Jan 2019 ECL’s credit rating report, ECL has received ICD of Rs 250cr.

-

ECL had infused Rs 140cr (Pref allotment at Rs 28.8/share) (August 2018), ICD of Rs 250cr and term loan of Rs 150cr. Above has been used to refinance/payment of bullet payment of Rs 700cr. Recently entire promoter holding of ECL has been pledged, while Srikalahasthi had 34% pledged.(27th March 2019)

In summary, it seems Srikalahasthi’s balance sheet has been “leveraged” by ECL for its bullet repayment. More clarity would be helpful.

4 Likes

I had analysed SriKalahasthiPipes in Dec 18 and at that time it was not Pledged (Source for Pledging Information - Screener.in). Did the pledging Happen after that?

decent set of results

The profit before tax for the quarter ended 31st March was Rs.47,43 crores as against Rs.45.91 yoy

The profit before tax for the year ended 31st March 2019 was Rs.160.05 crores, as compared to

RS.200.93 crores in the previous year ended 31st March 2018.

The Profit after tax for the year ended 31st March 2019 is Rs.117.54 crores as against Rs.147.40 crores in the previous year ended 31st March 2018

lower profitability due to higher RM costs- coking coal, iron ore ; depreciation of rupee vs dollar

implementation of 55 crores Ferro Alloys project initiated during the year is as per schedule and the first furnace will be commissioned by September, 2019 and the second furnace by December, 2019.

ductile iron capacity being extended from 3,00,000 to 3,50,000 TPA by fy 21.

2 Likes

I think highlight about the results is that balance sheet has gotten significantly better since september 2018. Loans and advances have come back to the company and receivables gone down again and Cash balance back up

5 Likes

4 Likes

Rahul Rathi of Purnartha PMS had once mentioned in an interview that they conducted a study and found that companies which have marker cap <= Operating cash flow of last 7 years are most likely to be profitable investments. So I ran following query and found Sri Pipes in the list.

Market Capitalization <= Operating cash flow 7years AND

ROCE3yr avg > 15 AND

Average return on equity 3Years > 15

The operating cashflow from 7 years is 973 with market cap at just 820 crs.

The valuations look attractive in terms of other statistical parameters as well.

PE at about 7 which is slightly lower than 8 year avg.

PBV at 0.65 vs 8 year average of 1.3!

Return ratios look good too.

However, this is just an at a glance statistical snapshot which just indicates that this business should be evaluated in detail.

