Guys any update on Solar Inds, it looks attractive now at 625 levels…

Disc. - invested recently

Promoter has also bought the stock from open market few months back.

1 Like

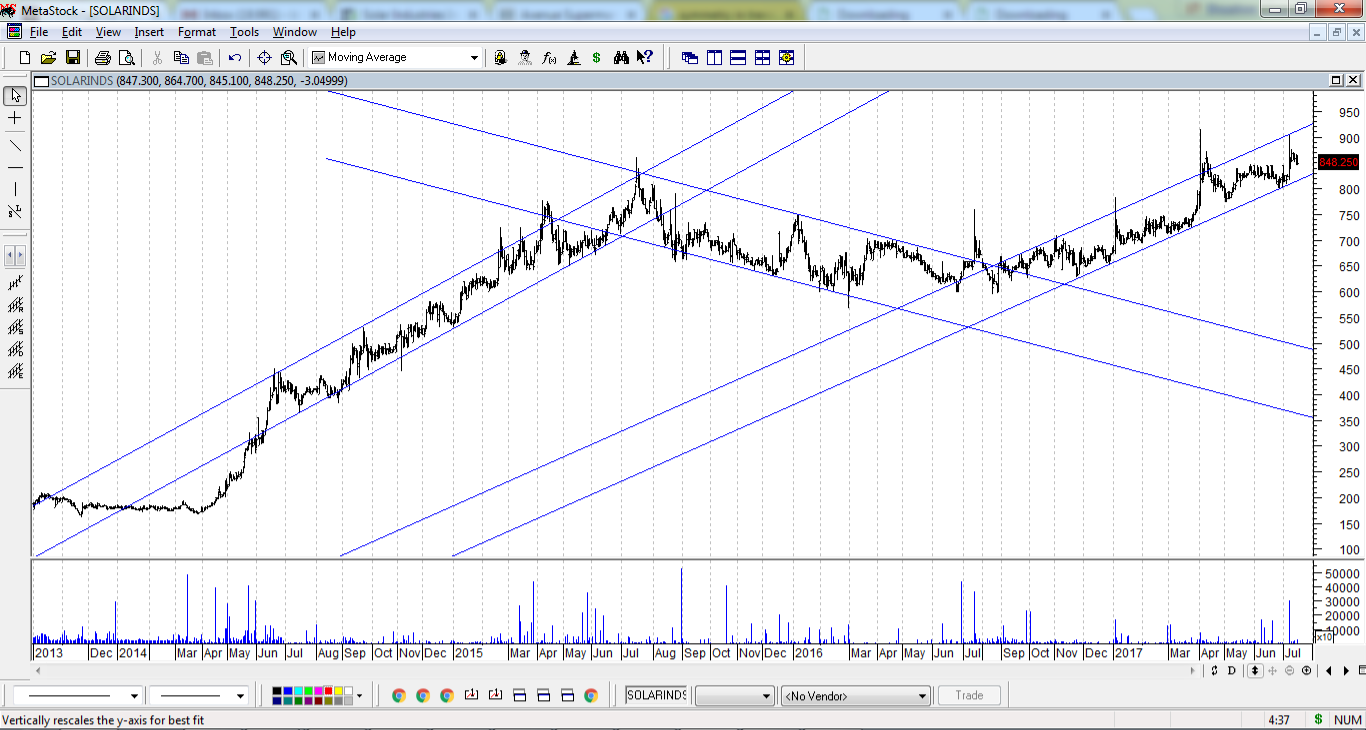

The solar industries chart is a great example of how prices follow an underlying structure rooted in investor psychology. What appears to be random may not be so

Best

Bheeshma

1 Like

Solar Industries India Limited has bagged the running contract for supply of Bulk Explosives to the subsidiaries of Coal India Limited amounting to Rs.1143.63 crores.

http://www.bseindia.com/corporates/ann.aspx?scrip=532725&dur=A&expandable=0

I have noticed this stock is not at all volatile . Hasnt fallen in this ongoing carnage.

Seems like a good buy, but any inputs on valuations ?

This is a solid, low risk, high quality compounder for several years to come.

Adding on every decline, but it never falls enough.

Anyone has membership of this ? full article ?

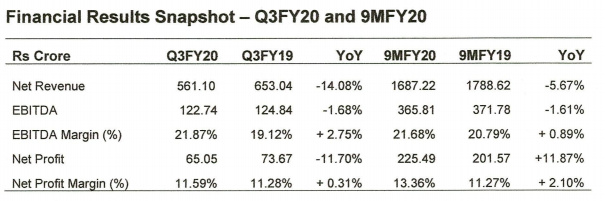

Disappointing Result . Anyone tracking this company ?

Poor quarter

Q3FY20 Results

• There has been fall in commodity prices resulting in lower realisation globally.

