Great questions, Anant. Let me add to Ananth’s reply (disregard the overlap part please).

a) The co has an over reliance of sales on one single CRAMS product (ursodeoxycholic acid) currently; approx 50% revenue. This is sales to ICE Italy. Though a concern, the comforting factors are -

- Shilpa’s facility is ICE’s only facility outside Italy to source this product and

- ICE has entered into a JV with Shilpa

Indirectly tells us robust demand of ursodeoxycholic acid seen by ICE.

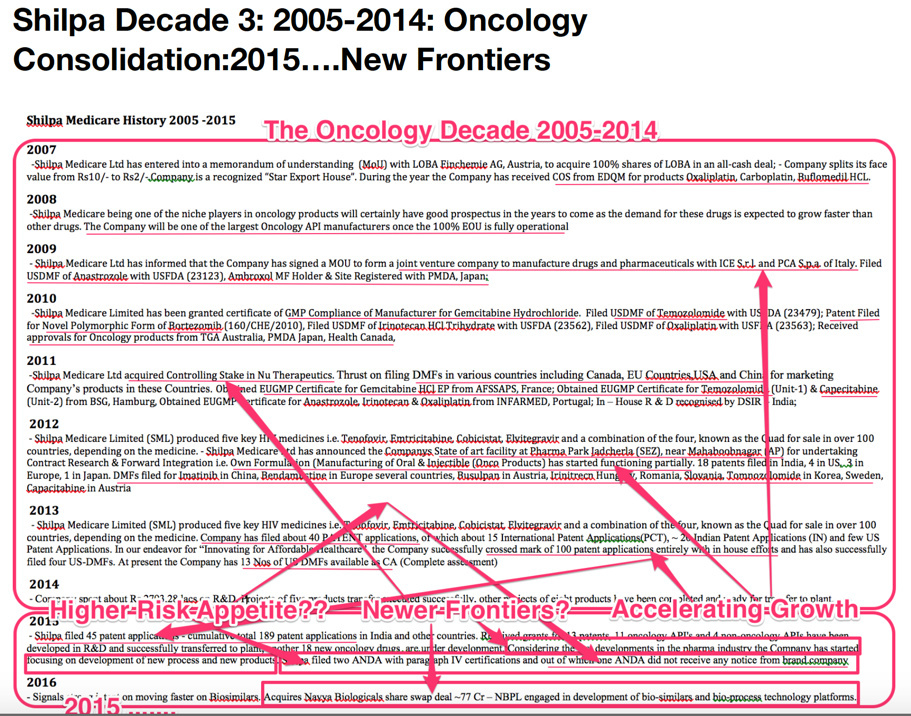

Coming to Oncology API - contributes ~27% of revenue currently. 80% of it comes from EU export. Its key oncology API customers are – Actavis, Intas Pharma, DRL, Cipla, Sun, etc. That said, the co has not reported growth in Oncology API revenue numbers (in recent past). Why? Probably because the co has been focusing on US market. Delay in USFDA approval has impacted linear growth path line. The USFDA approval for its API facilities has come in last few months - this should pave the way for growth in coming quarters.

Add forward integration of dozen+ formulation/ANDAs (EIR awaited), tells us huge scope ahead. From multiple streams with margin improvement.

