SP Apparels_Equirus.pdf (1.8 MB)

Little Old But Good Report of SP Apparels.

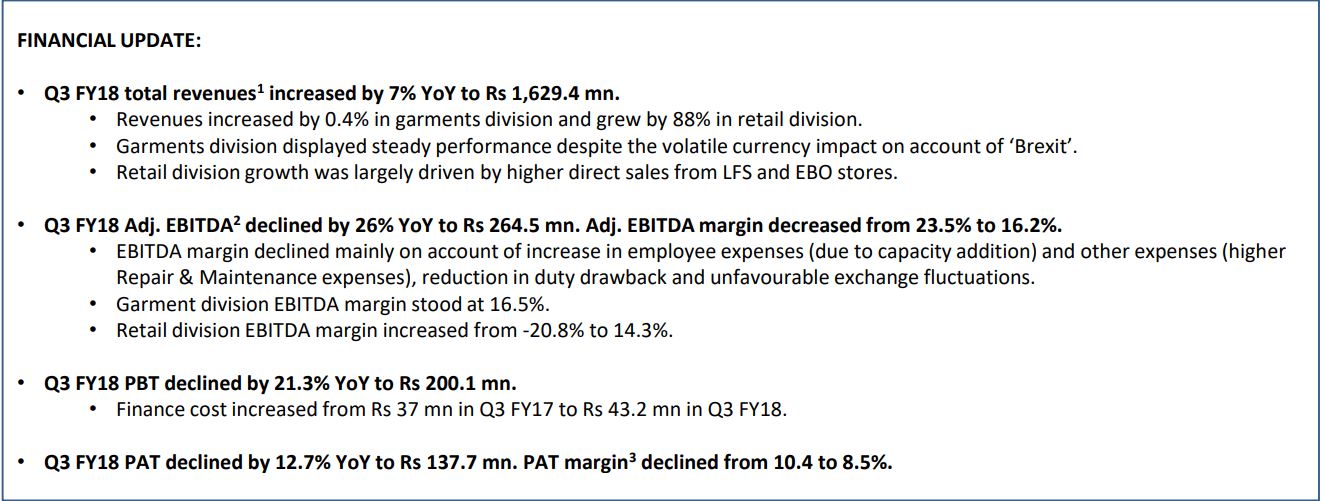

Q3 FY18: Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/39b5c734-e1f2-47c1-84d4-1dc18809c4e1.pdf

Q3 FY18 Investor presentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/eb6ab829-446b-461e-b410-573d0dc7e255.pdf

The turnaround in retail - although on a very low base - looks heartening.

Garments is still a drag both on top line and large one-offs (Repair & Maintenance up 46% YoY) impacting margins. FY19 is going to be a very crucial year for SPAL.

Board meeting for fund raising

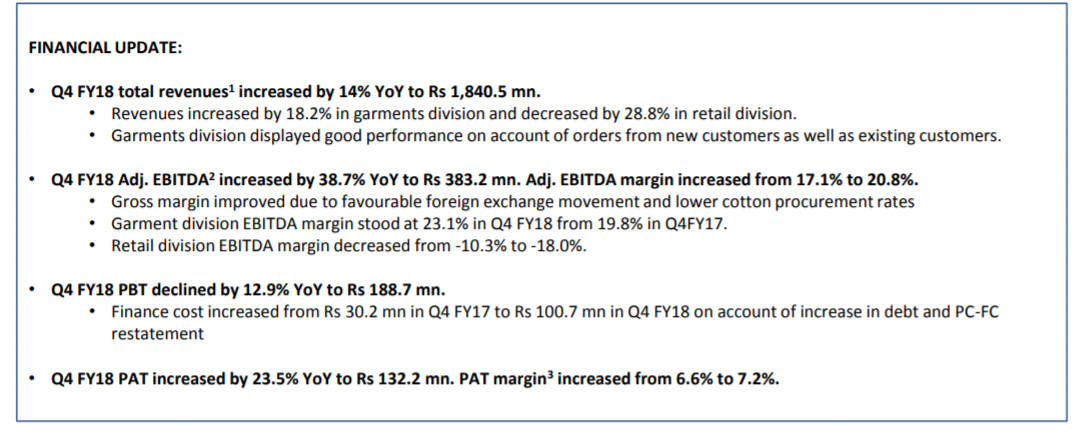

F18 Q4 Results:

Link to Q4 Presentation : http://www.s-p-apparels.com/wp-content/uploads/2016/01/Q4-FY18-INVESTOR-PRESENTATION.pdf

Link to Q4 Conference Call : http://www.s-p-apparels.com/wp-content/uploads/2016/01/Q4-FY18-TRANSCRIPT.pdf

Financial Update:

In Q4FY18, Finance cost grew from Rs.18 Crores to Rs.28 Crores majorly due to PCFC restatement and MTM losses, which have now been reversed. So company is starting FY19 with Rs.10 Crores of credit this fiscal year.