• Revenue from Well Sinking, Housing & Infra segment decreased by 24 %

• Revenue from Coal Mining segment down by 18.09 %

• Revenue from Defence decreased by 37%

• EBITDA has improved by 275 basis point i.e 21.87% compared to 19.12%

• Net Profit Margin has improved by 31 basis point i.e 11.59% compared to 11.28%

Management comments:

" Monsoon this year has surprised one & all. It was initially predicted well below normal but finished with excess rains not just for the year but highest in last 25 years. Excess & prolonged monsoons effected mining, infrastructure and well sinking activities. Coal India Ltd. 's monthly production dropped to a record low as the heaviest rains in 25 years flooded mines and hindered shipments.

The fallout from trade tensions across major economies, most notably the US and China, political uncertainties and a slowing Chinese and Indian economy negatively affected global growth, industrial production, market sentiments and our operations in Turkey is a major fall out of that. "

Disclosure: Not invested… tracking the story

1 Like

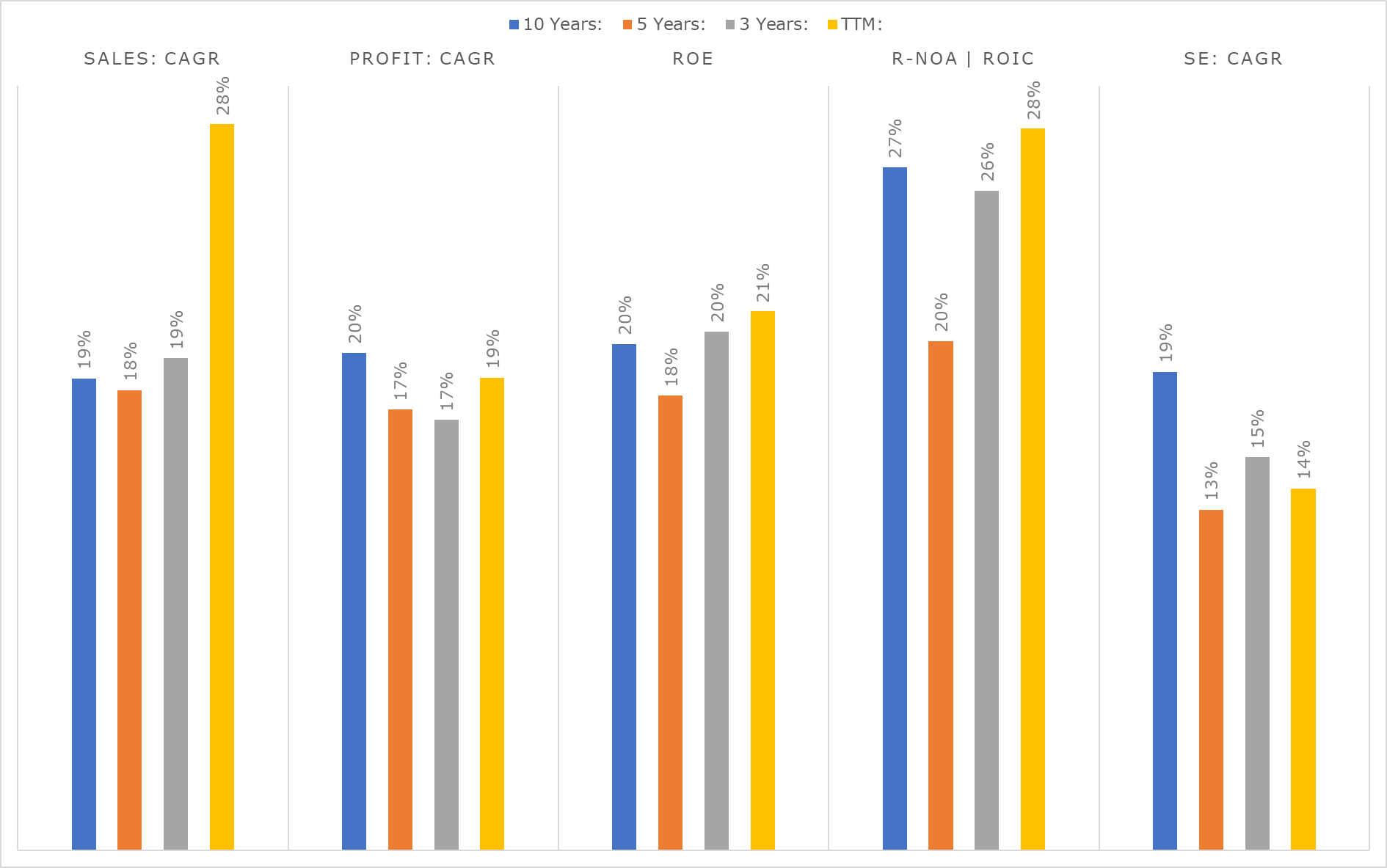

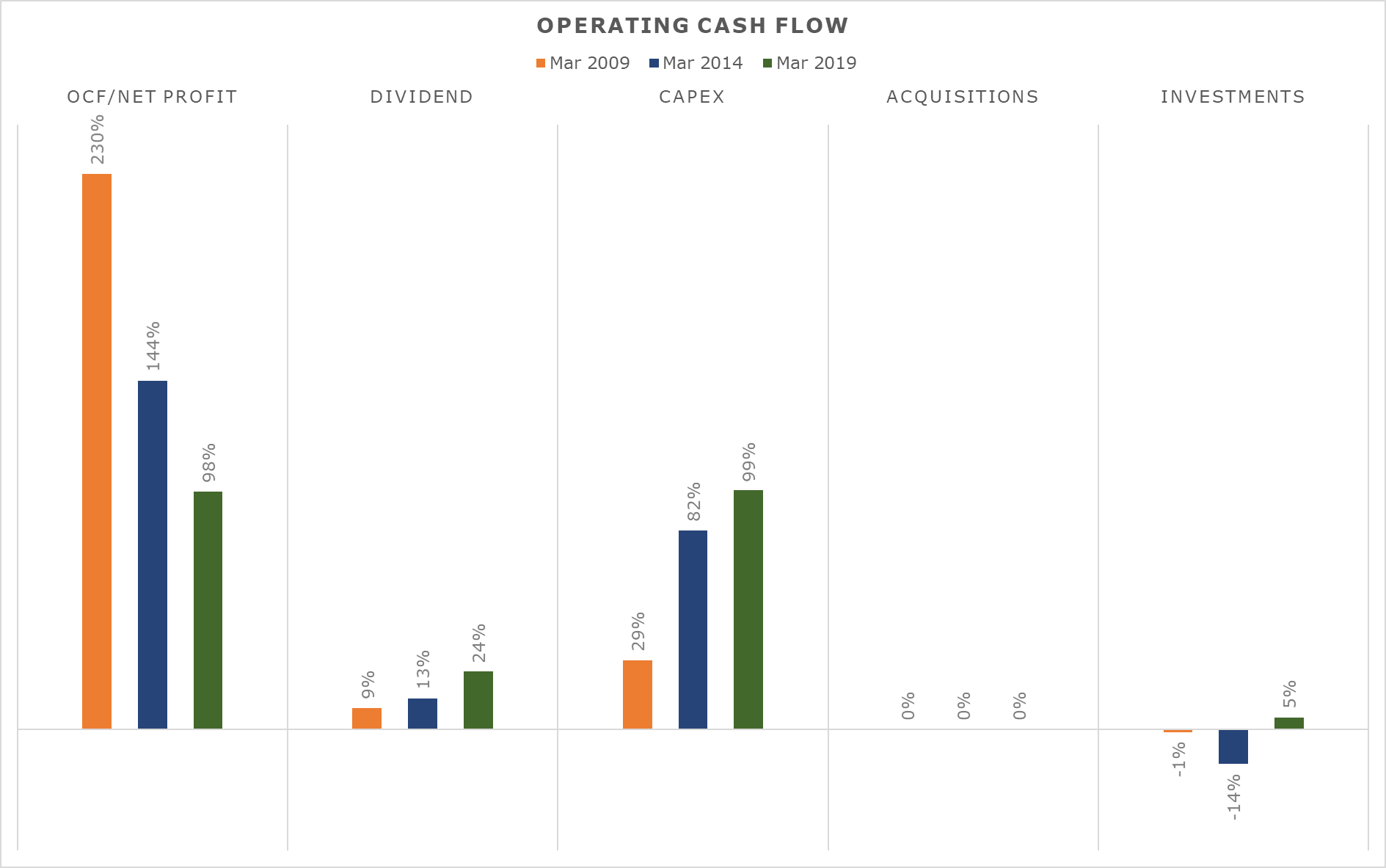

Below image (Consistent ROE with increasing shareholders Equity, Consistent growth in Sales and Net Profits) motivated me to spend time to understand the buisness:

