Main problem for Renuka Sugar is its location i.e. Maharashtra and Karnataka. Here sugarcane crop is mainly for 18 months and needs 2 rainy season to grow. If this year rain is good, it will reflect in 2017-18 crushing season provided next year is also good. Shree Renuka MD has said that company will get 20% less sugarcane next year i.e. 2016-17. Please read interview here.

It is different in UP. They need only one rain to grow sugar cane. Also there are very less chances of drought in UP because of its geographic position.

Company is not going to get sugarcane to crush that’s why it is not participating in sugar share price rally.

There is no data available for Brazil operations. It might be possible that Brazil and refinery operation may lift share price.

I believe real reason of not rallying in mountain of debt on bajaj hind and shree renuka…bcoz it is expexted that profitability to be eaten up by high interest…thats y no one buying here bcoz many other sugar shares with low debt are available…

Shree renuka has big inventory that can take care of 2 quarters… and also for next 2 quarter atleast there will be no shortage for cane as off now…

Hope for the best…some bumper results to be shown so that sentiments inproves here…so thay we have some handsome returns till diwali…

Next 2 q result will be bumper…yearly eps to be minimum 6…and industry pe is 25…so 6X25=150/-…thats industry pe even we give low PE due to debt i.e say 10 instead of 25…we can have 6X10=60/- share price…this can be easily available if sugar prices remain robust for next 6 months from now…

I believe they will and the sugar shortage to increase from next march even more…intersting times ahead…hild tight keep an eye …inly problem govt. Do not play a spoiler in controlling prices…Regards

Its Brazilion subsidary, Renuka De Brazil which has filed Bankruptcy protection has submitted fresh plan to repay the debts. Once Brazil units start breaking even, there should be reversal in Shree renuka’s fortune. Since fundamentals of sugar are improving in international market, It will make things comfortable for Shree renuka because of two reasons:

There should be rise in valuation of its asset in Brazil. Since there is no new sugar plant built in world in last 5 years.

Because better realisation of sugar prices, there should be reduction in debt.

Mehnazji: I looked at chart yesterday morning. You are right Bollinger band does demonstrate squeeze. May be it might see some for time and it will compress further as price bars are mini bars since many days.

My observations are squeeze was very narrow during bottoming out period from 21.09.15 to 5.10.15 at the price of 7 Rs. and consolidation lasted for about 40 days before a blast. This time consolidation has already taken 30 days and width of band is approaching slowly those level.

Shree Renuka Sugar has successfully turn around the books. Substantial relief in interest out go. This will improve the bottom line.C0A57EEE_1C54_492D_B417_C0CC5BAFBC2A_132226.pdf (1.9 MB)

that shows picture abhi baaki hai…!!!finaly demand and supply will set the prices…!!!shortage is genuine …price rise is fundamental…they can check the prices from going higher but cant make it fall too much…!! even current prices are more than sufficient to send eps skyrocketing for all the stocks in next 8 months…i.e march end…!regards.

Shree Renuka Sugars Ltd has informed BSE that under the Judicial

Protection Law (11.101/2005 Recuperacao Judicial), the designated court

in Sao Paulo, Brazil has on July 26, 2016, approved the Re-organisation

Plan of the Company’s subsidiary viz., Renuka Vale do Ivai S/A (Renuka

VDI).

hello … Extremely surprised to see no run up in renuka today … infact its coming down …

Are we missing something that market is not giving thumbs up to such a good news !!

Mehnazji: Good finding about 30 EMA. As predicted by you Renuka has bounced smartly from 30 EMA and in the forthcoming uptrend we can use it as SL. With the changing fortune of Company, I hope target of 35-36 is very much possible incoming months.

Thanks for your continued input with rich stuff.

I can say turn around story of renuka at the half way!

Hi friends. Do you think shree renuka or bajaj hind are worth to invest in at cmp considering their debt… How you see them after this quarter results… Will they make the festivals sweeter… Request your views…

What does this mean and what impact it will have on the share price?

“(the “CLA”) entered into between the Company and

the JLF Lenders and the consent of the shareholders

be and is hereby accorded to the Board of Directors

of Shree Renuka Sugars Limited (“the Company”),

(hereinafter referred to as “the Board” which term

shall be deemed to include any Committee thereof),

to accept the conversion right, exercisable by the

JLF Lenders to enable them to convert a part of the

loan into such maximum number of equity shares

of the Company as mentioned in the Explanatory

Statement, in accordance with the terms and

conditions as mentioned in the CLA entered into

between the Company and the JLF Lenders or as

agreed between the Company and the JLF Lenders;

and the Board be and is hereby authorized to create,

offer, issue and allot in one or more tranches, upto

such number of Equity Shares having a face value

of 1/- (Rupee One) to each of the JLF Lenders as mentioned in the Explanatory Statement at the price determined in accordance with Chapter VII of the SEBI ICDR Regulations, subject to minimum price of 16.56 per equity share, on the terms and conditions

mutually agreed by and”

