I think what they have done is quite unexpected and unethical. They say at “arms length” we know that is never the case. Why would they acquire for the shareholders a company they own personally. The numbers are also quite terrible for the acquired company.

Disc- not invested and glad I got out.

Did not expect this from these guys. Thought they are better than this.

@valuestudent

Disclaimer: I am not very good at reading acquisitions and mergers and their subsequent impact. It may so happen that whatever I have written below is crap, hence please feel free to correct.

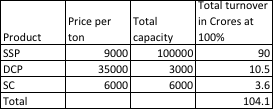

What I see is that the acquired company is into fertilizer space and based in Haryana. It has a turn over of ~35 crores. The PAT margins for the same are dismal and very low.

Shree pushkar has bought this at 33.30*2710000 shares = ~9 crores.

I then researched the approximate prices of SSP, DCP and Soil conditioner over the internet (not sure how accurate this would be as the price would depend on quality of the products too:

So, based on this data, based on current rates the acquired company has installed capacity to add 100 crores to the topline (considering 100% utilization)

Even if we consider a more practical 50-60% utilization we are talking about 50-60 crores per year.

After take over, I am sure with the able management of Shree Pushkar, over a period of time, the margins would improve too.

Also I would wait for management commentary related to the acquisition before questioning their ethics. If the overall intent is growth and there is no loss to shareholders, I dont see any issue. Again please correct me if I am wrong.

6 Likes

Hi @chets

Good observations.

I still find the deal suspect. Reasons:

-

If the promoters felt that there was a good future for the acquired company why are they being so generous and giving it to SP?

-

I am a firm believer in past actions speak about the future (That’s also why I was disappointed, as this I did not expect from the Makharia’s). The past of the acquired company is saying even at 45 crore sales profit was a measly 2.32 crore and since we have a single sheet to go by, would I not want to suspect the figures? They could have made a loss, or much lower profit, but cooked books to make the acquisition happen?

-

The promoters had earlier mentioned that they might do an acquisition. We were all aware of it. Suddenly we find out the acquisition is not an acquisition at all. It is a sale by the promoters itself of their privately held company to their listed company.

-

They simultaneously announce preferential shares to themselves. Why? What is the need? Any reason that anyone else can see?

They will increase their holding in the profitable SP by diluting equity of SP for us shareholders and using SP money of shareholders which is generated by acquisition of Kisan Phospate.

Just my views.

1 Like

I have gone through that notice. I don’t like it very much and am little surprised. But, at the same time, we have to look at this in the overall context. The acquired business is not loss making, acquisition price isn’t too steep seeing the incoming capacity; while business synergies can help improve profitability of the acquired company.

We need to remember that this management has not put a foot wrong since IPO. Mr. Punit Makharia is continuously buying from open market (last buy was around 225), so he is extremely bullish about the prospects of SP. Then, preferential allotment is coming as well. We need to see at what rates do they get the allotment. If this is around 200-210, i would be okay, as SP is pretty much rightly or rather slightly overvalued in comparison to its competitors. They want to increase the stake in the company without doubt. I will say, we need to keep hawk’s eye, but at the same time need to ignore a few things which are rather immaterial. Otherwise, one will not be able to hold any company for long periods.

Related party acquisitions are always a question mark but it doesn’t always mean it is mal-intentioned. I wouldn’t have preferred this, but i am at least as of now not too much bothered.

Pref. allotment might be for further expansion into textile chemicals. Look at Bodal, where Mgmt was going for 8000 MT of dyestuff capacity in the first round which they increased to 12000 MT due to demand scenario. So, i believe, dyestuff segment is going to see better days ahead, and mgmt is trying to get the financial power to do that.

4 Likes

Board of Directors of the Company, in its meeting held today i.e. Thursday the 7th September, 2017 (which commenced at 2.30 p.m. and concluded at 5.30 p.m.) has considered the proposal of allotment of equity shares on preferential basis to the promoters of the Company and matters incidental to it.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/a553ef7f-bf37-4100-9394-086a3ecdb07c.pdf

1 Like

6.15 lac pref. warrants being issued to the promoters. they said 2nd sep would be considered as the relevant date. so price range for allotment wd be 2 or 26 week average price? or wd this be determined by valuation report separately?