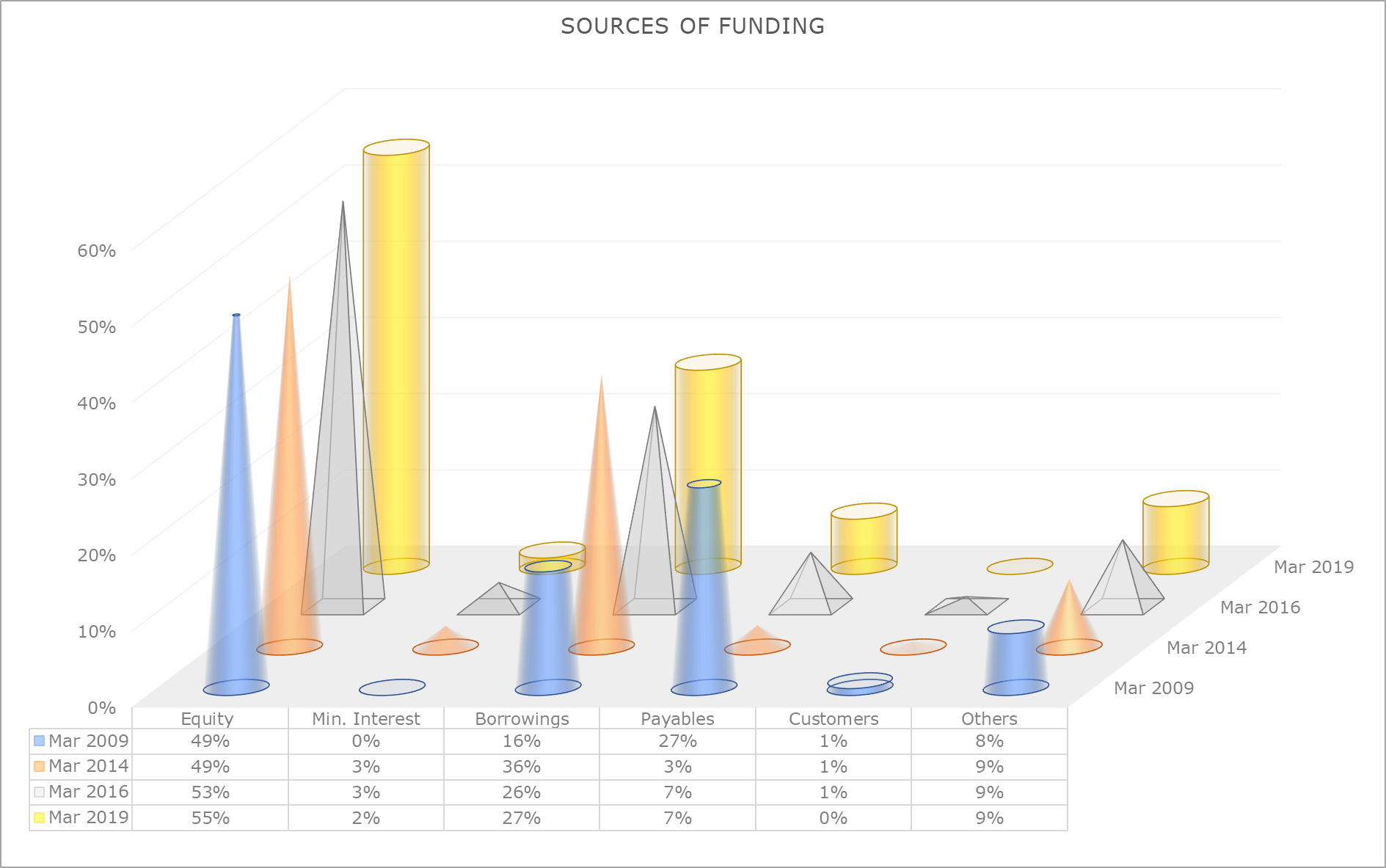

The company is funded as shown below:

The key observation from the above image is the snowballing of borrowings aka financial leverage which ‘MIGHT’ be the key reason for ROE of 20%. Suppliers (evident from Payables %) have the say and hence do not leave much money to enable company’s financing. The case remains the same with customers as well.

