I am not asking for this,it is already shared and we are trying to find out why this selling. Since promoter is not responding so trying to take help of BSE to take out the information on this.

If somebody is aware of the process please let us know.

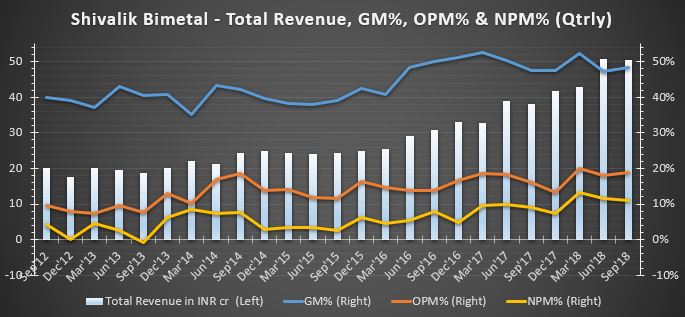

Growth in revenue of 29% from 125 Cr to 162 Cr. Growth in NP from 8.6 Cr to 13.95 Cr

Co was certified under TS16949 in Jan 2016 and now has upgraded itself

AEC (Automotive Electronics Council) compliant test facility was commissioned in previous year. This has allowed for development and successful testing of samples for automotive application, many of which are in final stages of testing and approval

Commercial Orders have already been received from leading automotive customers

Existing stamping facility is now in upgradation phase wherein new high speed presses are being installed. This will provide significant increase in accuracy, safety and capacity

Co has procured 2324 sq mt of land adjacent to existing facility. Construction work will start mid October 2018 and complete by July 2019. This will add approx 25,000 sq ft of additional area offering 3 floors.

UNIT 4 - as reported earlier relating to setting up of manufacturing facilities for capacity expansion, having obtained the possession of land, the layout is under finalization and construction is expected in March 2019 to be completed by Oct 2020.

R&D Expense this year is 1.45 Cr. 0.90% of turnover.

MDA:

Shivalik’s products are catered to broad spectrum of applications which include Switchgear, Energy Meters, Industrial & Electrical Applications, Automotive & Electronic Devices. We export to 50 Countries.

We are one of the leading manufacturers of Thermostatic Bimetal / Trimetal strips, components, EB welded products, Cold Bonded Bimetal Strips and Parts globally. We provide a complete solutions/package to the customer, not only of strips, but also of ready-to-use components.

Co continues to focus on improving yields, productivity and key strategic initiatives like automation and logistics automation.

Co is quite hopeful with opportunities in following:

Smart Meter - Co has developed products which are an integral part of meter

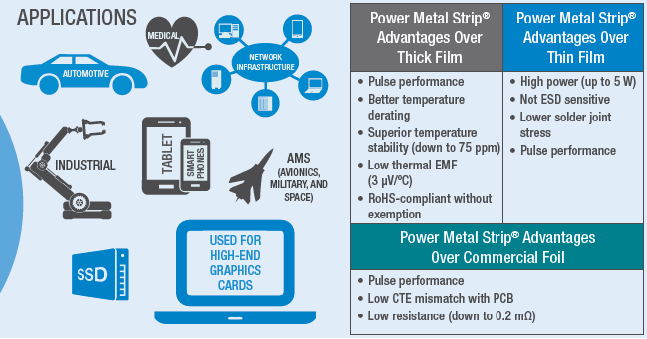

Automotive application - We have developed resistors which are used in high power low ohmic metals. Power resistors are used for automotive applications such as electric power steering, power window modules & IBS (Intelligent Battery System) of Electric Vehicles.

Snap Action disc: Company is venturing into niche application such as OLP (overloaded protectors) and thermostatic Bimetals of various industrial and home appliances. We are developing disc grade Bimetals for such applications.

