The sales in October is also in line with last month as far as quantities go. Price realization remains low though. We should wait for egg cycle to turn upside.

Raw material consumption as % of sale should be in range of 50~55% to make above normal profit. SKM, unlike its peers, does not sell product directly to end customers. It sells products to its subsidiaries in the Europe, Japan and Russia. We need to see consolidated Balance Sheet at the end of the year to know complete picture. Last year subsidiaries reported profit of 2 Crores. 100% Advance payment as seen in Q2 suggests negative interest rates in Europe and Japan will help company reduce working capital cost in India as we move forward

1 Like

@rohitbalakrish_ Export Data and Price of egg powder can be tracked with Zauba https://www.zauba.com/export-egg-powder-hs-code.html

https://www.seair.co.in/egg-powder-export-data.aspx

1 Like

@NaMo where are you getting the details on Ovobel takeover. and today saw a 6% rise in the stock. was a news released which I seem to be missing. Holding and looking to add more if drops to 50

@ninjasoar Please refer to the article featured in Outlook magazine. http://www.outlookbusiness.com/specials/power-of-i_2016/skm-egg-products-2795

I did not see any news afterwards. My guess on Fridays price action is based on two factors. 1. Demonetisation effect on egg farmers as they are forced to accept below standard rates. 2. Bird flue outbreak in some Asian countries.

Hi, any other website which provides the export volumes from December? Zauba site has no updates after Nov 22nd.

I came across this preamble to an upcoming recommendation from a reputed brokerage house and I was wondering if the stock being mentioned is SKM. Exports >50%, debt reduction, collaboration with International partner, entering new markets etc., all apply to SKM too.

Their write-up below:

"Last week, I contacted the management of a South India-based company. We’re in the process of scheduling our first meeting. Meanwhile, here is a glimpse.

The company is a successful turnaround case with a competent management at the helm. It is one of the largest in Asia in its niche domain. A major part of the business is export oriented. In India, it alone accounts for more than 50% of the total exports in this segment. The company has grown its bottomline at double digits CAGR in the last three years. Over time, the debt-to-equity ratio has been brought down from over 1 to less than 0.4 times.

Things were not always smooth for this company. In the initial years, its products were not accepted in export regions as they failed to match the required quality standards. This was bad enough to make company operate at just one-fifth of capacity.

Since then, the company has taken measures to ensure top-class quality. It collaborated with an international partner and now enjoys a unique edge. The company’s state of the art facility puts it ahead of the global peers. It has won awards for its efficient manufacturing processes.

Quick adaption to client’s needs, competitive prices, constant innovation, strict quality control - the company is hitting all the right notes. So much so that not just clients, but its competitor’s distributors too vouch for it. The company is entering new markets, India included, with strong existing demand for its products.

Going forward, the company aims to grow at double digit rates. What’s their strategy? How will it be funded? Will the growth come with increased value creation for shareholders? And what are the hurdles? Most importantly, is the management worth betting on? We shall find out soon…"

Hi Varadha, undoubtedly the company mentioned is SKM from that brokerage firm. Also they have used exact same phrases on SKM from outlook magazine link provided in previous post.

Please see below project report

https://vibrantgujarat.com/writereaddata/images/pdf/project-profiles/Egg-Powder-Unit.pdf

Will there be any possibility for SKM to open a factory there?

Hi NaMo, it will be great if SKM expands capacities, I understand that they are operating at >90% capacity and this will be a good opportunity to expand and scale up production, it will be interesting to see if they bag this opportunity and how they manage to go about it, if they do. Do they have sufficient cash on books to fund this expansion, without taking on more debt? Something seems to be cooking and Mr. Market is anticipating something, today it’s hit UC with huge volumes.

How do we track the export volumes of SKM after Nov 22nd? Is there any website which provides this info?

Export tracking websites stopped reporting. you are right. I don’t know any alternate ways. Sorry

Yes. Only buyers today at NSE. We will know soon.

Hi Namo,

if we believe report from Desh gujrat then they are planning to remove egg powder plant from vibrant gujrat summit.

Please confirm…

Ravi

Thanks Ravi for sharing this news. Then I am confused over the UC today. I couldn’t find anything else on the web.

How do we check the clients list of SKM? I could not see all the Clients in their website.

If you keep on posting such paid views out in the open, would not the supplier of such paid views come to know about it. The appropriate forum to post it would be the not-so-hidden-gems category.

Thanks Rohan, have edited the post. I was looking for info on how to check all the Clients to whom SKM supplies?

Dear fellow boarders,

Studied into SKM Egg forum of valuepickr, really quite amazing stuff, it’s kinda almost a-z study on the company. Everything covered. Hats off to the great contributors.

With due respect to all, I come up with a lil different logic on the stock.

At first impression, looked like a scary story exposed to unforeseen / unpredictable global vagaries & vigorous raw-material price volatility – with too many variables out of company’s control; companies profitability at the mercy of occasional global tail winds.

