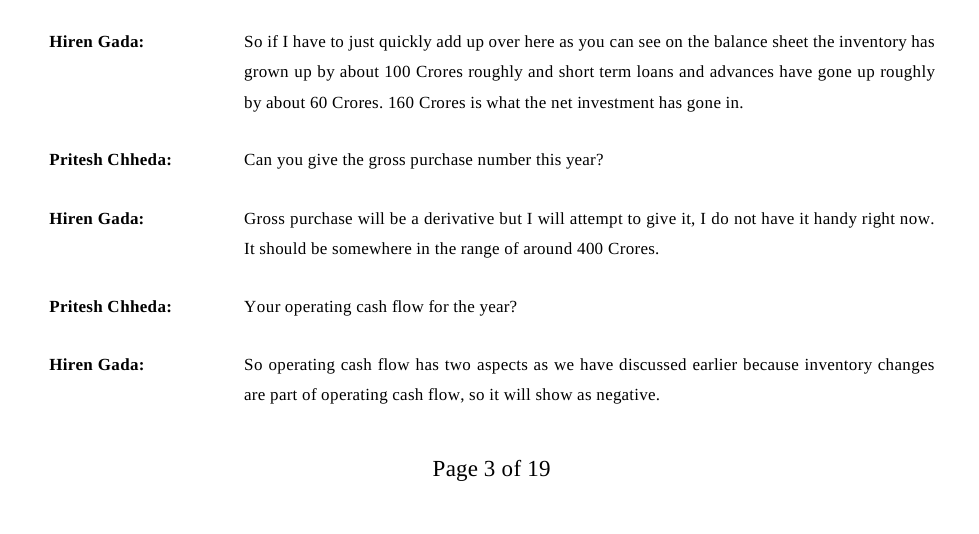

I was going through the conference call for Q4FY16

I could not understand the difference between Gross Purchase (400cr) and net investment (160cr) made by the company.

I was going through the conference call for Q4FY16

I could not understand the difference between Gross Purchase (400cr) and net investment (160cr) made by the company.

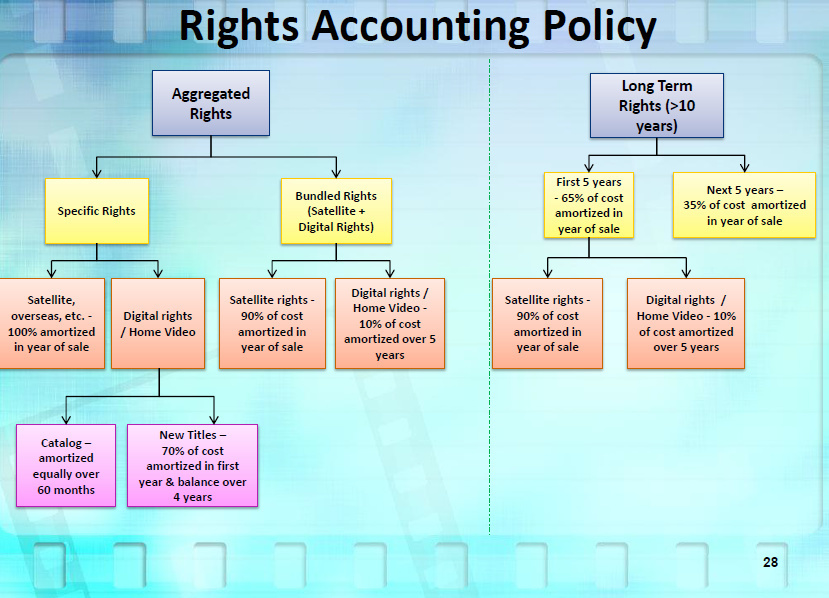

The company has accounting policy which is listed on Slide 28

From the enclosed slide, one can see that company follow different accounting policy for differnt business.

