Iron ore prices, coking coal and rupees depreciation adding to margin pressures.

Iron ore prices, coal prices continue to be strong, so little respite on that front for next quarter. I hope rupees gets stable going forward.

But overall this is a good company to hold knowing Irrigation, Sanitation is a mega theme to improve the standard of living and farm productivity. Also, valuations are depressed with more than 50% correction from peaks.

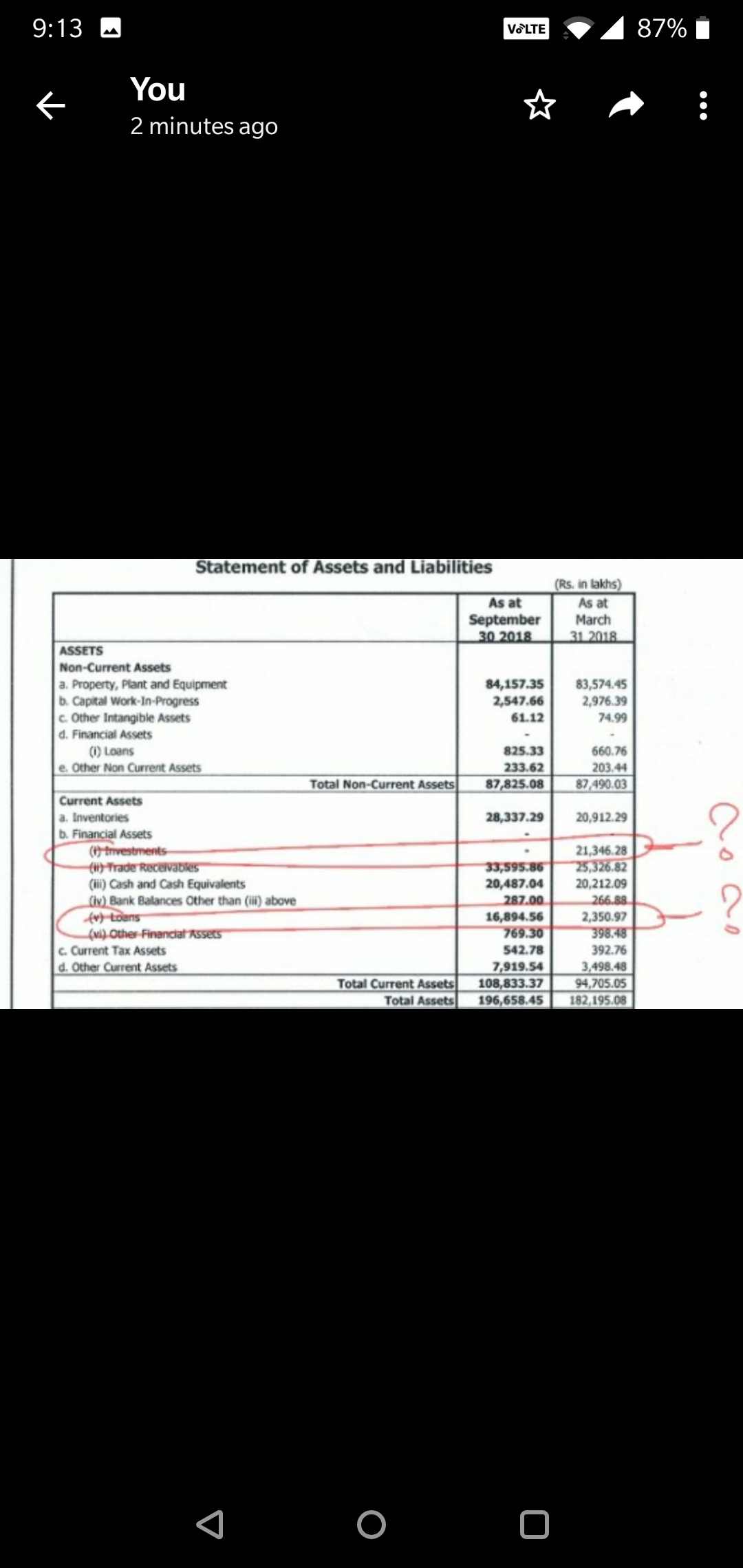

This quarter they have moved money out of current investments and given out loans. I hope they dont squander this money making loans which is completely outside their area of expertise.Think would be better to repay foreign currency loan.

Based on my understanding, the company has liquidated its investments and advanced loan to some entities. While long term loans increased by ~53 crores, the short term borrowings are down by ~170 crores.

The con-call should throw some light on what the management has intended to do here.

But overall, the results seem to be very positive, so unless the management has indulged in some serious malpractice, the stock looks attractive after the recent fall.

