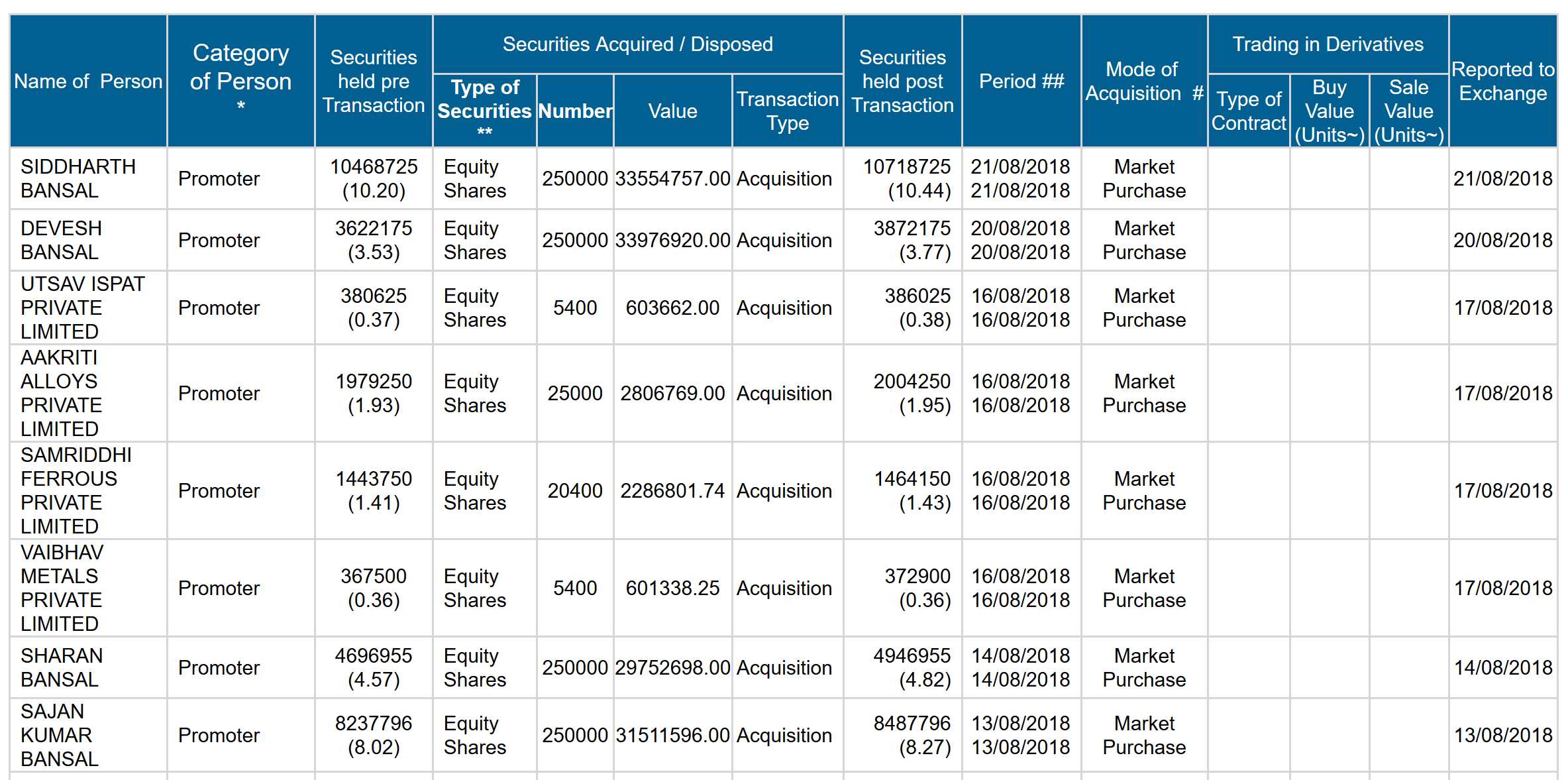

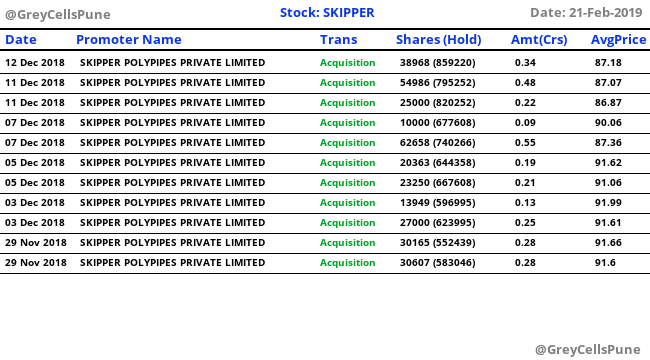

The promoters have been buying almost daily now for the past 2 weeks.

