What is the record date for demerger? Is it 1st April,2016?

On what basis are you giving a PE multiple of 20 to the plastics business?

Supreme, Nilkamal, Prima- all of them trade upwards of 20xFY17. That’s the rationale.

Debt ratios of both Supreme and Nilkamal are much much lesser than Sintex.

Also, both Niklamal and Supreme have a good track record of NOT diluting equity. This shows that the management quality of these 2 companies is much better than Sintex.

Considering these factors I dont think giving Sintex a valuation of 20 is fair.

At best, I would give it a valuation of 10 to begin with and see how the company and management behaves.

I used 5 PE for textile busines since its ROCEs are pathetic and 10-12 for plastics and got a valuation of around 5-6k crores. The other angle is dilution from rights and the FCCB again and governance/pledging issues and past history of doing highly dubious deals - given that, MOS looks low - at 60-62 looks a decent bet. guys like astral, supreme have a. low debt b. no promoter pledging c. no impending dilution and d. have much better governance e. better WC

6 Likes

Good results from Sintex!

YoY Qtrly TL up 20%

YoY Qtrly BL up 12%

QoQ Qtrly TL up 35%

QoQ Qtrly BL up 115%

1 Like

The receivables (Standalone: 1316.13 Cr , Consolidated: 1990.69 Cr) will have to be monitored because of demonetization affecting the Real Estate & Infrastructure sectors.

Disclosure: Invested.

1 Like

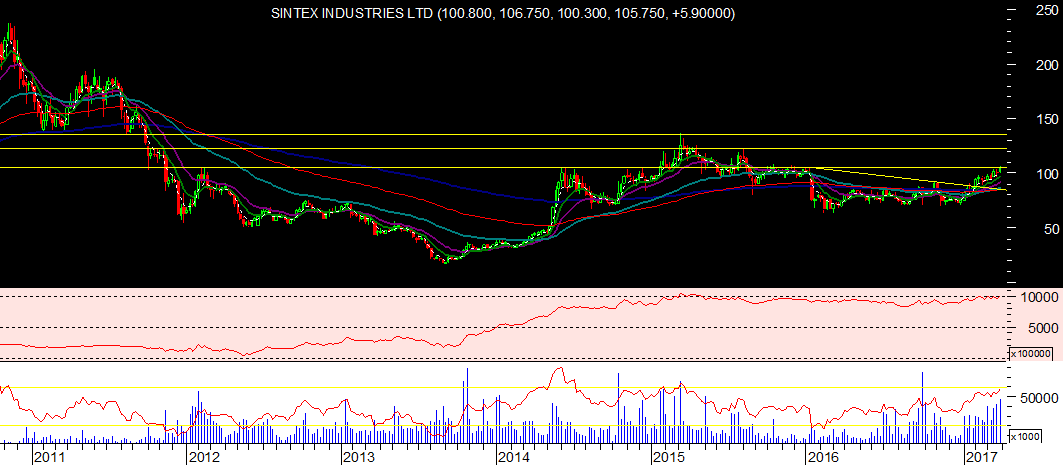

Sintex declared result today 20th Jan 2017.

Q3- 2017 profit 1,109 Mn Rs. Vs 1,808 Mn Rs. Profit in Q3 -2016.

Market seems punished this bad result.

CMP 82.70 -7.49%.

Regarding Demerger the record date is not yet announced to the best of my knowledge.

It was mentioned “appointed date of the demeger scheme” is 1st April 2016 ( Co announcement dtd. Dtd 29 September 2016) in the link below in “Key Highlight if the Demerger Scheme ” Section.

I am not sure what exactly the ““appointed date of the scheme” means. Can someone explain the meaning? Thanks.

http://sintex.in.cp-50.webhostbox.net/wp-content/uploads/2016/10/RevisedPressRelease29092016.pdf

Disclosure : Holding the share since 3 months ( 2 % of my Portofolio is Sintex Share).

Sintex Result Q3-2017.pdf (1010.5 KB)

Sintex continues its legacy to find ways to bring the stock price down and this time such a nasty surprise with very bad Q3 nos. which is historically their second best quarter of the year after Q4 so this may very well be a pre-cursor to what may follow next and market is quite right IMO in hammering the stock post Q3 result.