For instance, let us say it acquired portfolio of X No. Films (specific right only for satellite broadcasting), for Rs 50 Cr and assume that protfolio being sold to Channel Y for 65 Cr. In that case, as per accounting treatment, the company charge full value of Rs 50 Cr to P&L and there would no increase in March 31 2017 inventory. In addition to above, let say the company purchased perpetual right for portfolio of films for Rs 20 Cr and sold full portfolio to a media for Rs 25 Cr for 5 year. In this case, the company would charge only 65% of cost (Rs 20 Cr) i.e. Rs 13 Cr to P&L account would carry Rs 7 Cr as closing inventory. Assuming above two where only two transaction by the company, Inventory as on March 31 2017 would increase by only Rs 7 Cr.

So Net content purchase is only Rs 7 Cr, However, Gorss content purchase would Rs 50 Cr+ Rs 25 Cr = Rs 75 Cr.

This is what my understanding of accounting for the company and that is why there is difference between Gross inventory addition and Net inventory addition. In one of previous conference call (mostly after March 2015 results, but not sure), the company did mention that is follow certain milestone to classify inventory in book . At first stage, it give advance to owner of content which appear in Loan and advance on assets side. Once company legal due diligence is over, it shift from advance to inventory in its book. So in order to get total content purchase, in addition to change in inventory, inventory expense and short term loan addition shall give reasonable idea of Gross content addition. I shall try to collect that information shortly.

Hope this clarfify the issue. I also request other members to give me feedback in case my understanding has any wrong assumptions.

Regards

,

Thanks Dhiraj Dave @dd1474.

This structure makes me uneasy. It creates log of confusion in my mind. Do we have any idea, how business is doing?

Can we develop some metric from the data published by company to come to a reasonable conclusion?

Very difficult at least for me to anything from public domain. howver, past they did given some idea of content addition in gross and net terms.

Find enclosed interesting news appeared in ET disucssing better prospect for Hindi film channels vis a vis Hindi GEC for advertisement

http://economictimes.indiatimes.com/industry/media/entertainment/hindi-movie-channels-now-offer-more-entertainment-than-gecs/articleshow/53819425.cms

Also, recent tie-up between EROS and Reliance JIO

While first news I consider definitely positive for Shemaroo, as higher share in advertisement revenue for Hindi Movie Channels would also result in increased budget for content where Shemaroo is the largest players.

The second news is also giving positive direction about 4G launch and movies viewing. However, we do not have any idea about any tie-up between Reliance JIO and Shemaroo for content. Irrespective of the tie-up, entry of Reliance JIO shall definitely drive viewership of Indian film and Shemaroo may gain from online share/ advertisement share via youtube viewing.

Eagaly look forward to other members view.

Thanks, @dd1474, @crazymama, @myprasanna and others for contributing on this thread. I am Just putting out my brief investment thesis on Shemaroo. I have not covered the valuation part and request everybody to take their own view on the valuation. I find the story quite interesting as it has the tailwind of value migration of media consumption moving from physical sources to digital sources. If anybody is interested I can share the evernote compilation of Shemaroo work that I have done (mostly excerpts from ARs and Concall Transcripts with my annotations/observations) Please PM me and I will be glad to share the same.

Business Introduction:

Shemaroo was established in 1962 as book circulating library and over last 55 years it has transformed itself time and again to become a mainstream player in media aggregation and distribution business. It was established by Maroo brothers and is run by its third generation today. It is into three distinct businesses

(a) Content Distribution - focuses on aggregation and distribution of movie rights to broadcasters - Part of traditional media business- constitutes 75-78% of the revenue;

(b) New Media: Caters to distributing content on digital, mobile and over the top platforms- constitutes 16% of the revenue

© Home entertainment - part of traditional media business -constitutes 6-9% of the revenue

Content library- is the most critical component of the business which gets monetized through distributing the content through various modes. Company acquires two types of content rights (1) Perpetual rights - rights for perpetuity (2) Aggregation rights: Typically limited for 5 years, however lately company is trying to acquire rights upto 10 years. It has increased total rights from 2000+ in 2010 to 3600+ in 2016, while the number of titles with perpetual rights have increased from 500+ to 900+ in 2016

Company follows a strategy to generate decent risk adjusted returns and does not participate in higher risk businesses such as pre-release rights or the first cycle rights (first 5 years).It typically acquires content in the second cycle of the film distribution, i.e. five years after the release of the film, when the preference of the viewers is firmly established and economic value of the title can be established with reasonable certainty.