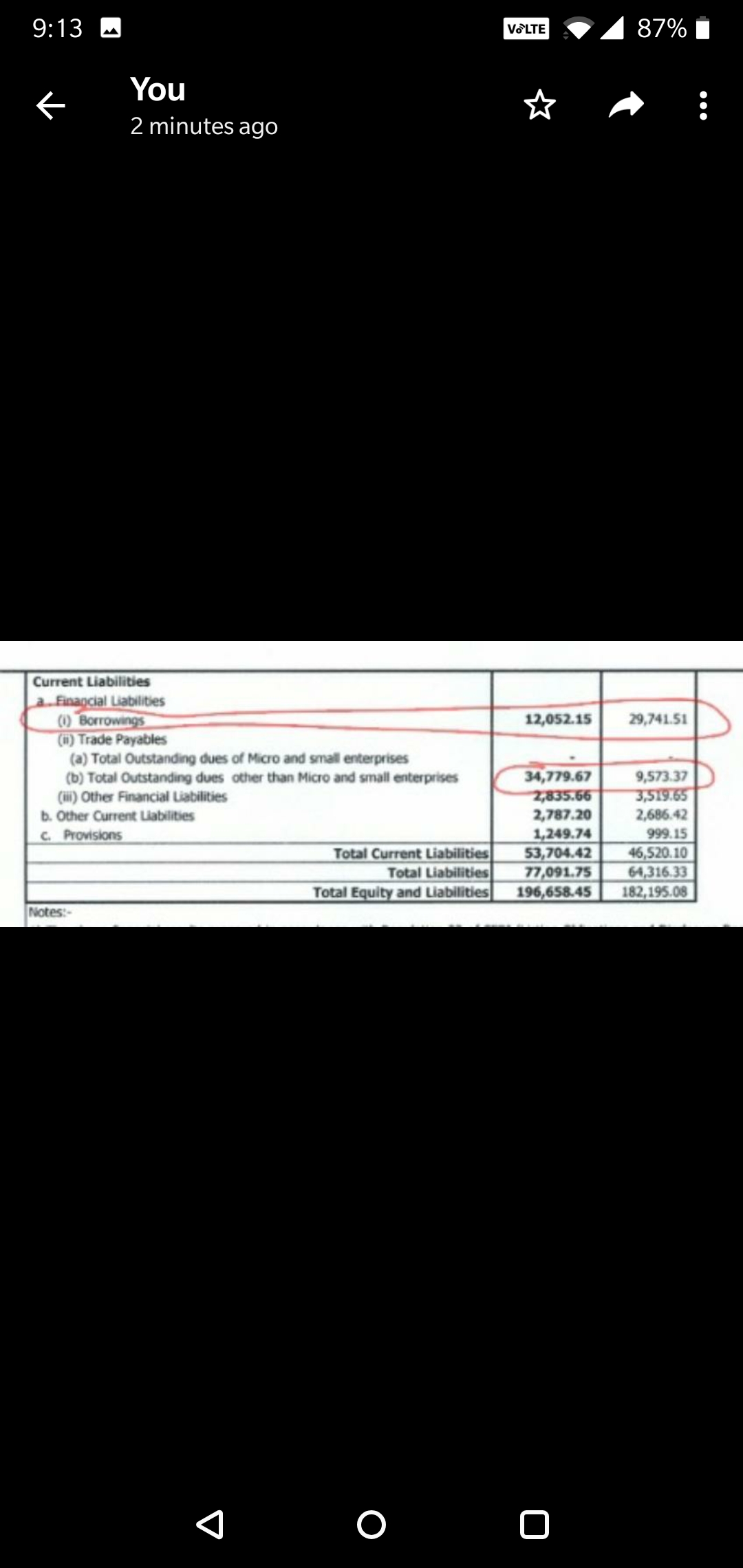

Hope management clarifies. Drop in investment (Rs 213cr to Nil), Spike in Loans (Rs 24cr to Rs 169cr) + Drop in ST Borrowings (Rs 298cr to Rs 120cr), Spike in creditors (from Rs 96cr to Rs 348cr)…Pretty baffling move in Balance sheet.

Disclosure - Invested

I did Analysis on Srikalahasti Pipes and below is a Brief of my Analysis in terms of Positives and Negatives. Please share your thoughts. As of now i am not holding this stock and its in my watchlist Negatives:

Electrosteel Castings, its main holding company which is also into the same business is not doing well.

Equity Share Capital Increased in FY18. This must be because of the QIP @360 because of which 250 Cr was raised

OCF (Operating Cash Flow) reduced in FY18 – This is because Trade Receivables are negative 11000 Cr. As compared to a Positive figure in FY17

OCF reducing from FY17

In FY11, FY12 and FY18 OCF < Net Income which is not good.