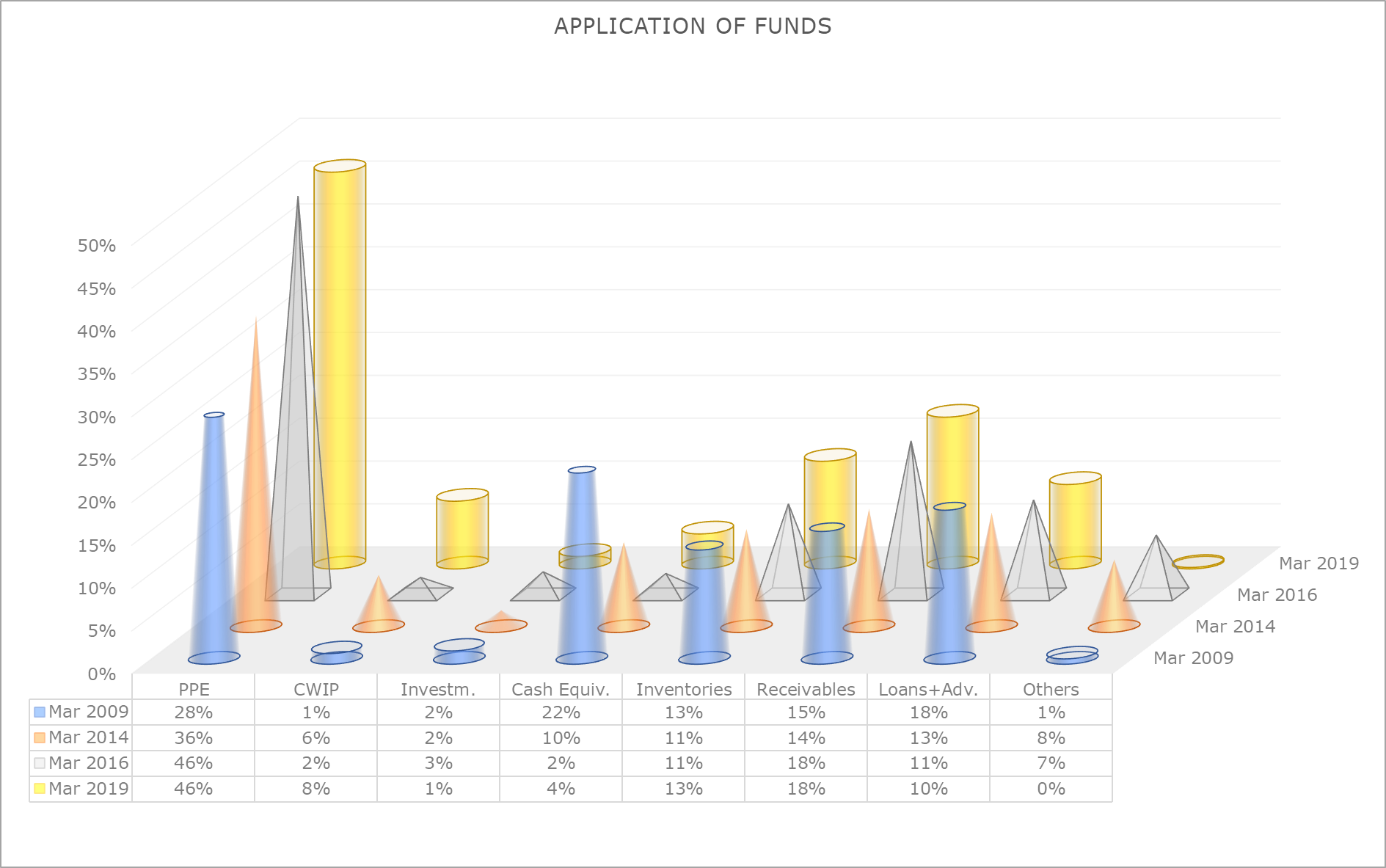

The company has utilized the funds as shown below:

Most of the funds are invested in PPE, Inventories, and Receivables. In the last 5 years, the company has done CAPEX of more than 500 Cr. for orders related to defence opportunity but yet to make any significant progress to sweat these assets.