I think Q3 nos. are not only very bad on all operating parameters - Sales, OP, FC, Taxes, NP etc., but their bread and butter plastic segment also has shown a de-growth which is really concerning. The mgmt has not announced anything today on de-merger but anyway it can be an icing on the cake but not a rational for the investment unless operating businesses are doing well.

I may take a fresh re-look if the price dips substantially from here on.

Disc: Exited Fully.

1 Like

After holding Sintex for a couple of years as my largest holding , I sold off all of it at a loss last year as I could no longer trust the management. They always came up with one or other shock in terms of either continuous dilution of equity, or investment in textiles etc which never improved EPS. Market has hundreds of other stocks which may not shock you as these guys do. No surprise that market has always assigned a low PE to it.

Disclosure: holding none. Sold off all at a loss. No plans to ever buy it again. Pl take your own decision.

4 Likes

After getting approval from tribunal on Friday now sintex industries is in talks with PE funds to sell a minority stake in demerged entity. @Varundubey CNBC

Initiating coverage with price tgt of 191/-

Sintex Industries Ltd.

Introduction:

Sintex Industries ltd. is present in to three main segments namely: textile business, plastics business and infra business. The company was founded in 1931 as Bharat Vijay Mills Pvt. Ltd. as a textile mill. The company then shifted to Plastic business in 70s by introducing storage containers (Water tank and all). In 2000s, the company entered into new business like prefabricated structures, custom moulding and monolithic constructions. Recently the company ventured into Compact cotton yarn.

Business overview:

- Plastic Business (contributes 88% of total Revenue):

a. Custom Moulding (domestics / international business)

b. Prefabricated structures

c. Monolithic construction

d. Retail business - Textile Business (Contributes 12% of Revenue):

a. Fabric

b. Yarn - Plastic business:

a. Custom moulding :

The company has diversified custom moulding which applies to areas like Automotive, aerospace & defence, Electrical, mass transit and off-road vehicles, Medical imaging products etc.

Various acquisitions has been done in 2007-08 period which helped the company to build its capabilities in this business and got clients from Fortune 500 base.

o Sintex NP SAS (Europe)

o Sintex Wausaukee composites INC. (US)

o Sintex BAPL Ltd. (INDIA)

Company has diversified clients in terms of industries as well as companies. They don’t have single client contributing more than 5% of the Custom Moulding revenue share.

Total contribution to total Revenue is 44% while domestic contributes to 45% while international contributes to 55%.

b. Prefabricated structures:

• Company entered into this business in 2001 and has 3 manufacturing units which manufacture structures like class rooms, Medical centres, portable ATMS, site office and so on.

• Mainly these products are used for the social development area for both Government (B2G) as well as B2B. Company covers nearly 80% of India’s geography.

• B2B business is for the companies who are eligible under the New companies Act, 2013 where it is mandatory for large size companies to spend at least 2% of the Net Income while the B2G business get contributed by the various government scheme such as Sarva Shikha Abhiyan(SSA), Swach-Bharat, National Health mission and so on.

c. Monolithic construction:

• Commenced in 2005, it is largely used to construct low cost housing. Basically monolithic construction involves fabrication and casting of four walls and slabs together by pouring fluid cement concrete while using nominal quantity of metallic reinforcement bars to form a single or multi-storeyed building.

• The company had various issues regarding the policy of government in terms of placement of order and various clearance issues forced the company to reduce focus.

• Advantages of the business:

Time savings: It takes 6 months compared to 2 years using convenital construction techniques.

Strengths: Provides robust structural resistance to vertical and horizontal forces

Dead load: Estimated at almost 50% of the conventionally constructed multi-storied structures.

Labour: Requires low skilled worker intensity, facilitates time bound mass construction with limited resources.

Zero maintenance cost

d. Other Retail business: this segment focuses on B2C business

• Water storage:

Pioneers in water storage solutions since 1975 having varied products with market leadership of more than 60% across India.