Business Model:

Content Aggregation and distribution: This is a cost plus model where company acquires the bundle of content rights of films from various produces/production houses and then does value addition by improving quality of content, the technical aspects,the legal clearances and packaging it to the TV channels in the manner they find it attractive.It then sells these rights to TV Channels at some mark up to cost. The critical success factor in this business is to identify the compelling content for viewers, acquire the same at reasonable price and create a portfolio of content that balances volume and quality of content that is appealing to the broadcasters. Company ensures that they generate at least 18% pre-tax IRR on the content acquired and distributed through this business. Company books 100% revenue from the sale when the content is sold to broadcasters. On expense side, if it is aggregated content, 90% of the cost of acquisition is booked (rest 10% is attributed to digital rights) as expense at the time of sale of content. For perpetual rights, in the first year of first cycle of re-selling (first five years after acquisition), 65% of cost of acquisition is booked while rest 35% is booked in first year of second cycle of re-selling (Year 5 to 10 after acquisition). This business has high receivable days i.e. 160-180 days.

New Media business: Company distributes the content in digital form through various ecosystems such mobile, Internet and Over-the-Top broadcasters. The digital content rights are typically acquired along with the content distribution rights for broadcasters. Though, company may acquire separate digital rights or creates its own content and distribute through new media platforms, it is not a common practice. There are three separate modes through which the content gets distributed in new media business. Here the content is chopped/churned creatively to form targeted short and long form contents (i.e songs/comedy scenes/movie in 15 mins) thus increasing the monetization potential of the content. Dynamics of two main ecosystem for new media businesses are

Mobile: 50% of new media business comes from Mobile VAS and other forms of content consumed by the subscribers of telecom companies. This is a mostly subscription based revenue where the user pays for the content. Company and telecom operator share revenue in proportion of 30-40:60-70 if the content is hosted on telecom operator’s platform. If the content is hosted on Shemaroo’s platform, the revenue share is 60-70% in favour of company. More and more content is migrating from Telecom opertator’s platform to Shemaroo’s platform.

Internet:50% of new media business comes from this stream. 66% of this stream (i.e. 33% of new media business) comes from Youtube. It is an ad supported model where Youtube shares 55% revenue it receives on advertising on Shemaroo’s content. Company runs number of channels with different type of programming (Comedy scene, songs, full movies, regional language content, kids content, devotional music etc) and gets viewers for its content.Company has achieved phenomenal growth in viewer ship on this platform with total monthly views reaching 120 million in Q4 FY16.It has 4-5 channels in top 100 most viewed Youtube channels in India. Other than you tube, the revenue comes from over the top players like Hooq, Spool, Airtel Digital, Tata Sky etc. Both these models largely works on revenue share models (though have different variants within that)

New media business has been growing at 60-70% and is likely to grow upward of 50% due to multiple tailwinds such as increasing penetration of smart phones, internet and migration from low speed to high speed (2G to 3G/4G).

Margins in this business is higher than consolidated margin of the company (28-29%), and there is enough room to increase due to operating leverage available in the business.

Receivable days in the business range from 60-90 days.

Home Distribution: This business in declining mode as the consumption is moving from physical media to digital media. Typically a low margin business because of high fixed cost involved. Overall contribution to the business has been reducing (23% in FY 10 to less than 10% in FY 16) and this trend is likely to continue in future too.