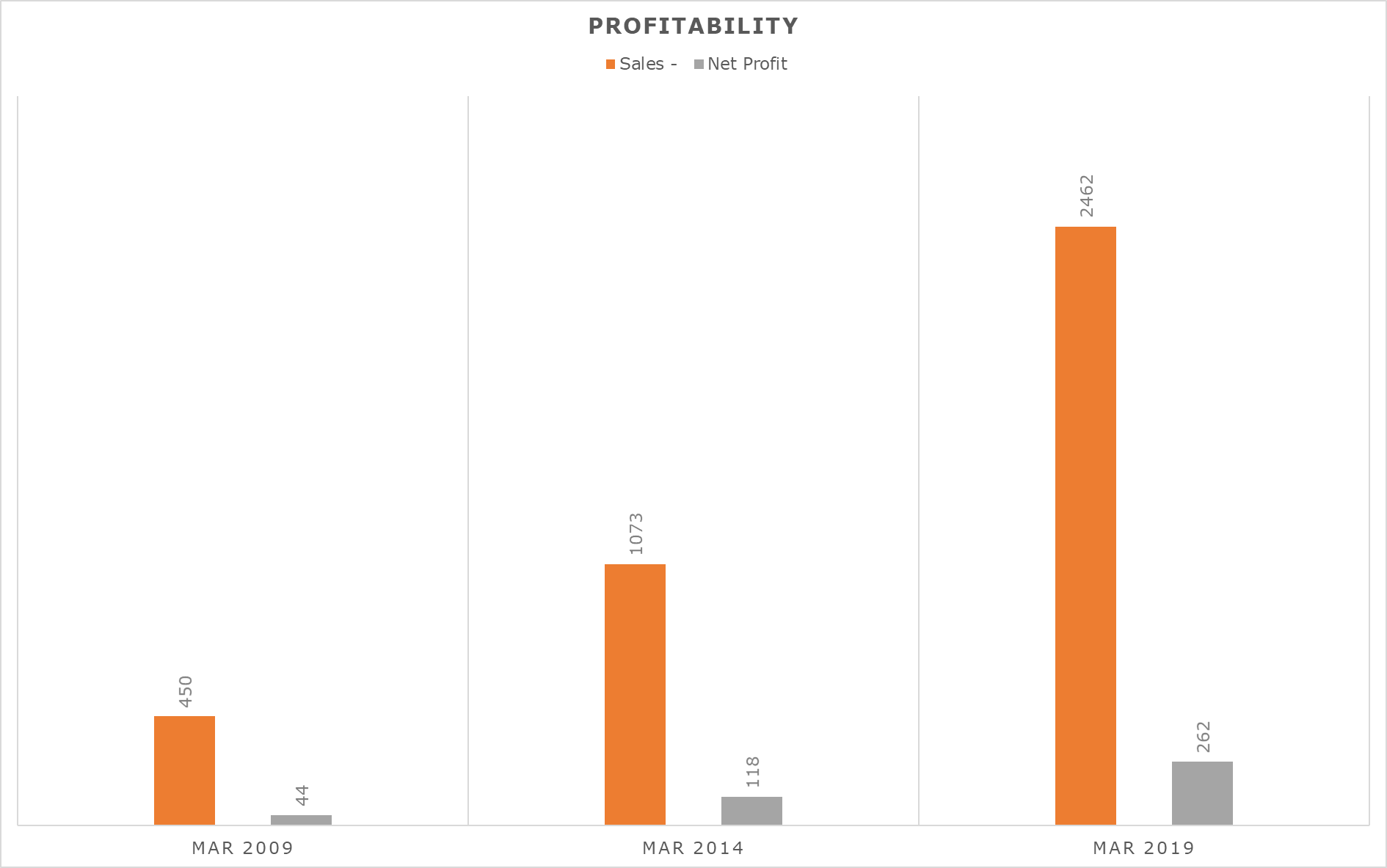

Below snapshots show the profitability parameters of the company over the 10 years period:

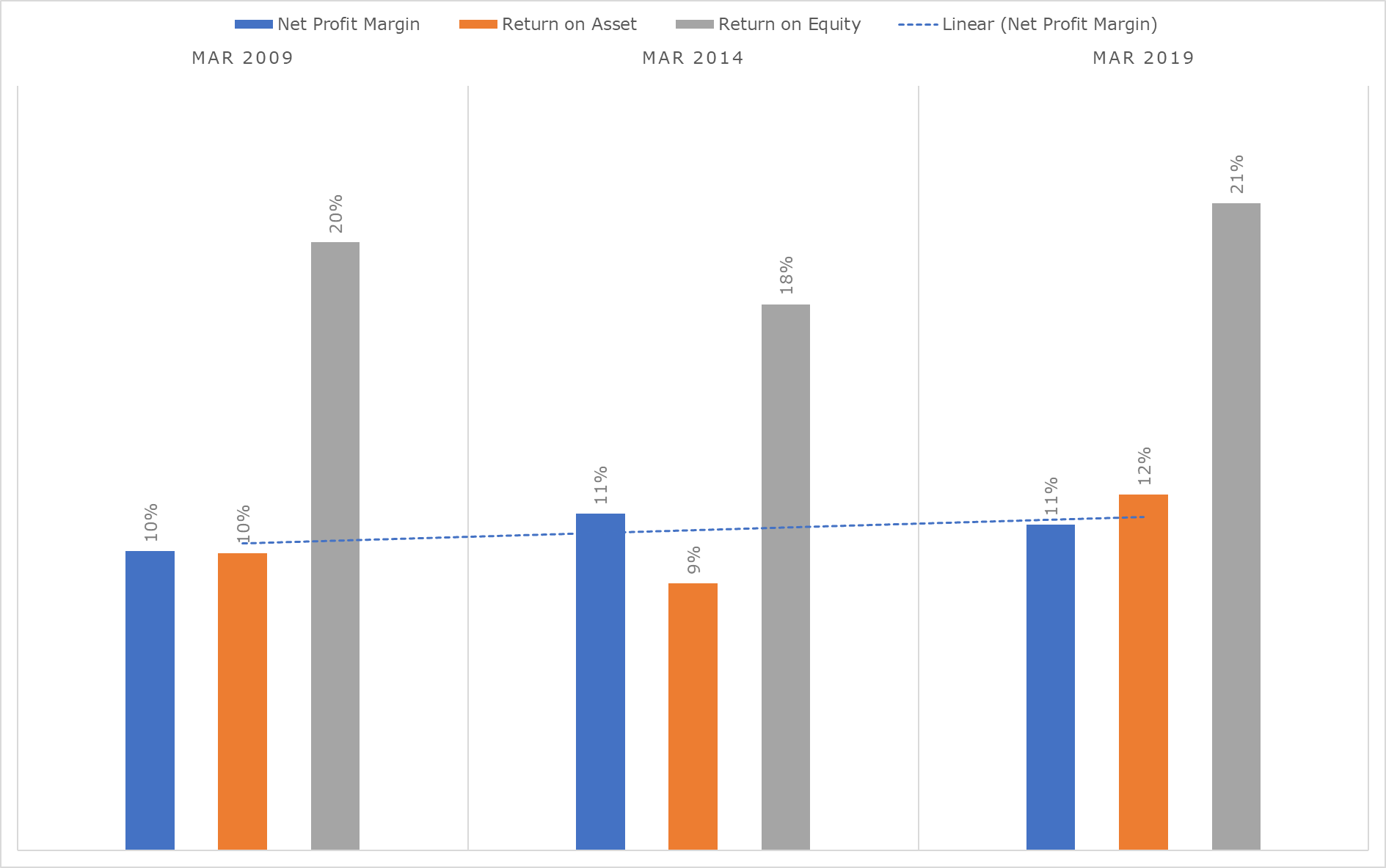

The below image shows the ‘MAGIC’ of borrowing aka leverage. For example, ROA of 12%in FY-19 is scaled up to ROE of 21% due to leverage.