Overall things are looking positive as the company is moving to a stable operational environment.

Thanks for sharing the analysis on Capital Allocation @Prdnt_investor. Since there was no update for long so I thought of reinvigorating the thread. The share price has been languishing in 250-230 range for quite some time and has fallen precipitously from 400 levels. I read yesterday that earlier this year promoters aggresively bought shares worth about Rs 201m at an average of 371 per share. Their holding as of Dec 2018 is 61.60% up from 60.53% as of Mar 2018. Besides Cotton price, brexit and gst what could be the other reason for such a drastic fall while the promoter is still buying. Although the analysis above indicates good quality of business and inst. holding is high including goldman sachs… but after burning my fingers in kitex there is always a fear of this also being a catch 22 situation and a falling knife…

Disc: Invested, thinking of averaging down at Rs230

This is a typical commodity manufacturing with no pricing power what so ever. With higher adoption of robotic workforce in the textile segment, this labor intensive businesses in India, Bangladesh etc also face a high obsoletion risk in the coming future.

Thus it would be difficult for markets to progressively assign a higher PE to these type of businesses going forward. Hence even if earnings recover, stock price may not reclaim previous highs in a hurry, also there are too many people sitting on losses etc. so would face large volume selling at higher price points.

Would also suggest to look into Technical Textiles and the companies operating in that space. That would be a better bet for someone with a 3-5 year horizon willing to invest into Textile sector

The stock has seen quite an uptick from a low of 201 on 29th Jan to a high of 240 today 31st jan. looks like intense buying after a very long time. .Ideally only the changes in earnings or raw material price drives such short rally… But it could be Some HNI buying or brexit or is it the budget effect? Would like to know more.

Disclaimer:Holding… avaeraging down

No specific news other than the news that MFs have increased stake in S.P. Apparels. See below:

The stock has been beaten down heavily and valuation is not expensive (under 12 PE if we annualise H1 EPS). Buying from institutions and HNIs may be driving the stock up. We should also note that the stock is extremely low on traded volumes normally and small buying make take price upwards.

More importantly, we need to watch out for competitive advantage the company carries like Prdnt_investor talked about.

I guess we need to watch earnings trajectory for Q3 and Q4 keenly as Q2 earnings were very good.

Well from 201 odd levels in Jan to 303 levels it touched today, quite a phenomenal run. Thanks to continued MF/institutional buying. Relief to see such a movement… but yeah thanks for your reminder on competitive advantage of textile industry… have to keep that in mind always

Q3 earning was excellent - that might have given boost to the stock

Very Good Q4 Results

Q4 2019 vs Q4 2018

FY 2019 vs FY 2018

This good result of nearly 50% growth in YOY profits & eps has not translated into similar stock price increase, even in a broad based rally of a cheerful market. CMP at 294 is actually a pre-result level… so either heavy profit booking happened by institutional investors /super investors or market does not see a silver lining on the clouds for this company…

yes could be. this kinda of situation also happened with JK paper. last two quarters were great but still market didn’t consider pushing the price higher. is there something we are missing ?

Debt in the book is 201 Cr and total interest paid was only 6Cr. Moreover for the last two quarters interest payment is negative… although while going through the past few years interest payment was around 10% of total debt .any idea regarding such deviation …

This was the reason given in the Q4 presentation,

"Finance cost was Rs 31 mn, offset by reversal & restatement impact of PC-FC.". Can anyone explain what is this ?

PC-FC is Packing Credit in Foreign Currency, this is more like short-term working capital finance available to exporters at internationally comparable interest rates. This article has more details on this topic.

A lot of export credits and other incentives were delayed due to GST implementation, so the offset they mention might be related to this. Overall company seems to be in a comfortable financial position link.

The stock has touched its lowest in 4 years. Profit before tax for the qtr dipped 21% yoy even though revenue has increased. Main impact is due to Finance cost going up from - 16m to 55m, depreciation and ammortization from 59m to 67m, and other expenses up from 426m to 545m as compared to previous quarter. Not sure what constitutes “other expenses” and why it went up so much & same for Finance cost (is it still due to the pc-fc reversal impact as mentioned in Rudra’s post above ) . Can anybody help understand.? Are these temporary issues?

Very good Q2 results - good growth in revenue and profitability back on track.