Investment Rationale:

Business

New media business is likely to grow at 40-50% for next 3-5 years (it has grown at 70%+ CAGR in last few years albeit on much smaller base) due to number of tailwinds such as increasing internet and smart phone penetration and high speed internet becoming affordable due to launch of 4G services by Jio at rock bottom rates. The high growth in New media will come from combination of volume and realization growth.The volume growth will come the above mentioned tailwinds as more viewers consume content. The rationale for increased realization is that higher number of consumers of content combined with increase in average engagement level (time spent on viewing content) will lead to higher monetization of views (i.e fill rates) and increased realization of CPM rates (currently in India CPM rates are USD 2 to10 per CPM for top Youtube partners, the same is USD 10-40 for other countries. Though India may not reach the level of developed countries any time soon, directionally it will move towards that number…thus CPM rates will increase as digital penetration will increase).

Traditional media business on the other hand is likely to grow at 13-15% in base case scenario considering the strong catalog of the company, continuing preference of Indian viewers towards movie as content class and consistently increasing movie channels leading to higher demand for movie rights . However, in traditional business too, the tailwinds of better financial resource availability with broadcasters due to increased ARPUs and lower carriage fees combined with inherent demand supply mis-match for quality content (demand far exceeding supply) is plausible. This has not been built in the base case scenario and any gains from that shall be taken as upside. . Home Entertainment business will continue to decline and hence for next couple of years will take away 1-2% of growth in traditional media business.

The differential in growth rate in both the business stream will lead to change in business mix. Revenue contribution of New media business will rise from 16% in FY 16 to 40-50% in next 4-5 years. Since, margin in new media business is much higher than traditional media business and there is still decent operating leverage available in New media business to take its margin higher- we can see decent margin expansion for next 3-5 years. Similarly, asset utilization efficiency too will eventually increase as New media business has lower receivable days and earns higher yield on inventory.

Based on above base case scenario, we can expect 20%+ CAGR in top-line and significantly higher bottom line growth (upward of 30% CAGR) with much better return ratios (upward of 20% RoE) due to twin filip from higher margins, increased asset utilization efficiency and tapering off of investment phase toward end of 2018.

Management

Management has demonstrated its ability to time and again transform the business to remain in sync with changes in consumer preferences and emergence of new technologies (Book libray to video library to CD/DVD distribution- broadcast right syndication- new media). More importantly, they have managed to pull these transformations off while taking a well calibrated approach where they run small experiments/pilot projects and the scale it up based on response to their pilot projects and changes in external environment. Management is also extremely focused on risk. They continue to trade path of generating adequate returns without taking undue risk as is evident from their unwillingness to participate in pre-release/first cycle of content aggregation and distribution and disinterest in infusing significant capital in film production business. Management has demonstrated its ability to take rational decisions even if it means acting counter cyclical or not bowing down to industry imperative. In 2008-09, they refused to participate in buying new content and suffer loss for a year against buying content at irrational prices due to entry many big corporates in content aggregation business. They were willing to bear short term pains for doing what was rational decision that will pay off in long term.

Thus, there is high probability that management will do a god job at capital allocation. On corporate governance, they have been reasonably candid in projecting the picture of business through their communication. Feedback from reference check on promoters is very good.

Scenarios for Valuation and Expected Returns:

Base case scenario- Bottom line growth of 30%+ as articulated in the investment thesis- probability of this scenario playing out is 60-70%. Fair P/E multiple in this case will be 20 times forward earnings

Scenario 1: There is 20% probability that New media business grows at much lower pace of 25-30%. In this scenario, the earning growth can be in range of 20% and hence the P/E multiple is unlikely to expand.

Worst Case scenario:There is 10% probability of losing money from here in case if company acquires content at very high price and then is not able to monetize it.

Variant View on the business:

The variant view on the business is that the cash flow from operations is negative and hence company is not making any positive cash flows making the business model unsustainable. Though this is true at the moment, the reasons for the same are threefold.

Interesting view point

Company has increased perpetual rights library from 500 to 900+ over last 5 years. Perpetual rights library gets expensed out over 10 years. However, the value of perpetual rights keeps on increasing. Typical increase in the value of perpetual library is at 12-15% CAGR (as indicated by management in commentary). Thus, after 10 years of acquisition, the accounting value of perpetual rights become zero, while the economic value of perpetual rights will increase by 3-4 times. This will help increase the margins and return ratios. A large portion of perpetual rights are acquired post 2006, hence significant part of positive impact from this is likely to come in next 3-5 years. The economic value of perpetual rights will also provide downside protection to the value of the business as it will keep on increasing.