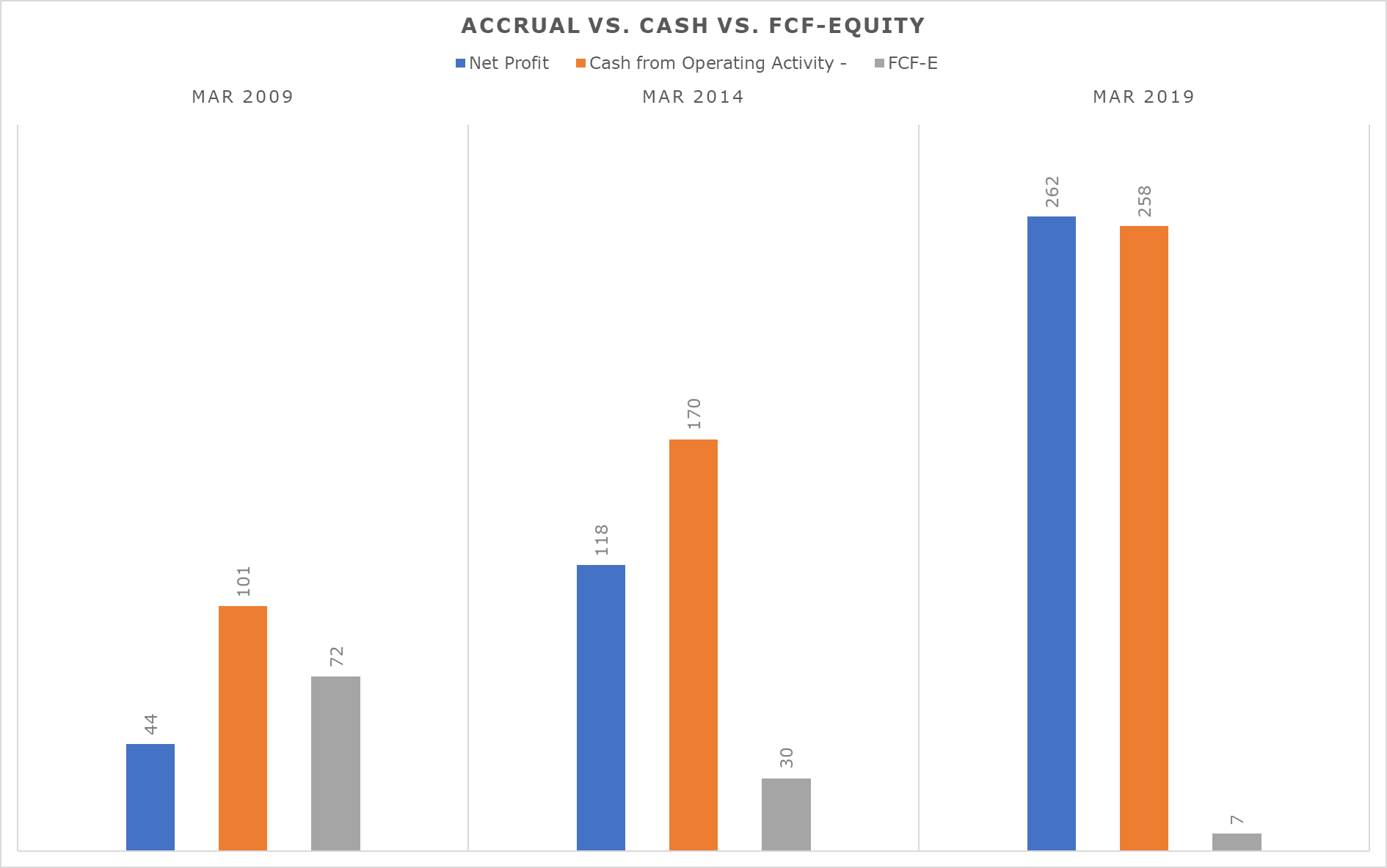

How the company has utilized the funds over this time period? Below image shows the details-

I am yet to make up my mind on below points:

1- Overseas expansions. They are yet to bear good results due to currency and country-specific risks.

2- The constant increase in Debt.

However, the company has a dividend policy to pay up to 30% of the net profit as dividend and they are following the same religiously in the last few years. Capex has been consistently 200+ Cr. in the last 5 years.

Request fellow VPers to share their notes if the company is anyone’s radar or warehouse ![]()

Disc: No Investment. Studying and sharing my notes for others learning/feedback.

4 Likes

Great in detail analysis.

One simple way is to look for ROCE instead of ROE or ROA.

This solves the problem

Regards,

Vikas

Disc : I am newbie in company analysis …. So please take the notes with pinch of salt…

I have started analyzing the company based on their past 10 years record….

I have just gone through there concalls and below are my notes ….

-

Board meeting / FY 20 (Q4) results are postponed due covid 19 not sure if there is any other major company which has done this

-

Company has major capex spend on Defense project, but I feel they are not progressing inline

Ref con call Q4 FY16

When below question was asked completed capex was 250 CR

As per Q3FY20 Capex is approx. 580-600 cr and expected revenue is 1000 cr this does not argue capital allocation

- No major order has been received and they have been spending huge capex

- So additional capex of 300 cr approx. is just spent to get 200 cr revenue not sure if I am missing some thing

Defense project land is accused to be in conservative area (could this pose a risk in future but did not see any other article after this date )

Others …

- Decline in Singreni revenue or no revenue —> severe competition and management does not want to further lower prices

- Defense ::Expected revenue 1000 cr

Expected margins :: 20-24 % … Management is positive that EBITDA would be better then explosive business due to longer gestation periods

Capex Amount:: Rs. 580 Crores to Rs. 600 Crores mark by FY 20

Capex: created facilities for INSB materials, propellants, warhead manufacturing, integration of NASA or integration of any kind of rocket or missile + testing facilities

Present Progress :: RFP stage

Chances :: Need to check

Expectation ::

Pinaka (indigenous multi-barrel rocket launch):: approximately about 1000 pieces as far as the RFP goes per annum 10 years

multi-mode hand grenade: 10 lakh pieces and that is for 2 years

Part of present defense revenue is trail order of Pinaka

Working capital :: I doubt if receivables would be done in 60 days so more WC and more debt as per management experience initial phases of projects receivables are on higher side but once the project subtilizes receivables are in 45 to 60 days

We will participate in most of these RFPs in association with DRDO and leading global technology provider.–> Not sure what this means

@Surender please check above my notes based on concalls

The notes on rising debt should also be seen in the light that most of this is for the overseas subsidiaries, as per the management. This is not a bad thing, as it limits the risk on the indian balance sheet to forex fluctuations , as having debt in foreign currency overseas in the same currency of sales limits forex exposure and potentially gets them access to cheaper funds.

whats the status of the defense orders. i was under the impression that they have already received the 800Cr order for the missiles propellants etc. details not know to me. does anyone here have an updated

Mr. Kailash Chandra Nuwal ceases to be the Executive Director and Vice Chairman following an audit of Related Party Transactions - https://www.bseindia.com/xml-data/corpfiling/AttachLive/8ab3c3c6-d9a4-4f81-a6de-f6d4279833a4.pdf

I am guessing, this could be the reason for postponing the Board Meeting.

2 Likes

Is there a family dispute going on or something? If anyone knows about it, would be helpful

@Sagar_Naik not sure if there is any family dispute

but in any case i feel this is a corporate governance issue (rental agreement ), this only raises more questions on management …

Mr. Kailash Chandra Nuwal’s has 20++ % stack in the company

Well, rental agreement is not an issue as such. Having audited so many companies during my CA articleship, almost 80% of them had rented the office space from related party or promoter owned place. I was keen to know why he did not disclose it and about the other transaction which they have not disclosed. Will try and talk to IR to see whether they give some more color.