But no more after I looked into the historic numbers. Highly impressive sales volume and value growth over solid 19 years – from since inception at 1997 to 2016. This single graph tells the whole story of BIG PICTURE.

HISTORIC VOLUME GROWTH:

The company started with a volume of 304 MT in FY1998 and the volume for the latest year FY2016 was 6603 MT with peak volume achieved in last fiscal FY2015 at 7375 MT. In all those two decades of topsy-turvy global and domestic industry scenario, the company suffered volume decline in only 5 years (compared to previous year) – in FY2004, FY2009, FY2011, FY2012 & FY2016. Quite commendable!

HISTORIC SALES GROWTH:

This is even more impressive story. The company started in FY1998 with sales of Rs 4.54 cr; sales for latest fiscal FY2016 was Rs 270 cr with the peak in last fiscal FY2015 at 271 cr. (Consolidated sales for FY16 was Rs 303 cr, which is also of very consistent growth).

The down years were just 2 – that too very marginally – in FY2010 (down by 6%) & in FY2016 (down by 0.7% - !?). Effectively I could say, THEY NEVER HAD A DOWN YEAR IN TERMS OF SALES OVER 2 DECADES. Amazing!!

HISTORIC PROFITS:

But yes, stock price is ultimately a slave of cashflows and bottomline, not of topline. The story here is not so linear like sales, but with wild gyrations driven by occasional (alternate?!) global head winds & tail winds. But mostly they managed to churn profits and GREAT OPERATING CASH FLOWS.

Now they are no more a child playing in the dynamic and risky global highway, but a well grown-up, established name globally. And now with the debt drag is entirely out of the way, they are having more fire-power to deal with this global slowdown and to swing into green ASAP.

Moat business with high entry barriers / market leader in India’s egg powder exports with more than 50% share / leading player in many of the countries they have presence / continuously entering new geographies / constantly expanding customer base (minimum 2 customers added every year, as per the historical average) / decades old strong relationship with global MNC food giants / top of the league quality products commanding a slight premium over global competitors / now armed with ammunition of debt free B/S / investor friendly, capable, kinda intelligent fanatic Mgmt with ambitious targets / very consistent topline numbers.

The good part of staying with honest and competent people (mgmt) is that they do all the worries and takes care while investors can sit back and relax. SKM Egg is having that kind of management. Even I tend to say, it will join the elite club of companies run by Intelligent Fanatics – Shree Shivkumar & team is so dedicated.

IF TWO DECADES OF PAST PERFORMANCE IS OF ANY INDICATION, notwithstanding the current severe business down-cycle, THEY WILL FIND A WAY AS THEY HAVE THE WILL.

So, it’s BASICALLY A BET ON MANAGEMENT CAPABILITY to turn every stone for growth.

Given their size, scale and global franchise now, the downside for stock price would be very limited below the 52 week low of Rs 50.

Stock may not be attractive in the short-term; may be few more quarters of difficulties in terms of numbers due to the current GLOBAL GLUT AND DOMESTIC DRAUGHT.

But certainly makes sense to an investor with over 3+ years view. Things could evolve to make it a serious long-term story. Also now I sense the entry of smart money into this stock.

Its a call is based predominantly on BIG PICTURE rather than number crunching, keeping investing simple AMAP.

Happy value investing!

Disclosure: I have entered recently @ 62; still adding on weaknesses.

8 Likes

Interesting article. Egg powder exports in India flourished because of this reason, now with supply coming back, perhaps an oversupply situation prices of egg and thus egg powder are going to be in check.

2 Likes

Your above two posts are very good. Just wanted to share that. These are the questions that as analysts we should try and answer…

1 Like

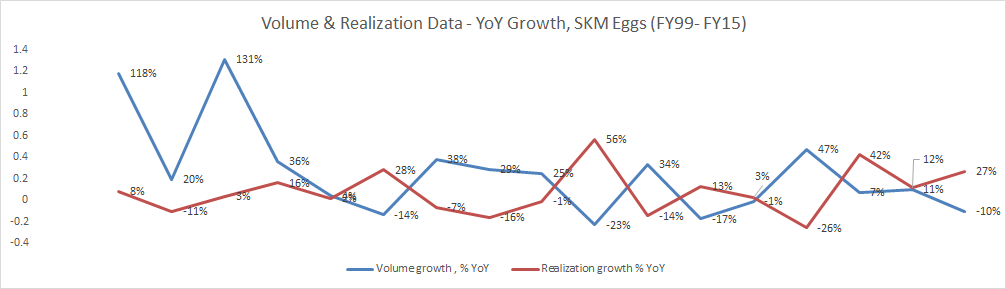

Just trying to do more work on this. if we look at the volume data for the last 20 odd years- it has been very erratic. One needs to understand this cycle better.

Similarly, realizations have been also very erratic. Almost counter to the volume growth, and that’s the reason perhaps for the sales in INR terms to not decline as someone mentioned in the post…

Its very critical to understand what are the factors that are driving these two things.

Blockbuster rally today almost 20% circuit lockin in the end of the trade. What is the buzz around this stock ?? Is there some news ?