Key Risks

Company’s inability to acquire meaningful content consistently can impact its standing with broadcasters and hence mean weakening of its competitive position.:

Likelihood: Low ; Impact: Moderate

Euphoria around the content monetization can drive many players to market (like 2008-09) and can jack up prices of the content to irrational level. This may lead to capital mis-allocation and/or sharp reduction in business volume in short term.

Likelihood: Moderate; Impact: Moderate to High depending upon scenario

Likelihood: Low; Impact: High

Discl: 7% Allocation with Average Buying Price of 240

I am not a research analyst/investment adviser and the portfolio here is not a buy/sell recommendation in any manner. Please do your own due diligence before taking an investment decision.

Dhwanil,

Excellent post highlighting all issue in one place. While aware about the issues (except economic life and cashflow for perptual content), putting it all in precise and concisely bring out investment rationale in right perspective. Also appreciate and share same risk factor, i.e. Negative cashflow and bit of hope that the company would be able to leverage on content with increased smart phone penetration. My holding is around 3% and I shall attend AGM. Do let me know in case any one have any queries.

Regards

Dhiraj

Hi Dhwanil…

Would like to understand this in more detail…

When they say they are building inventory now, are they acquiring content which is old (> 10 years old)? Or is it content created from recent years??

In media content always gets created at the same rate, so ideally they should be acquiring content at the same rate all the time if valuations are reasonable.

So why should they slow down after 2018?

Your thoughts on this??

Hi,

As I have received many PMs for sharing the evernote doc, I though it may be better and easier to share it on forum. Here is the link

It is a very pertinent question. Though, my sense is it has nothing to do with the vintage of the content. Typically Shemaroo participates in the second cycle of the content monetization which happens 5-6 years after release so most of the content will be older than 5 yrs.

My interpretation of they being in investment mode is: they are creating inventory faster than they are monetizing thus creating excess inventory that can be monetized in future either through traditional media or new media. This also implies that their yield on inventory is lower than normalized yield as they are not monetizing the content at the same rate at which they are building inventory.

However, this is my interpretation/understanding of the business and it will be good to get it clarified from management.

Hi @desaidhwanil,

My query may be an extension of Hiten’s query on the basis of your above response.

I have had a very small tracking position in Shemaroo since last year from 245 levels and have been contemplating adding depending upon available liquidity.

I was more interested in Eros Now to begin with but then Eros Now was owned by Eros PLC (the Indian listed entity didn’t own it) combined with corporate governance issues in Eros put me off. I was drawn towards Eros Now (despite Shemaroo’s larger content library) purely because of a view that quality of its content would be much better (it being new age production house and owning rights for lot of new content).

Shemaroo’s performance (ability to monetize its content) till now kind of answered my reservations (be the reservations right or wrong) on the quality of content.

But, could you please provide your views on the below, which was the other question that I had in mind:

I had a view that Shemaroo may not be able to generate decent cash flows if it has to keep acquiring content like it has been doing. Mgmt. comments on going slow on content acquisition and generating free cash flows going ahead added weight to my view. BUT I didn’t factor what you have stated that their pace of content monetization maybe slow right now.

My query is do you think they would have been able to generate decent cash flows in the below 2 scenarios:

A) Scenario where content acquisition goes on at current pace but pace of monetization increases?

B) Scenario where content acquisition goes on at current pace but despite this cash flows will improve substantially few years down the line as most of the cost of acquisition is amortised in the earlier years itself?

Cheers.

Hi dhwanil

On the content aggregation, the aggregation rights seem to be 5 years and the company books revenue at the time of sale and expenses 100% of the rights cost. So in effect, for this segment of the business, investment in inventory is more like an opex than a capex, unless the rights can re-sold to another broadcaster within the 5 year window. In some of the conference calls, the management acknowledged that this is more like a trading business.