Stock is now available AT PE of near 9.

Hello…does any has idea about the impact on the Skipper due to demerger and allotment of shares of SPL by 1:1

Disc - Not invested /Tracking

https://www.screener.in/company/SKIPPER/#balance-sheet

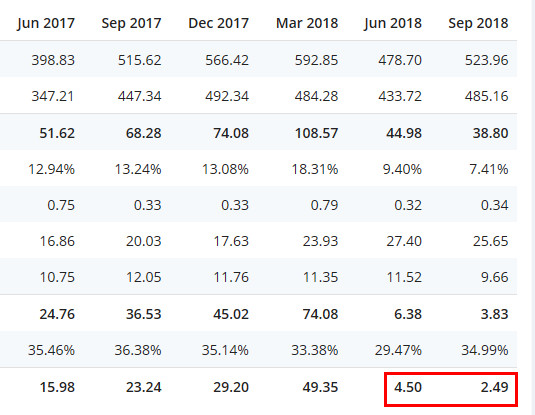

Why has their reserves decreased from 627 to 614 between Mar 18 & Sep 18?

Any idea?

It is noted that share holding of promotors increased in last 6 months i.e. from 70.17% to 71.88%. However, at the same time performance deteriorated. Although management after Q2 cited reasons like orders drying up from PGCIL, forex loss etc. They also stated that others companies of same sectors are also facing head winds. Whether we can take the reasons on face value. Disclosure- invested from higher levels