My personal note - The co has shared the breakup of revenue and even given quantitative details. Its interesting to see that the shunt segment is growing at an exponential rate and has become a material part of business in just 3 years. Given that its being used in areas like Smart Energy meters and EV Batteries, its interesting to think of the potential

One of the promoters Gurbir Sandhu is constantly selling from 6.46 lakh shares in dec 17 it is down to 3.65 lacs now. Is this promoter actively involved in the business? If yes then this is a matter of great concern. If no then the reason can be personal and the share will move up once the selling is over. Can someone throw more light on this?

Regarding this, company was communicated over this mail id investor@shivalikbimetals.com.

There was no communication for 2 reminder. On stating I will take BSE help on investor non-communication ground they replied and pointing the same screenshot which I shared from bse site,saying it is informed to bse. No reason nothing.

Please raise concenr on this continuous selling and ask for the reason. Any answer please let us know over this forum.Thanks.

The concerned promoter selling shares is an inactive/dormant one. He has not been part of the active management for the last several years. He is supposedly shifting to Canada and requires funds for the same.

Received a very sayisfactory reply from th3 company. Excerpts from the reply given below.

Ms. Gurbir Sandhu is the wife of Mr. D J S Sandhu, Ex Deputy MD of the Company. Mr D J S Sandhu had sought retirement on health grounds and he ceased to be Deputy MD of the Company w.e.f 20th August, 2015.This fact was duly communicated to the shareholders through the Directors’ Report forming part of 32nd Annual Report( 2015-16). Mr D J S Sandhu and his wife, Ms. Gurbir Sandhu hold the shares of the Company in their personal capacity and trade the shares as per their personal requirements. These trading of shares by Ms. Gurbir Sandhu have nothing to do with the operations, functioning, promoters holding or deliberations in the Board of the Company. He is no longer privy to the deliberations held in the Board and or other statutory or other Committees of the Company.

Shivalik Bimetal – AGM 2018 Notes

(prepared by me, @ankitgupta and @yogansh)

We incorporated our company in 1984 and because of insurgency at that time we chose Solan as it was near to Chandigarh and the environment/temperature was conducive for bimetal manufacturing (need clean environment for bonding). Furthermore, Solan is a district head quarter and has all the infrastructure available. In addition, we got lot of subsidies for setting up a factory at Solan. Solan also has other advantage including low attrition rates.

We have built world class facilities for both bimetals and shunt resistors which is at par with any other global company. In fact one of our customer, the biggest switch gear company based out of France, remarked that our facilities and processes are like any other European company.

On Cathode Ray Tube (CRT) markets declining suddenly : CRT market declined suddenly. We had anticipated the obsolescence of CRT markets but did not anticipate the fall to be so quick. Even black and white TV sets had remained in the country for a long time post introduction of colour TV sets. Earlier they were the market leaders in CRT and one of the largest facility for CRT in the world. They were expecting that the CRT technology would be viable for another 10 years. However the industry quickly went down as many of the customers went bankrupt like samtel, BPL etc. Post obsolescence of the technology, they were left with huge capacities.

Shunt resistors : We started working on shunt resistors a decade back. We supply to electronic manufacturers which uses our strips and we also manufacture resistors ourselves. There are two major drivers for shunt resistor demand:

Energy meters : One of the biggest demand driver for shunt resistors is change in energy meters to electronic meters from magnetic ones. Most of the countries in Europe are changing to electronic meters including France, Germany and UK. Smart meters use sensor that are made of shunt resistors.

Automobile : The battery management system (BMS) uses the shunt resistors and there is increasing demand for that. BMS monitors the batteries in car. One eg of BMS is the car stopping automatically at red lights on traffic signal. It is currently being used only in expensive cars as its expensive but with BS VI emission norms coming in India even a small car like Alto will have to use it. This alone can lead to reduction in pollution by 15%. Furthermore, increasingly cars are becoming more connected and using electric components. A high end cars uses at least 300 motors. For EVs, the application of shunt resistors is much more important and critical as BMS plays a very important role.