If the above point is true, then the current margins seem to be over-stating the free cash flow by 1-2 %. In such a scenario, the unleveraged ROE seems to be 11-12%.

The new media business with lower recievables and OPM of around 30%, could give an unlevered ROE of 14-15%.

As a result i am unable to arrive at a path of how the company can reach a 20% Free cash flow based ROE ?

Am i missing something in the above calculation ?

In one of the concalls management has clearly said that in last 1-2 years, significant part of their spend on inventory is on digital rights. Now in digital rights, the content gets monetized continuously and incrementally and not once (as it happens with broadcasters). Another peculiarity of digital right monetization can be back ended because of the tailwinds of higher penetration of smartphones/internet and higher internet speeds. Another interesting point is (And this is again hypothesis) that once you get higher volumes - it leads to higher realizations too in digital media…further accentuating the monetization.

Similar thing happens for perpetual rights too…that rights that you have acquired perpetually…and hence paid higher value for it(reflected in higher inventory value)…get monetized in chunks but 100% expense gets booked in 1st and 6th year (65% and 35% respectively). Thus the cash out flow and inflow from monetizations are not in sync.

So, I feel in Scenario (A)…there will be free cash flow generation that is depressed currently will improve going forward even with the current level of content acquisitions. Also, we have to keep in mind that off lately, they have been acquiring content for longer period (10 years instead of 5)…so they are paying cost upfront for 2 cycles (reflecting in inventory) which will get monetized in year 1 and Year 6 (At much higher value). On Scenario (B), what you are saying may be case for perpetual content and some longer period deals (10 years aggregation) but not for 5 year aggregated content.

Having said that,I also agree that inherently it is a business model where you need to keep on investing in content from time to time and put in capital to keep growing. So, it is not a business model which will gush out tons of free cash flow. However, what matters is if they keep on generating decent returns on their incrementally invested capital. It is like a business model of Wonderla/Divis where you have to keep on incurring capex to grow and then generate decent return on it.

What you are suggesting would be true if they sell the monetize the inventory within short time of acquiring it. Though sometimes it may be the case, sometimes it is not. They call it “warehousing”. So, when they “warehouse” inventory and monetize it at later date, it becomes Capex if time period between acquisition and monetization is large. Else it can be viewed as Opex. However, we shall also consider that they acquire other kind of rights too…such as perpetual rights where you pay upfront higher amount… and then monetize it over a long period of time. This is of nature of Capex. Even for the separate digital rights that they acquire…or the value that they pay for digital rights along with conventional media rights…it get monetized over a period of time incrementally and continuously…and not in one shot. So, the nature of spend there too is like Capex. Hence, it may be a combination of Capex/Opex depending upon when and how the right gets monetized.

Now, the only problem is to quantify the proportion of the above mentioned categories of monetization as we do not have break up for them. However, considering the substantial additional value that one pays for Perpetual rights and the fact that digital content monetization is back ended may balance out the margin bump that may come from aggregated rights.

Also, if we take the same logic, the capital deployed too shall be lower for the current level of profit as certain portion of capital is tied up (as reflected in inventory) but not fully monetized…this is especially true for perpetual content. So, considering this, I feel the ROCE may look depressed because the assets are underutilized and hence adequate profits are not reported against its profit generating capacity. So, let’s say perpetual content that is 10 years or older, goes of the inventory and is fully expensed out after 10 years, will result in margin improvement when monetized…which is largely uncaptured as most of the perpetual content acquired is after 2006 and the 10 years period is still to get over.

On calcualtion of RoE, my assumption is that New media business is making higher than 30% margins (as said by management in one of the concalls) and they expect operating leverage to increase it further. In fact, under blue sky scenario they expect it to be around 40%(management commentary in one of the concalls). Now consider a situation where they earn 35% margins and the asset turns too increase (due to lower receivables in new media business and the proportion of new media business rising to 40-50% in next 4-5 years), combined with decent leverage can lead to 20% ROE.

Of course, there are a few assumptions here and we will have to be watchful of how things play out on some of these key assumptions.