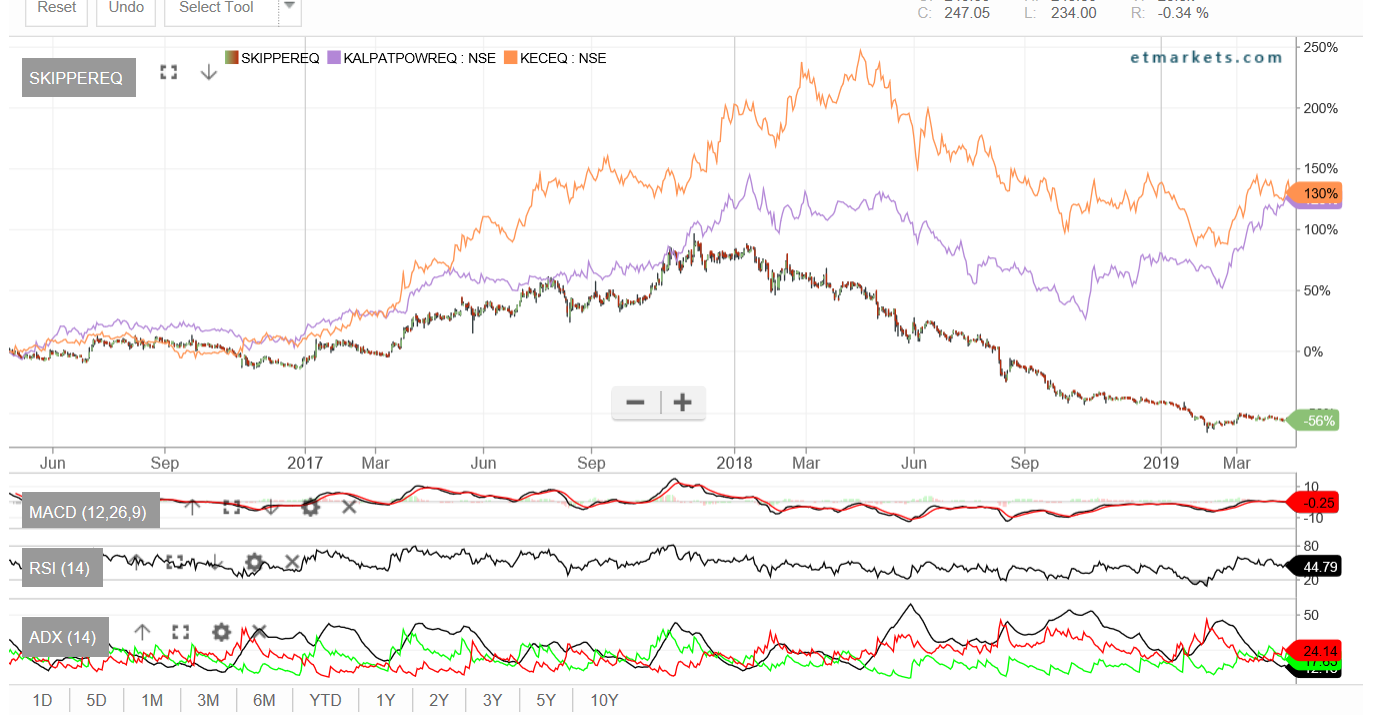

The price behaviour is telling a negative story at this moment.

Disc: Invested at higher levels.

The stock price is falling beyond expectations. Looks like something very bad happened. But not finding single news or source??? Anyone aware of this great fall?

2 Likes

Can you see the abrupt reversal of Quarterly PAT trend? Investigate the reason…

Reliance Capital 2QFY19 Result Update

https://trendlyne-media.s3.amazonaws.com/reportPDF/29760_pdf.pdf

Disc. Not following this stock.

1 Like

Had invested in this stock when i started rebuilding my equity portfolio 3 years back but exited soon as Infra is a lumpy order book project to project business, sucks some capex and this one is a real working capital heavy business. Looks like its the working capital which has created at the dent. Had got some interest due to correction and spent some time. Look at the investor presentation and compare balance sheet of March’18 to Sept’18. Revenue has remained almost same, assets have remained almost same but short term debt has shot up. A shot up in debt with flat revenue, flat assets and declining margins will only make things worst as increasing cost of debt will create a spiral cycle of margin fall unless other components of P&L bring the margins back on track. In IP, management has highlighted reasons for increase in working capital loan. I think deck and concall has enough hints on this state of prices due to multiple factors apart from what I mentioned like flop pipe market entry, heavy forex losses (again it is important to study risks associated with company/management) etc. and obviously a bad news in a fearful mid and small cap market is a real bad news  . Disc: watching from sidelines. Interested due to value valuation gap play but willing to to stay on sidelines till risk reward gets in favor on a relative basis. In current times, much stronger businesses available. If they can improve margins in a sustainable manner and still price offers attractiveness, may have a re-look

. Disc: watching from sidelines. Interested due to value valuation gap play but willing to to stay on sidelines till risk reward gets in favor on a relative basis. In current times, much stronger businesses available. If they can improve margins in a sustainable manner and still price offers attractiveness, may have a re-look

3 Likes

One can only draw some comfort that management is still holding more than 70% and increased stake in last 6 month.

Disclosure: invested from higher levels

Monday results and conf call details

1 Like

Profit Rs 6.4 Cr. approx 78% decline from YoY quarter. The following points r noted while listening to concall:

(i) there was liquidity crunch which led them to lower execution - but question is that whether they are getting difficultly in credit.

(ii) regarding non supplying information to Cricil - they mentioned that they r discontinuing Cricil rating, since they r already having another rating agency - CARE

(iii) debt position is approx 650 Cr. while approx 175 cr. is in long term debt while rest is in working capital.

(iv) They have highest order book this time and approx 70% are variable rate contract.

(v) depreciation reduced due to very little capex and new method of depreciation where depreciation is calculated on remaining life of assets. Some assets have completed their life.

(vi) international orders are showing strong traction and margins are supposed be higher, they being low cost producer.

(vii) they mentioned that they prudently executed/ despatched orders in this quarter to avoid defaults.

.(viii) bids are also being invited by PGCIL, however there concentration is much on Railways.

The commentary of management was very positive and they expect to pick up margins from next FY.

I may be missing some crucial points of concall, so please hear the same. It is available on researchbyte

I think at this moment one can only wait and watch whether management walks the talk in next few quartes.