Sales have Grown consistently by Net Profits have not grown consistently

Remuneration of Management is 8% of Net Profit.

The Chairman doesn’t hold any stock of SPL but holds 2% of electrosteel castings

There was an Authority BIAS because Dolly Khanna owns it but I have done my Analysis

Positives:

New Entrants, Competitive rivalry, Supplier Power Threat of Substitution. Ease to substitute is not so easy

I see some MOAT exists from Qualitative Perspective.

Overall Debt and Long Term Debt is less and reducing

Reserves are increasing

Cash is Good

Raw Materials % is Decreasing

Net Profit Improved

Operating Profit is Maintained/Increased

The Sources of Investing are coming from Operating.

Company is paying out good Dividend

Operating cash flows are Consistent

Overall Cash flow is good

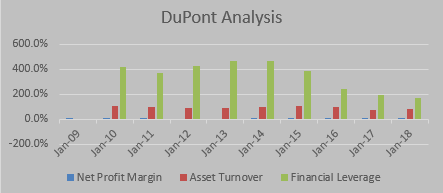

ROE is increasing. The breakdown as per Du Pont is also good except the Asset Turnover.

As per the Less is More checklist this seems to be fit for Long term investment

The Annual Report doesn’t seem to have cover-up’s.

I have been looking at this company on and off for the last few months but have always encountered the same issues (most of which have been mentioned above):

Lack of pricing power. A few large players in an industry is no predictor of pricing power. Further, the threat of smaller players gaining market share is very real especially when contracts are awarded to the lowest bidder. I am vaguely aware of several such ‘unorganised’ players in South India.

Corporate governance worries. The good impression I got from the well-timed QIP has been offset by the deterioration in the B/S over the last 6 months.

Commodity business. While all the cost reduction initiatives deserve merit, everybody in the industry is carrying out the same. Perhaps it is the nature of the business, but I didn’t like how the management was unwilling to quantify the benefits of the ferro alloy plant. On the hopes of a PE rerating, what would the fair value of such a business really be? Does anybody have any thoughts of the margin of safety the current price offers?

My biggest (and really only significant) concern is the sustainability of the tailwind the company is riding on. How predictable are revenues given that the Gov’t may be curtailing fiscal spending soon? I haven’t found statistics relating to how Govt spending trickles down to the DI pipe industry, and am not sure such an exercise would ultimately be useful.

As its just at planning stage, would take a long time (atleast 3 years) to commercialize. At the same time it upholds the hypothesis of limited players and strong demand especially in South

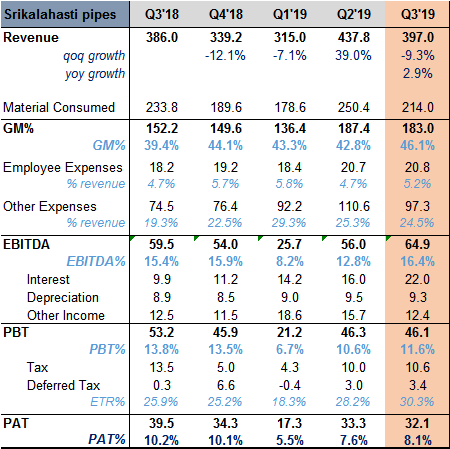

Bad results from Sripipes. Currency move & imports of raw material dented profits . Too much capex going on by the company without getting any benefit for past capex done by them . Significant increase in Interest cost of 7 cr (QoQ) Thats why profits are affected . But sept result mentioned reduction in short term loan by 120 odd cr so why int cost is high . Need to look deeper.

The higher cost for finance could be because of foreign currency debt affected due to rupee depreciation in past quarter .Need to seek more clarity from management .

The gross margins have improved owing to No purchase of stock in trade, Raw material price, despite mentioned in results does’nt seem to be a problem. Only concern here to me is high interest cost of 22cr which the company can improve given their cash balance … Insights Appreciated

In the H1FY2019 results shared by the company, there has been a high increase in the amount of debt (from 384Mn to 917Mn). No reason provided for the increase in debt. Capex perhaps?

The company has advanced ‘Loans’ to extent of 1689Mn (up from 235Mn in FY18). No explanation regarding the nature of such loans

There has also been an increase in the amounts due to micro/small enterprises (up from 957Mn in FY18 to 3478Mn in Q2FY19). No explanation for the increase.

Add to that the company has high interest cost of 22 Cr, which is the prime reason for subdued profits

Unfortunately, the company also has not held any con-call for 2 consecutive quarters now. Definitely some concerning red flags in absence of any information.