@Mridul @chets No clarity on the pref price just mention of valuation report and also, where is the dividend? Were they not supposed to give Rs. 1.50 dividend. Please watch carefully. I am not paying too much attention.

Missing clarity on pref price allotment is indeed mysterious.

Regarding dividend, the date is between 4th-11th Sep.

1 Like

Received EOGM mail with issue price as:

“The issue of shares on preferential basis shall be at price of Rs.211.57/- (Rupees Two Hundred and Eleven and Fifty

Seven Paise) per equity share. The price is determined in compliance with SEBI (ICDR) Regulations for preferential

issue as per Regulation 76”

@Mridul was right in predicting about the issue price. .

4 Likes

Good Upmove - 20% UC by Shree Pushkar today - Any news ??

2016-17 AR: http://www.bseindia.com/bseplus/AnnualReport/539334/5393340317.pdf

Dividend was credited to my account on 7th October.

2 Likes

Some interesting points from the AR:

- The industry continues to operate within a tough environment. The current economic aspirations, the perennial pollution problems and cleaner environmental necessities, pose a challenge on the Industry which under any circumstances has to be met. Our challenges are not only financial. Our task in oversight involves monitoring three areas of risk, Financial, operational and geopolitical. On our part, I may say in very few words that we, within our capacity and reach, are clear on our financial framework, and are in the course of action to meet the other challenges as well.

Currently we have on our drawing board plans for the next 3 years to maintain our upward trajectory of growth through continued expansions in our operations, a planned approach and a strict discipline over capital costs and gearing - As regards the funds earmarked for other corporate purposes at Rs.4.00 Crs. also stands utilised towards setting up of the new office premises at Goregaon, and purchase of an additional new plot of land admeasuring 40,000 sq. MTs at MIDC Lote, for future expansion.

- Textile processing Chemicals:As was indicated in the last annual report, we have launched 12 auxiliary Textile processing chemicals around mid of FY 2016-17. These products have shown good market acceptance, and with the demand for these products steadily increasing we propose to launch a few more chemicals in the current year and have also initiated active steps for setting up a proper manufacturing facility for these items on Plot No.D-18.

We are thus moving in the direction of providing a one-stop textiles solution Company. - The external credit rating of your Company has further improved from the earlier “[ICRA]A (-)” on long term scale and “[ICRA]A2+” on short term scale, to “[ICRA]A” and “[ICRA]A1” respectively by ICRA, which has been as a result of our performance and financial discipline.

- MAT credit entitlement for March 2017 is shown as 54.79 lacs under Non current Assets. However they have availed 0 in 2017.

- Reactive dyes contributed to 13% of total revenues in 2017. This shows that there is a robust demand for this segment.

- The EBIDTA over the last 5 years has grown from Rs.22.74 Crs in 2012-13 to Rs.52.34 Crs in 2016-17, which in % terms has improved from 13.2% to 16.7 % during the period.

However it lacks information on:

- The blue sign certification status

4 Likes

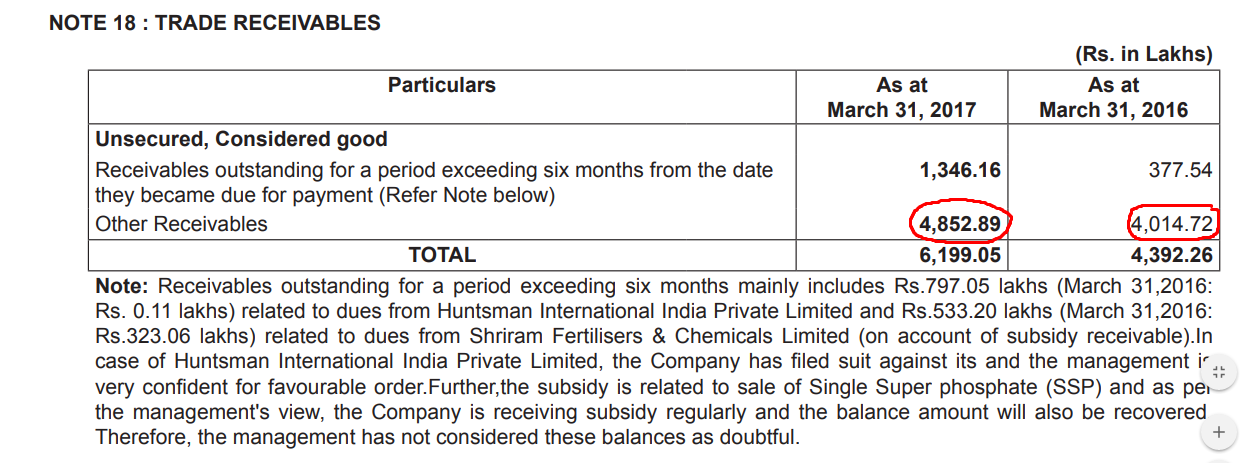

I went through the balance sheet and found that they are having Rs-61.99Cr(2017Ar) vs Rs-43.92(2016) as receivables, I am attaching the screenshot from the 2017AR , Can somebody clarify me why company has receivables of Rs-48.52 Cr. The company has given clarification about the Rs-13.46cr , but what about another Rs-48.52Cr. Companies products are good, so why so much high receivables? It will be great if anyone can come up with a good logic or am I missing some thing?

2 Likes

Dont look at absolute number. Better look at receivables as a % of sales or receivable days and then check:

- compared to industry

- Peers

- Self over years

That would give a clearer picture if this is good or bad

3 Likes

Thanx for the reply and can you tell me the other Receivables listed under in the above pic,What is the period for that receivable . Rs-48.52Cr for what period they are referring, is it less than 6 months?

Sorry for not going through the image in detail. please find my comments below:

-

Any receivable more than 6 month old is bad as chances of recovery reduces. Here, management has highlighted that this has gone in litigation. Also, you can see tht there is a 3 times plus jump in >6 month old receivable which is bad. The deeper risk could be if company does not have a prudent risk process where company should block sales to any customer if he has more than 3 or 6 months receivables pending. Assume if company has made more sales to this customer in last 6 months and that also turns bad

-

yes , other one is less than 6 months and it is important to ask management, out of this 48 cr, how much belongs to same customers who r holding > 6 months of receivables as it exposes these receivables also to similar outcome

sorry again for half baked reply earlier

Worst case scenario, may be you can factor in this as provisional loss in the model and see if it has what % impact on valuation if you are confident it is one time event for the company and wont repeated.

1 Like

Promoter bought from open market:http://www.bseindia.com/xml-data/corpfiling/AttachLive/10BAFF4A_1192_4AEE_9881_35825D31AE7E_151357.pdf

6 Likes

Thats a good news, they have bought 40000 shares, worth Rs-1Cr+

Last year the results had come out on 12th Nov and the announcement for the board meeting for results was done on 27th October.

The results seem to be delayed this year. Anyone has any idea why?

And here it is…

Dear Sir,

We wish to inform that pursuant to provisions of regulation 29 of SEBI (Listing Obligation and Disclosure Requirements) Regulations, 2015, the meeting of the Board of Directors of the Company will be held on Monday the 4th December, 2017 at 3.00 p.m. at 301/302, 3rd Floor, Near Udyog Bhavan, Sonawala Road, Goregaon (East), Mumbai - 400063, to consider and transact the following business:

- To consider & approve inter-alia the Unaudited Financial Results for the Quarter ended 30th September, 2017;

- Any other matter with the permission of chair.

Further, the Trading Window as described in Code of Conduct for Prevention of Insider Trading, will remain closed for all directors/ officers/ designated employees of the Company for the above purpose from 25th November, 2017 to till the expiry of 48 hours of publication of financial Result to the stock exchanges.

You are requested to take a note of the same and oblige.

3 Likes