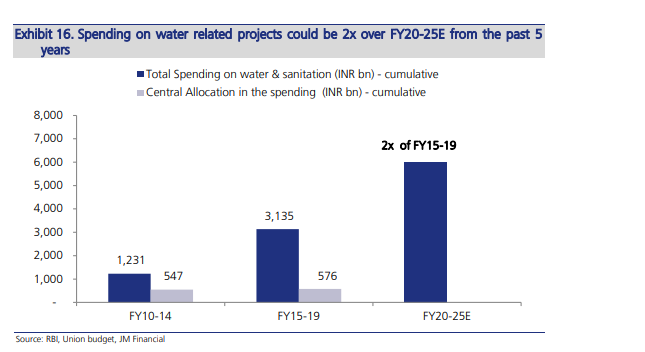

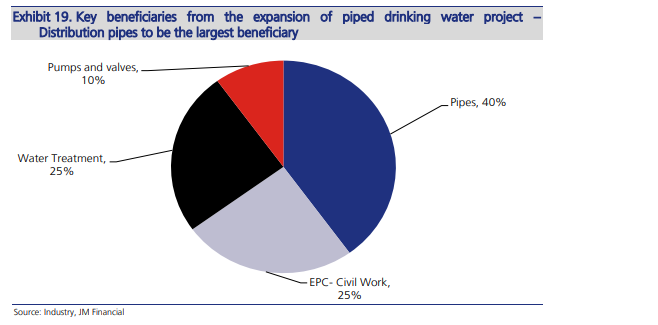

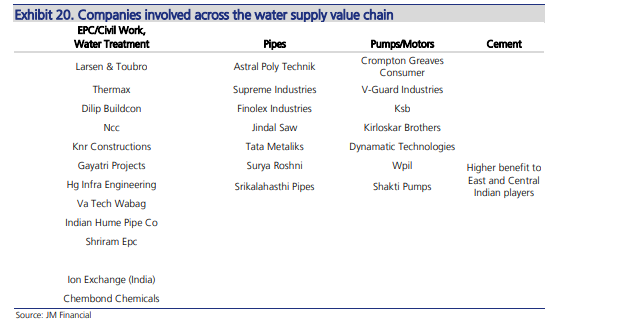

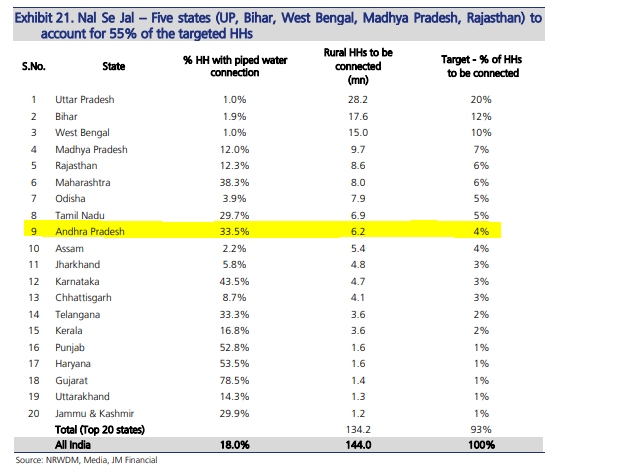

I was trying to see if the company could be beneficiary of “Nal Se Jal” program of government which aims at doubling the spending on water supply. I found following report which gives good idea about the scope and possible beneficiaries. However, the major beneficiary states seem to be Eastern and Northern parts of India as Southern India seems to have higher connectivity already with AP having 33% households having tap water. Following are some highlights.

For those who are following this business, I have few questions.

- Which are the major states in which Sri Pipes supplies?

- Do you think Sri Pipes is in the position of being beneficiary of this initiative?

- The issue of some loans forwarded by the company, is it still an issue and how crucial?

Disc.

Not invested, evaluating

7 Likes

Another stellar quarter.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/3e572881-6005-4d73-bc4b-a66dc9699a27.pdf

1 Like

Pretty good results given the stock price…margins back to 15%…infact its surprising to see the beating that has happened here.

Both Tata Metallik and Sri kalahasti seem to be optimistic about the demand and expanding capacities materially given the government’s focus on water.

2 Likes

@ayushmit

Any idea why the Pig iron spreads troubled Tata Metaliks, so much more than they did Srikalahasthi?

Pig Iron contributes 58.21% for Tata Metalliks. The Company operates two business segments- foundry pig iron and DI pipes. Tata Metaliks is one of the India’s leading manufacturer of foundry grade pig iron.

https://www.tijorifinance.com/company/tata-metaliks-limited#revenuemix

Pig iron is just 0.55% of revenue mix of SRIPIPES. Srikalahasthi Pipes Ltd is one of the leading producers of ductile iron (DI) pipes in India.

https://www.tijorifinance.com/company/srikalahasthi-pipes-limited#revenuemix

1 Like

DI Pipe is forward integration of Pig Iron. As Tata metalliks has excess capacity of pig iron hence some of their fortunes are linked to the inherit volatility of that segment

1 Like

For water supply system…my observation in my municipality area…they are using plastics pipe instead of DI pipes. When I enquired about change, their reply was it is due to corrosion they switched to plastic pipes

1 Like

DI pipes offer a life time of 50 to 60 years. Doubt the reason for change to plastic pipes. SPL has delivered good results. Expansion plan looks progressive and market demand depends on new AP govt.