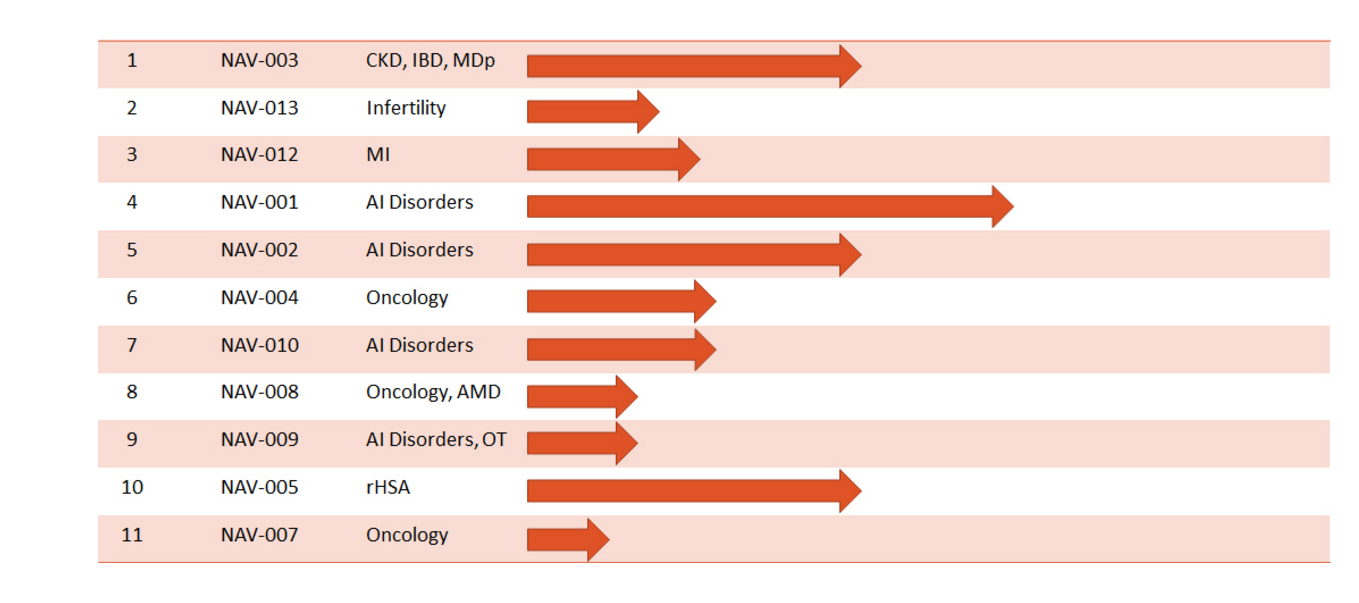

b) Oncology is a vast segment; multiple tumor types (unfortunately). Leukemia, Melanoma, Breast, Lymphoma, Lung, Sarcoma, Colorectal, and many more. Each having multiple molecules/treatments. Over the past 5 years, 70 new oncology treatments have been launched. I’ve draft chart (work in progress currently; will post shortly) showing in spite of 42 Oncology API in kitty (plus dozen under development), Shilpa has lot more to do to better its oncology coverage. Long runway ahead. In short, single oncology landscape, but multiple treatments/products in it.

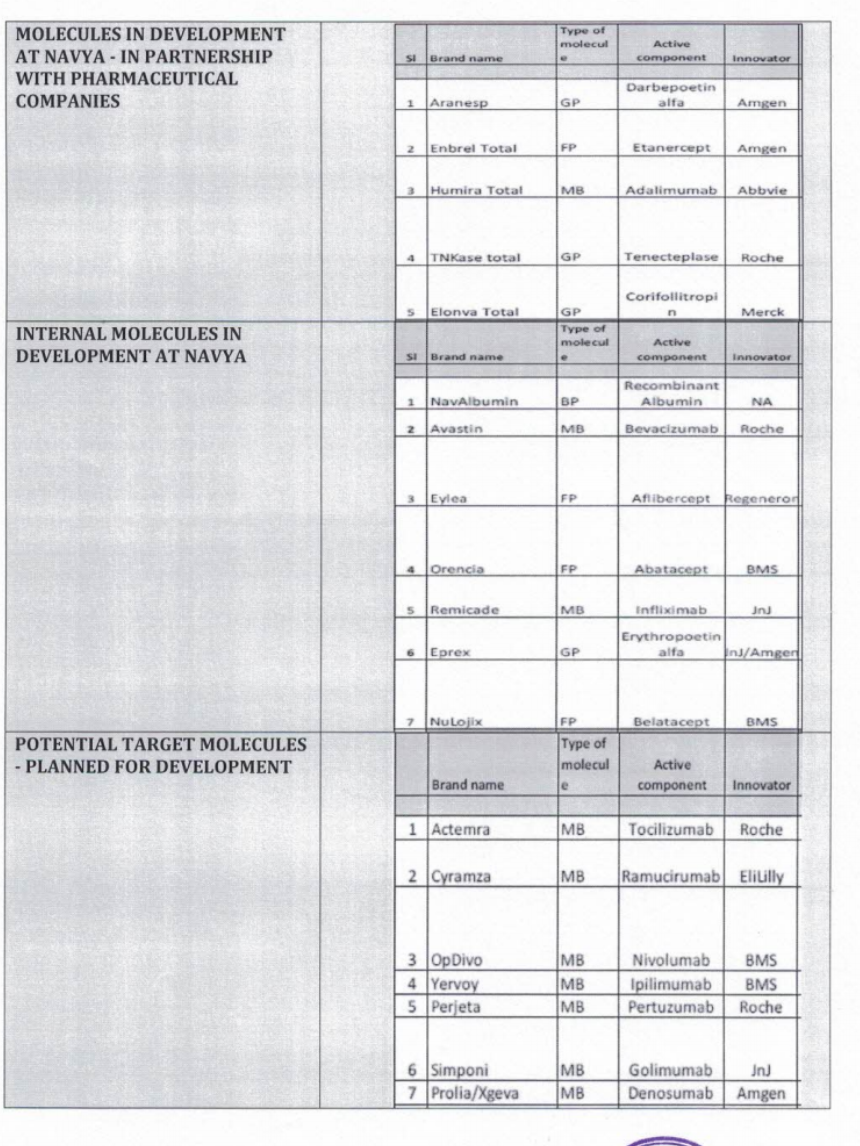

Many of co’s new investment via subsidiaries path appears non-oncology. e.g. Shilpa Therapeutics (oral disintegrating strip products), Makindus (ophthalmology and rare diseases) and Navya (biologics).

c) Other cos are visualizing what Shilpa visualized few years back (Disc: Holding Alembic, Shilpa & Torrent). Oncology cost growth is expected in the 7.5% to 10.5% range annually through 2020 when global oncology costs will exceed $150 billion. Smart cos want to have a sizeable pie of this niche area. Shilpa has got couple years of head start. Invested heavily in resource and capacity prior others. Hopefully now is the time to enjoy fruit of seeds sown years ago.

d) A very valid concern. The FY16 AR throws some light on action plan for the subsidiaries going forward. Seems the co has clarity on near term growth through Oncology landscape and is thus investing confidently in long term initiatives. Sowing new seeds for future. Somehow I see it as a sign of visionary management; thinking multi year ahead (am positively biased).

I’ve execution concerns with Shilpa. Jockey has been visionary. Question is - can the co convert patents, approvals and capacities into delivery numbers? If yes, then great time ahead. Just for high level comparison (not an apple-to-apple one) - another well respected Indian co generates ~4000cr revenue and ~1150cr PAT with just 49 DMF filling (mostly non-oncology) + CRAMS.

As Ananth mentioned, we should ask these questions to management.