Other applications : We are continuously working on new applications where shunt resistors can be used. For e.g. we are working for a chip manufacturer who supplies to smart phones. We have developed a resistor for the company where in the same size our resistor carries current of 1.3 Watts as against the existing 0.5 Watts. Ours is the most efficient resistor in the category.

In shunt resistors we were the first company to enter into shunt resistors. Gear and mechanical approval for vendors take at least 18 – 24 months while electronic approval takes 3 – 4 years. Last 2 years, we have been working on projects which will mature in 2020 – 2022. The project approval timeline runs for 5 – 6 years.

Our shunt resistor products are better than competitors because our bimetal/shunt strips have more power carrying ratio to size. The key is welding and bonding of metals. We are one of the most experienced welders in the world. It is not easy to buy an electronic beam welding machine and start manufacturing the products we manufacture. There are only 4 vendors in the world who can manufacture the low ohmic shunt resistors that company manufactures. There is lot of welding experience/competence required for developing the low ohmic shunts. This kind of expertise is available only with few companies around the globe. They claim to have welded highest number of kms among all the companies which has lead to gaining significant expertise in welding technologies. This experience/know-how of welding and bonding with varied materials is helping them.

We are applying for two patents – one for bimetal and one for shunt resistor.

We have acquired two lands – one land is adjacent to our existing facility while other is 1 km away. The expansions will come in two phases:

Phase 1 : The adjacent facility will be used for transfer of existing shunt resistor facility as well as for expansion. We will transfer our existing shunt manufacturing facility to the new one since we want to separate bimetal and shunt resistor facility. Currently, customer for shunt resistors who visit our facility perceive us as a metal company rather than an electronic company. The new facility will expand our capacity for shunts will double our existing 1800 MT capacity (around 3500 – 4000 MT). This expansion will be completed by Q2 of next year and will require a total capex of Rs.5 crore. We already have the machines with us and the capex will be only for buildings.

Phase 2 : The second phase will for expansion of bimetal facility and will be completed in 2020. The bonding capacity in the new plant will be much higher than our existing facility (185 mm coil as against 100 mm coil). This will also bring down overall costs. The total cost of capex will also be around Rs.5 crore for the new plant.

Bimetals which has seen low growth over the past few years will see higher growth because of new product application as well as expansion into new geographies.

Biggest customer contributes 14% of our total revenue (including bimetal). We understand the risks associated with customer concentration and are working to reduce that. Mr. Ghumman on the side lines told that over the next few years other customers whom they are in discussions with combined will become as big as our largest customer. They are at various stages of testing with them and expect approval in the medium term. Some of these customer will enter into contract with the company for 5 – 10 years. We started working for a manufacturer in 2015 and approval for commercial production is expected by 2020. The company is working with several auto companies since 2015-16.Many of them are in pilot stage and will go in commercialisation in 2020-21-22. These products will be in used in these models have long life of 12-15 years. The chances of changing vendors for shunt is very less until the company screws up in a big way.

Snap action disc which has applications majorly in geysers and is value added product. It’s a safety product and we are hopeful of making it successful. The testing for the product is rigorous.

High commission expenses: When you have MNC customers, they need a representative or an office in their country. We thought the costs of setting up offices is much more than hiring agents who represent our company. These agents are technology and marketing guys who understand the product well. Their incentive structure is based on the sales they bring. With exports expected to grow substantially, we expect that commission expenses will also increase.

R&D team: Mr. Ghumman leads the R&D team of 40 people. Mr. Ghumman divides his time between R&D and production. We keep on working on new products. On being asked what will happen after him, he said that his team is experienced and has been with them for a long time. They will continue to perform well.

Shunt resistors have better profitability than bimetals.

Why would a MNC company like to tie up with a small company located at a remote location like Solan? They have lot of respect for us. They have comfort and confidence on the owners. They know that the promoters are committed, have integrity and reliability. MNCs look at you with a microscope. They look at your financials as well whether you have stable balance sheet or not.