1 Like

Does anyone know if the loan given to ECL has come back? The pledge was created to forward the loan to ECL which is quite alarming about Corporate Governance of the company. ECL is going through troubles and if this loan is written off then it would mean that funds of Sri pipes share holders have been siphoned off to ECL which is a related party!

1 Like

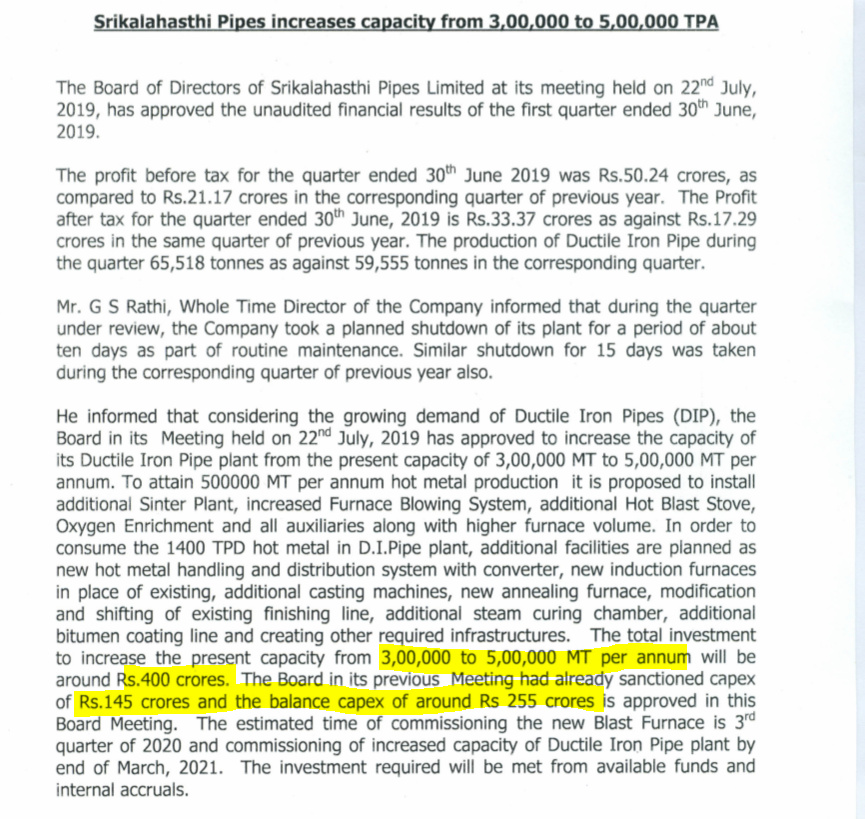

Plans 400 cr capex to be funded through internal accrual. Need to see when they bring down the pledge levels from 31%.

Disc - Evaluating.

1 Like

Check their related party schedule at the year end - appearing as part of BSE announcements - Advance remaining with Electrosteel is 48cr

It does not show any loan given to ECL - means even if it was given, it was routed through an unrelated entity (my speculation). But based on the closing balancesheet, it appears to have come down significantly

Hi All,

I am doing some research in the DI Pipes Industry. I have a query related to the future industry supply. Tata Metalliks, SriKalahasthi Pipes are doubling capacities, KIOCL setting up the capacity.

With demand is growing at 13-14%, will this not create supply glut in the industry in next 1-2 years? Are the big players Jindal Saw, Electrosteel losing capacity which will prevent supply glut?

Requesting views from people who are monitoring the industry for long time. Posting in both Tata Metalliks and Srikalahasthi threads.

Thanks

Mukul

We need to be careful and validate such statement with past history of the promoters. This is an excellent statement ‘investors’ normally likes and that’s why promoters are using such statement. However, we need to verify based on their execution skill, ROCE, existing cash position. Sometime such statement remain as statement if it is used to ‘create positive sentiments amongst investor in bad time!’