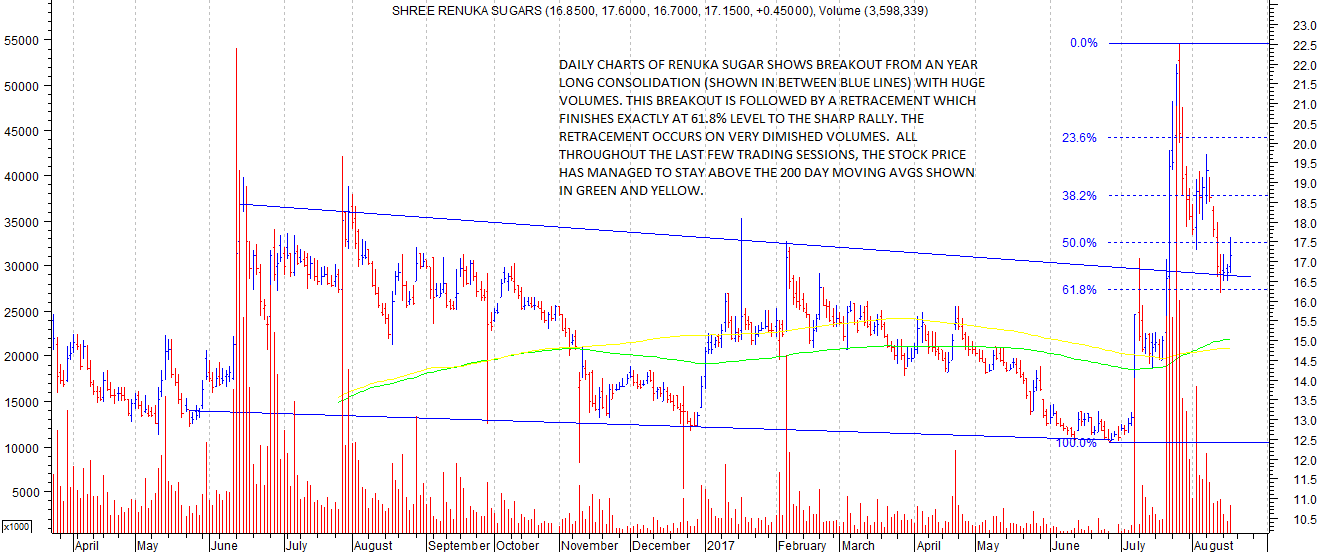

Attached a daily chart of renuka sugars showing a breakout from a year long consolidation with high volumes and subsequent retracement with low volumes. Now we need to see if it can resume its uptrend. Fundamentally a lot of interesting things are happening with its Brazilian subsidiary on the blocks post the restructuring with its lenders.

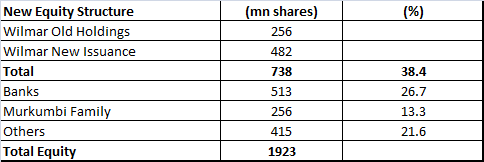

Currently Renuka’s standalone debt stands at Rs 3600 cr. Post this exercise, according to the management, debt will come down to Rs 1500cr (As reflected from above Equity, RPS and OCPS totals close to Rs 2220cr). Though the above debt is payable but largely starting from 8th to 10th year from date of restructuring. So interest will be charged on balance Rs 1500cr.

Finance cost stood at Rs 365cr in FY17, this will come down close to Rs 150-175cr.

Company has put one of the units in Brazil for sale (Madhu Mills). It owns 2 units. According to the company if sales succeeds then Brazilian debt (Rs 5000cr) will cease to exist. Bids will be submitted by August 8, 2017. They will be opened on 5th Sep, 2017.

Old Shareholding

New Shareholding

Equity issued will go up from 929 mn shares to 1923 mn shares (more than double). Promoter stake coming down to 13% isn’t positive.

Broad impact

Yearly interest cost will come down by Rs 150-175cr. Close to Rs 2000cr of debt (Principal) will be paid from 8-10 years onwards.

Brazilian unit sale will be good trigger since it settles Rs 5k cr debt and frees one unit as debt free.

Stock has hardly participated in entire sugar bull run. a) with debt restructuring b) brazil unit sale, provides good optionality to play sugar cycle. If above doesnt work downside is as good as what stock has been all through sugar cycle (which started from Oct-Nov 2015) at Rs 13-14/share.

For long term holding, one needs to analyze potential EBIDTA company can make post restructuring, since there will be operating efficiency and financial efficiency which will need to be factored into. Most Sugar companies are generating close to 20-20% operating margins, While Renuka did 4% EBIDTA in FY17.

as per Mr. Murkumbi, MD Renuka Sugar !!

as per Mr. Murkumbi, MD Renuka Sugar !!