• Cold chain Network:

Sintex has developed an integrated solution for cold storage by manufacturing sandwhich panels which are ideal for walling and roofing solutions and are considered great energy savings for air conditioned and cooled buildings.

• Sub-ground structures:

Sub-ground structures like septic tanks, Packaged treatment solutions, Bio-gas holder, manhole structures and covers that provides drainage and water treatment solutions

• Environmental Friendly products:

Aggressively promoting a new range of Euroline dustbin and containers with international looks and finish which have received an overwhelming response from several markets particularly Eastern India

• Interiors:

Affordable quick to construct and low maintenance plastic products such as false ceilings, doors, cabinets aimed at low cost, mass housing solutions such as slum rehabilitation shelters and Janta housing. - Textile:

-

Sintex textile division is the oldest one which established in 1931 having manufacturing units in Kalol. -

In the last two decades the company is into structured dyed yarn shirting and corduroy fabrics

a. Fabrics:

• Sintex manufactures high-end, structured dyed yarn fabrics for shirting, ultima cotton yarn based corduroy and other speciality fabrics

• Sintex mill produces high end structured dyed yarn shirting and corduroy fabrics and has an annual production capacity of 24 mn meters supported by 348 weaving looms and 24,000 yarn spindles that produce inputs for fabrics

• This business further divided into two:

Collectors design : which manufactures two collections comprising of 12,000 designs per quarter which is marketed to premium segments in Europe.

Fabrics for readymade garments: company provides structured dyed yarn fabrics which are marketed to various domestic marquee clients such as pantaloons, allen solly, Louis Philippe, Arrow etc in India.

b. Yarn:

• Sintex has recently commercialised ultra-modern, highly automated, world class compact cotton yarn spinning plant at Pipavav, Gujarat and is in the process of setting up another spindle unit for blended yarn as well.

• Company plans to target selling the premium compact cotton yarn to export markets like China, Malaysia, Vietnam, Thailand, Indonesia, Turkey, Greece, Portugal, Italy, Egypt, Nigeria, South Africa, Brazil, Argentina and North-America.

Phase 1 – commissioned in Q1 FY 17 Phase 2 – Upcoming by September 2017

Capex: Rs 19, 000 millions Rs 21,000 million

Product: Compact cotton yarn Compact / Blended cotton yarn

Export : 50-60%, Domestic: 40-50% Interest subsidy: 7% ( Gujarat New textile Policy)

TUFS benefits: 4% Electricity Duty rebate: 15%

VAT Exemptions : 8Years Debt : Equity 70:30

Investment Thesis:

Basically the main theme behind Sintex Ltd is the Demerger play. According to the http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/086c4641-6f2f-40c1-8026-e70975ffc333.pdf<src="/uploads/default/original/2X/0/061d6eccabdc6ec2ea969f94c5b0e438f1ed3120.png" width=“690” height=“301”>img in BSE, the two business will be separately listed, one will be plastic entity and other will be Textile entity.

Financials:

Textile Business:

Year (in millions) 2013 2014 2015 2016

Revenue 4732 5482 7281 9464

Revenue growth 1% 16% 33% 30%

EBIT 423 732 1255 1480

Margins 9% 13% 17% 16%

Capital Employed 11841 21067 29993 49257

ROCE 4% 6% 6% 5%

This entity will constitute Fabrics business and Yarn business. Till FY 16, Yarn business revenue is Zero and will start contributing in Fy 17.

Management has commented that after this expansion plan, this business is expected to grow at a CAGR of 35%.

Company will be able to generate higher realization due to Compact cotton yarn vs basic yarn.

Company will also get various financial incentives such as TUFS, Gujarat New textile Policy, VAT exemption as well as power subsidy.

Plastic Business:

Year (in millions) 2013 2014 2015 2016 2017

Revenue 46347 46135 55750 63851 73429

Revenue growth 16% 0% 21% 15%

15%

EBIT 5570 6187 7901 8604 9895

Margins 12% 13% 14% 13% 13.45%

Capital Employed 46884 41627 44797 55401

ROCE 17% 13% 19% 19%

Revenue has been growing at a CAGR of 17% from 2008-16 while the margins are nearly consistent at 12-13% in the same period.