Disclosure: invested

2 Likes

1 Like

https://www.legalcrystal.com/case/656001/delhi-development-authority-vs-skipper-construction

all most no patented products thus lacking long term pricing power

Capital intensive and cost of raw material varies as the cyclic in nature

@Kanwal Sudan pointed out well the receivables are quite high and there i not explanation How the company is going to expedite the process of recovery

High cost of capital will squeeze out the margins of skipper

if one compare Skipper Ltd with M/s kalpataru and M/s KEC international Share price movements showing difference one may need to have deep dive in to company …?

disc : Not invested in watch list but waiting at sidelines searching for answers

1 Like

The demerger of the polymer business can make Skipper at the better position for growth. I read this article - SKIPPER DEMERGES POLYMER BUSINESS FOR POTENTIAL GROWTH mentions that the T&D and the EPC business which is already profitable is separated and the less mature polymer business is combine with Skipper Pipes.

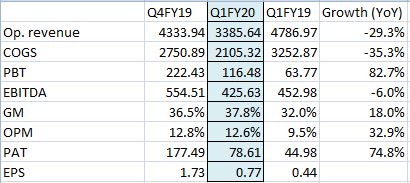

YoY consolidated sales decreased 30% while PAT increased 75%.

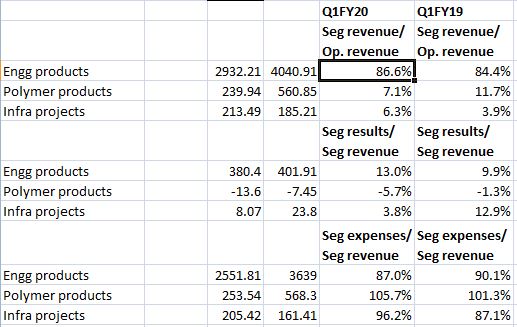

Polymer segment continues to make loss. Infrastructure segment expenses increased. Engineering segment margins have improved considerably.

1 Like

The Q2 FY 20 result of skipper ltd continue to be poor. Sales are decreased. As per management presentation ( this time perhaps they skipped the con-call) the lower sales was a conscious decision for preserving bottom line. It appears now company is taking lesson from past mistakes of depending too much on one customer ( PGCIL). Next couple of quarters will be interesting to watch and challenge for management to walk the talk.

Disclosure: Investing from higher levels

Does anyone still track this company? Dec’19 quarter results seems like the company is trying to rein on costs and try to improve profitability. Though the overhang of decision to not demerge polymer division will still linger, is there any value emerging from this counter?

1 Like

Company is skipping investor con-call for last 2 quarters which appears a negative, rather company should come forward to clarify the issue which are affecting their sales and performance. However, still promoter stake is approx.72% which gives certain degree of confidence. From their investor presentation following things noted:

1.EBITA as % of revenue has improved for Q3 FY 20 and 9M FY 20, which also endorse the management statements they are not chasing growth at the cost of financial discipline.

2. They have cited revenue impact due to absence of contracts in last 2 years in domestic market, absence of short term orders and structural changes in polymer segment.

3. Engineering EBITA ( w/o forex gain) is back to normal ( approx. 13%) which they cite is due to cost cutting measures, stable raw material cost and better operational efficiencies. They expect margin to be better in future.

4. Total Order book is 2280 cr. which is 1.5 times sales ( it gives some revenue visibility )

5 Secured new orders worth 274 Cr. in Q3. Bidding pipelines ( 4150 Cr.- domestic 3450 Cr., domestic 700 Cr.)

6. Seeing much traction in export orders and expecting to grow export order to 50% from 13% in FY 19. In grew from 300 Cr. ( FY 19) to 373 Cr. ( in 9M FY 20).

7. They are broad basing on their customer, geographies, sectors for better profit margins. low sector beta, becoming global player etc.

8.They have many international certifications, which appears some time of moat. They enlisted 11 prominent customers in last 2 years.

9. They have competitive price in comparison to Chinese players.

10. They have considerable higher bidding volume in international T&D.

11. It appears polymer segment is growing but effect is yet to be seen.

From all above it appears to be an interesting story going forward. However, execution and walking the talk will be challenge in future.

Dislclosure: Invested from higher level and may add further on current market price

2 Likes

rating update on skipper ltd.

Disclosure: Invested from higher levels