There is shortage for alloys with lead time of 6 – 9 months. However, we have established relationship with our suppliers. We treat them as a stake holder. Earlier we used to have one supplier but now we have three suppliers. Our customers also know our suppliers.

We have a natural hedge against currency as we have exports and imports. Over the next few years, our exports will be much more than imports. We have a pass through clause with our customers where we pass through increase in prices of raw material as well as depreciation of currency to them.

Kabir Ghumman has gone to China to test one equipment supplier for machines.

We have increased the borrowing limits due to ban on Letter of Credit imposed by RBI. We want to have additional limits in case of any exigency. Furthermore, we are working on a product with DBS Bank for our import requirements.

The company plans to growth by 15% CAGR over the next few years (they seem to be pretty conservative

Thanks for sharing the AGM notes, Couple of queries on this front,

Why customers prefer Shivlik Bi-metals against Chinese products? is it because of cost and quality or both?

What plans are there to expand beyond shut-registers products.

Will the new debt/borrowing will be used for new plant? does the new plant means maintenance cost increase and will reflect negatively for few quarters.

How is the dollar impact on Shiavlik as it is involved in both export and import.

Apologies for not replaying earlier. Please find below point wise reply for your queries:

Customers on shunt side prefer Shivalik’s products because of better quality. Although of a small value, it is a very important component for batter management system (BMS) in cars or even electric meters. Customer wouldn’t mind paying more for quality given its importance.

They have been focusing on finding new applications for shunt resistors and bimetals. For eg working with car manufactures to develop resistors for systems where the car automatically stops at red light. They have been working with defense for developing some applications. It is possible that some of these projects might not be successful but does reflect on the R&D capabilities of the management. All these might not fructify into confirmed order but does reflect on its product innovation and R&D capabilities.

The new plant cost as per management is just Rs.5 crore each for both the plants (for shunts and bimetals). It would largely be funded through internal accruals.

Shivalik imports alloys and exports its product as well. However, it has pass through agreements with its customers for rupee depreciation. It is a net exporter and might get some benefit from dollar depreciation.

Shivalik Bimetal Q2 Result updates

-Topline has increased from 38Cr to 50.53Cr yoy. A 31% Jump

-PAT has improved from 3.46Cr to 5.56Cr. A Jump of 60%. PAT Margins has also improved from 9.1% to 11%

-EPS has improved to 1.47 from .9 which is 63% up.

Half yearly basis:

-Topline has improved from 76.93Cr to 101.21Cr, its a 31.5% improvement.

-PAT jumped 56% from 72.7Cr to 113.6Cr. Margin increase from 9.4% to 11.2%

Overall a very goos set of numbers.

I expect company to post such number for another few years at least.

Co’s product plays an important role in applications (for example - EV BMS, smart meter, defense, etc) but represents a very small proportion of the cost of materials. Competition tends to be less on price and more on product quality. Once an analog device has been designed into an application - a process on which the original equipment manufacturer and the company often collaborate, it is costly for the manufacturer to replace it.

the article provides a glimpse of the mind boggling innovations going on in the chips and semi conductors space. though not directly related to shivalik, however its products are one among the many that go into making up the circuitry. can innovations be far behind in this area also?

Electric vehicles remain a distant dream in india but company is benefitting from EV demand in developed countries.In indian context,company has huge potential in area of smart meters.Replacement of traditional meters by smart meters to improve operational efficiency of discoms is one of the important component of UDAY scheme.Just last year,EESL floated 2 tenders worth 1000 cr for acquiring 50 lakh smart meters.Shivalik being only maker of shunt resistor in india would benefit from this push.

Very nice video which explains the potential of EV and how soon the adoption could be in developed markets.

With just a limited adoption of EV, Shivalik Bi-metal has already been a beneficiary. If the competition remains limited in the coming years (like it is now), company should be able to scale up well.