Valuations:

o Current Market cap is Rs 56828.7 million,

o FY 17 EBIT (plastic business) is Rs 9895 million,

o Debt is 30,000 million

o so if the multiple of 12 is given to the EBIT of 9895 million than EV will be Rs 118,739 million less Debt of 30,000

o Than the market-cap is around Rs 88,739 Million so compared to current market cap the other businesses are totally free.

While the textile business will also start contributing when both the phases in Yarn business will be completed in FY17 and this business can grow at 30-35% CAGR.

Risk:

• The company had issued FCCBs which will be matured in May 2022 (coupon at 7%) at a conversion price of 92.16 per share and they have also done equity dilution year after year as in Warrants, QIB, Rights and so on. This activity doesn’t suit the qualities of the management so we need to check every quarter.

• The company have 40.24% pledged shares. (Need to ask them)

• The textile business seems very capital intensive business which means ploughing in large capex on a regular basis leaving little room for debt to come down and generate free cash flow

• Company has done various small mergers and Demerger which gives the suspicion of management integrity indulging in accounting manipulation. (But, Alembic Pharma’s promoters were also doing the same thing but after their demerger in Alembic Ltd. and Alembic Pharma, pharma became the compounder but the Alembic ltd is still at the same place.)

Technical

2 Likes

What is the logic behind 1:1 de-merger? I don’t understand this, but it looks like they are doing it based on asset value of the two businesses, which is very unfair in my view and this might drag down plastics valuation. There is this de-merger play in this stock, but given management’s history of siphoning of cash from plastics to textiles, the ratio is looking crooked to me.

Allotment of 18,29,597 Equity Shares of Re. 1/- each of Sintex Industries Limited to Foreign Currency Convertible Bonds holder upon exercise of their conversion Right:

Corporate announcement

post demerger…stock went from low of 16.15 to 34

Can you please share from where did you get these financials:

Textile Business:

Year (in millions) 2013 2014 2015 2016

Revenue 4732 5482 7281 9464

Revenue growth 1% 16% 33% 30%

EBIT 423 732 1255 1480

Margins 9% 13% 17% 16%

Capital Employed 11841 21067 29993 49257

ROCE 4% 6% 6% 5%

I’ve been digging around to get the division-wise financials, but didn’t quite find any.

Does anyone know where we can get the division wise financials? I was assuming that there must be some mandatory filing, that documents this information, but having dug through the Scheme of Arrangements, I don’t see the financials of the divisions being demerged. I was hoping to see some kind of PL/BS for each of these divisions. Is this not mandatory for demergers?

important announcement for conversion ration amongst… sintex industries (textile business) and sintex plastic(rest of the business)

As per this the % cost of acquisition of equity shares is 36.38% for Sintex Ind.(textiles business) and 63.62% for Sintex Plastic Technology (rest of the business). Does this mean that, Assuming fair market price of Rs.100 for the combined pre-demerger entity, Sintex Ind. (textiles business) and Sintex Plastic Technology (rest of the business) be listed at Rs. 36.38 and 63.62 respectively?

Why was Sintex Ind. (textiles business) available/opened at around Rs. 17-18 yesterday and not at 36.38?

When would Sintex Plastic Technology (rest of the business) be listed and at what price?

Does this mean that, Assuming fair market price of Rs.100 for the combined pre-demerger entity, Sintex Ind. (textiles business) and Sintex Plastic Technology (rest of the business) be listed at Rs. 36.38 and 63.62 respectively?: YES. THOUGH THIS IS THEORETICAL EXERCISE AND MARKET MAY HAVE LITTLE DIFFERENT VIEW.

Why was Sintex Ind. (textiles business) available/opened at around Rs. 17-18 yesterday and not at 36.38?: MARKET TAKES TIME TO UNDERSTAND AND ADJUST NON-LINEAR EVENT.

When would Sintex Plastic Technology (rest of the business) be listed and at what price?: AS I UNDERSTAND A MONTH OR TWO, WHICH ARE REQUIRED FOR FORMAL PROCESSES TO GET OVER FOR NEW ENTITY TO GET LISTED.