@srvn

Thanks, I think you are on to something.

I am not sure as well, I first thought they have already issued shares but now learnt that they have not already issued shares.

Todays board minutes say of further preference shares issue at the low price

If true its not a good sign from the existing promoters.

Markets are down but I am not sure if the sell off in this script was due to mornings board meeting or general selloff across the market

1 Like

It is not newly issued shares. Out of total proposed 44lakh preferential issue around 32 crore got issued in last board meeting. So more than 100 crore came to books in September. The money they will be using in the new capex. Remaining 12 lakh shares will be converted later, may be in March or during the finishing stage of the project. Further the preferential shares were proposed around 6 month back and the guidelines for fixing price was followed and was allotted around market price.

Puneet, Hope you have attended the AGM yesterday. Please share the gist and important findings if any.

Please add some view those who joined Shivalik AGM this year.

Sorry for the delayed response.

I did manage to attend the AGM.

Sadly, I was the only investor present, remaining attendees were employees.

Found the promoters quite open and welcoming towards questions. The actual AGM lasted barely 5 minutes. Post the AGM, I had a one to one conversation with the Chairman and the MD. I found the Management to be quite conservative and rational, didn’t make any hi-fi claims with hefty targets.

Apologies for the unstructured notes, I’m writing whatever I’m able to recall:

-All the approvals for the Gujarat plant have been obtained and they will shortly announce the commencement of the construction.

-The plant will have 8 units and they are confident to get atleast 1 unit operational by Oct-19.

-The requirement for capex is huge even after taking in the recent pref issue of over 100cr. Management isn’t in favor of taking any debt for the purpose of capex and want to do majorly it through internal accruals and the funds raised.

-Strong focus on R&D. They’ve hired a new team of scientists for their new R&D center at Bhiwandi.

-They primarily want to ride the Make in India wave and want to focus on APIs which most of the Indian Formulation players import from China

-In the preferrential allotment, Pharmadanica(Danish pharma firm and other promoter of Medicamen) also participated through related entities which shows their confidence in the promoters

Disc: Invested and adding

8 Likes

Thank u for sharing the details. Is there any updates on progress of Oncology project of Medicamen Bio?

I didn’t get to discuss much regarding Medicamen. Though, in the brief mention, they said that the work regarding the oncology plant is going as per schedule and should be commisioned by early next year.

Another good news. Mr Shrawat played a crucial role in scaling up the sales at Shilpa Medicare from by 8x in his tenure. Hope to see similar feat by him at Shivalik.

1 Like

Wow a COO of shilpa joins a much smaller company

Usually for a good cv and your career you want to join a bigger company as there is also better pay, benefits, social prestige by being associated with a bigger firm which is another stepping stone for greater heights

Who would risk their career unless they were certain joining Shivalik is going to be more exciting and rewarding than a bigger company

Exciting times

1 Like

There may be other reasons also. May be he ran out of options.

Are u still invested

Could some one help me to understand without marginal increases in TOP line How EBITA EPS etc… Raising It need some digging

Dimethonate is old generic product with out substantial margins …Wil company sustained in long run or this is just another tulipminia ??? I don’t know

in 2014-15 AR they mentioned it

aslo in page 43 in AR

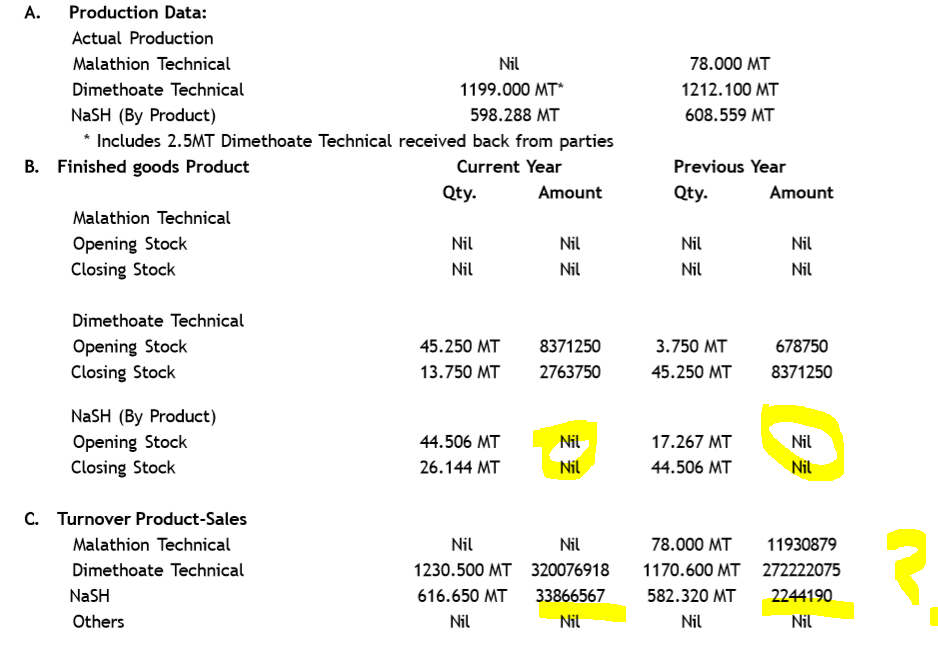

in page 60 of 2015-16 tax paid is in whole figures ??? it raise my eyebrow

in 2012-13 there is no valuation of finished product ??? I may be missing some link

in most recent AR they decorated Board of directors with

other wise majority are financial guys … of the Board … DO they Selling the AR… or Manufacturing GENERIC Chemicals … I don’t know …

24% increase of management remuneration in 2016-17 WHAT EXCEPTIONAL they have done ??? Diverging money i may be 100% wrong in my perceptions in Page 34 of AR 2016-17

I Diisc : i am not sebi approved analyst this is not any sell or buy recommendation .I do not own shares of the company .

3 Likes

Please go through the previous posts in the forum to understand their business. The insecticide business is now the secondary business for the company. The growth is driven by their subsidiary Medicamen. Major trigger here is the huge capex company has undertaken for API facility in Gujarat which is expected to operationalize by early next year.

Hi,

I have some queries about Shivalik’s new API business.

- Company manufacturing API to supply only to medicamen or they are going to supply other big companies also.

- If they are ready to supply other companies then it would be only domestic or other countries also.

It would be really helpful for everyone if anyone have any idea about it.

Thank you

1 Like

Company will sell API to Medicamen and others as well.

In terms of geography, I think it should be a mix of both domestic and exports, although heavier on the domestic side.

Thank you Puneetc for the clarification.

Company’s director Ashwani Kumar Sharma bought 12500 shares from market on Friday.

Positive news, also considering the current price is around 18% lower than the QIP price of 325.

1 Like

Shivalik rasayan ltd consolidating near 200-220 after it fall from 300-350 , stock accumulation is going on by big players . Good explosive growth ahead after API plant operational by DEC-19 ,also company planning to foray into speciality chemicals business as per website data…

Good longterm play.

Disc - Invested and adding slowly…

1 Like

One more thing …promoters have alloted share to themself at 50% higher price than CMP 220 Last year…one of the director also recently June 19 purchased in bulk from market

The new website looks refreshing.Q4-20 onwards, we might see additional Synergy benefits (Supplies to Medicamen) coming in as well.

1 Like