Awesome notes @desaidhwanil . Gave me goosebumps.

2 observations/hypothesis, on your comments in the highlights sections of your evernote:

Highlight 1: “However, selecting which movie to air has become trickier due to lacklustre performance of some box office hits on television and bland performance of a few big budget movies. This has necessitated television broadcasters to become more strategic with their films acquisition budgets, significantly impacting the C&S rights of most films . While prices of A-category films continued to hold ground, the rest of the films took a beating either in terms of price or ability to sell the title. There were very few bulk deals and certain films, despite crossing INR 1 bn at the box office, were unable to find buyers. Nonetheless, industry experts remain optimistic on big budget movies, stressing that their C&S rights will still be bought but probably at a lower price”.

Your comment: This is a very candid view of the changing industry dynamics. It also implies softness in deal values. How does shemaroo construct portfolio to counter this?

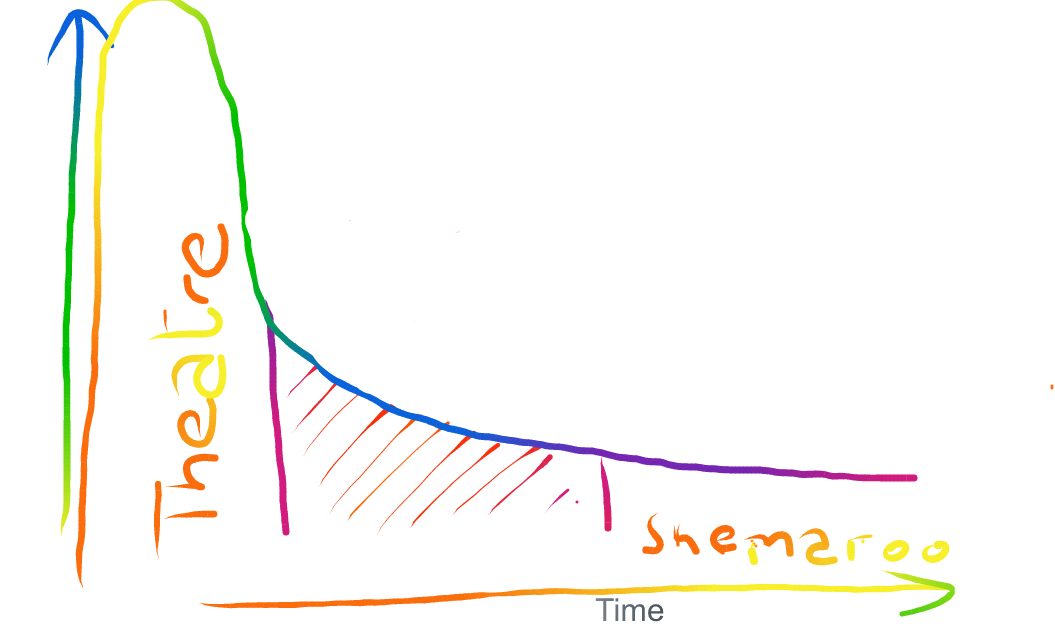

My hypothesis: If I use the help of a diagram of distribution of revenues, this is probably what it looked like 5-7 years before

The area under the curve is the total revenues generated for a particular movie across time. The middle shaded area represents the reveneus generated from non-theatrical section first cycle.

I think going forward, this is how it would start looking like:

There would be more such movies produced where most of the revenues from the first cycle would be concentrated in the theater release itself. Paying high premium for broadcasting/television rights won’t be a great investment. However, this would not really affect the second cycle revenue and it should probably stay stable, if not increase. However, the premium of the content rights for the second cycle might start coming cheaper due to lower revenues being generated from first cycle (excluding theatre releases). Businessmen might extrapolate the poor revenues generated from first cycle and give away the second cycle rights for cheaper rates in bundle. Given the experience of management of shemaroo, they would probably pounce on such deals going forward. I think this trend is not visible right now clearly, but going forward people would slowly realize this trend.

Highlight 2: “Share of video in Internet data traffic is expected to rise from about 41% in FY2012 to 64% in FY2017. In India, consumer Internet video traffic is expected to reach 1.4 Exabyte per month in 2017, up from 121 petabytes per month in 2012”

Your comment: So what is the CAGR?

My thinking: 1000 petabyte is 1 exabyte.

So 1.4 exabyte is 1400 petabyte. Thus CAGR would be (1400/121)^(1/5) ~ 63% CAGR.

One more thing which we can infer is that Internet data traffic would have around 50% CAGR as we have to take into account the increasing share of video in Internet data traffic (from 41% to 64%)

There might be a lot of inaccuracies in my judgement and calculation so please feel free to question my inherent assumptions.

Disc: Not invested, but tracking very closely.