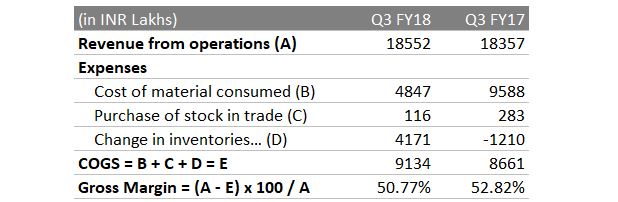

My old school type Gross Margin (GM) calculation follows. It says GM is down by 205bps to 50.77% in Q3 FY18 from 52.82% in Q3Fy17.

3 Likes

Any clarity on the 483 resolutions?

Pledging of shares by promoters

What’s going wrong here? Any insight into why Bhutada is pledging his personal shares for a personal loan?

Even at this price Shilpa medi is pretty expensive vs the sector valuations.

VAI Jadcherla from USFDA VAI: Voluntary Action Indicated. Objectionable conditions or practices were found, but the agency is not prepared to take or recommend any administrative or regulatory action.

2 Likes

Earlier status of formulations is maintained-no wonder the share rose from around 415 to around 460 over the last couple of weeks

Thanks for the update @MONK88888.

Shilpa Medicare has received Establishment Inspection Report (EIR) from the USFDA for its formulation facility located at Jadcherla, Telangana for the inspection carried out in November 2017.

Relief. Phew…

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/78c40cfc-6f0f-4836-9a55-444104447bce.pdf

1 Like

Can you elaborate ‘VAI’ to help me understand.

3 Likes

Any insights on Raichur API facility expected resolution? Is the Jadcherla FDA clearance useless without the API facility getting approved?

If a 10 point Jadcherla is resolved as VAI , I feel that API (3 points to resolve) should not be an issue. Since API inspection happened after Jadcherla , their CAPA would have been submitted thereafter. My guess is we should see a possible VAI in a month’s time. USFDA for JAdcherla was required to ensure that ANDA’s filed with respect to formulations get approved . Lack of EIR for API plants should not impact Jadcherla .

7 Likes

Shilpa sold it’s stake in loss making joint venture Raichem Medicare to other partner i.e. ICE.

Results are yet to be announced. Its on 28th May

results are out

Revenue is up YoY however profits are down YoY. Pressure on margins.

I’ve been monitoring some API manufacturers off late and their operating history over the last 6-7 years…What struck me when I saw the numbers of both Shilpa and Neuland Labs is that their gross margins have increased significantly since 2012-13 but none of the incremental contribution has reflected on EBITDA Margins…

The windfall generated has been re-invested into the business in the form of higher employee expenses. Now one way of looking at this would be that the companies are upping their compliance game and are hence hiring top notch professionals. Or the other thing would be that they simply lack the power to pass on these costs to the end customer.

Can somebody explain as to why this business would need so much investment in man power?

Attaching Neuland Labs as well for reference.

1 Like

Shivalik Rasayan is also entering in oncology. They have hired akshya chaturvedi from Shilpa and making state of the art manufacturing facility at dahej with capex of more than 100 cr.

Stock continues to look very expensive vs other companies in pharma sector.

Bounce in Shilpa due to its API manufacturing units in Raichur receiving EIR from USFDA:

SHILPA MEDICARE receives Establishment Inspection Report from USFDA to both API manufacturing facilities located at Raichur, Karnataka. The inspection has now been closed by USFDA.

— ShareDunia (@shareduniaindia) July 11, 2018

2 Likes

Management interview today - https://twitter.com/CNBCTV18News/status/1016941692543369217

The JV will be sold. So in a way the loss will stop. The contract manufacturing (in Shilpa) we were doing for ICE is at about 150 Cr and will remain at this level for next 2-3 years.

You had filed for 36 ANDAs - yes, 18 are ours and 18 are of customer. 2 approvals have come for us and 2 at customer’s end. expect 5-6 approvals in FY19.

Last year we did 35-40 Cr from US formulation business. This year we should be 4-5 times this number. This can go to probably 300 Cr in FY20

Yes, price erosion is there but we are in a segment where competition is lesser.

25 Likes