Hi,

This is my long(ish) post on valuepickr. So, please bear with me.

I have recently been reading the Shemaroo annual reports from 2011-12, I focused particularly on the management discussion and analysis section.

Do we know how the distribution is done? Let’s pick up a random movie called X. Shemaroo allows Zee Cinema to broadcast X on a particular day. And if Zee Cinema wishes to broadcast the same movie next week, will they pay Shemaroo again? Meaning, in what manner/way Shemaroo monetizes on a particular film over a period of time, across multiple channels?

I checked the projected size of TV industry for 2013, 2014 and 2015 from the AR of 2012-13. The size of TV industry in later years consistently outperformed by a small margin the projected size by a small margin. I take this as a sign that the size of the TV industry (where Shemaroo operates) and Media and Entertainment industry will largely remain in line with projections.

Now TV industry is supposed to grow at CAGR 15%, reaching INR 1098 billion in 2020. Increase in subscription revenue and strong advertising revenues will be the driver.

Could there be any reason of TV industry not growing? Assuming advertising revenue grows, what happens if subscription revenue doesn’t grow? Then the ARPU of MSOs will be low, which in turn can affect the broadcasters, cascading to Shemaroo? May not happen, but wondering.

Shemaroo is a unique player in the above mentioned scenario. It enters after 5 years of release of a movie. Apparently they do not want to enter in the first cycle and that is why they are increasing their library. Broadcasters have to show movies, but if they don’t know/couldn’t decide/hesitate in airing recent blockbusters, then they may have to go to firms like Shemaroo who owns movies. Therefore which movies are bought by Shemaroo and whether they become successful in monetizing those movies, are key.

This assumes:

i) Broadcasters do not buy recent blockbusters or buy in less quantity.

ii) Production houses jack up price of new big movies, causing broadcasters to step away.

Another scenario may be that Shemaroo picks up content management role on behalf of broadcasters. I don’t know whether this is something the company is willing to do.

New TV movie channels mean possible advantage for Shemaroo.

Do we know how much revenue is earned by English movie channels compared to Hindi movie channels? A case can be argued that if people watch more English movies, then Shemaroo will not be the beneficiary. However, MSOs don’t provide English movie channels at base subscription. Hindi movie channels always come with base subscription.

Other than cable TV, DTH penetration is something to be watched for as well. How is Shemaroo’s relationship with DTH operators like Airtel/Videocon/Dish etc?

Shemaroo earns money by giving broadcasting rights of movies to TV channels. It buys a movie from production house after 5 years. Correspondingly the revenue of Shemaroo is dependent on:

i) Revenue of the movie channel - consists of ad revenue and subscription revenue

ii) Revenue of the parent broadcaster - consists of ad revenue and subscription revenue

iii) Broadcaster’s relative revenue from movie channel - if a general soap opera channel gives more profit, it might happen that ads will flock there and not in movie channels.

No of broadcasters in India is 350 and no of channels is 780.

A very good explanation of TV industry value chain is given in page 33 of 2012013 AR.

BARC rating of channels is something to watch for. The new rating system can influence ad revenue.

There used to be a section in management discussion, called 'Significant factors affecting our results of operations. It is available in page 24 of 2011-12 AR, page 35 of 2012-13 AR and page 21 of 2013-14 AR. Not a single word was changed for this section in all three years, i.e. the same words were repeated, punctuation by punctuation. Could risk factors stay same in 3 years and could it stay same in exactly identical manner?

The section got dropped from 2014-14 and 2015-16 AR. No explanation is given in AR.

I haven’t went through the numbers yet.

Disclosure: Small holding in Shemaroo.

if this is true , this is in contrast to as stated in 1 of the annual report , where they wait for 5 yrs after launch and than buy the content for a long period of cycle

We typically wait for the movie

rights to finish its first cycle of five years

and gauge its performance.

We play the high volume strategy

where the risk is spread over large

compelling content.

They buy rights for 2nd cycle which is 5-10 years but those rights are bought much earlier say in the 2nd or 3rd year, once the commercial viability of the movie is established. So I don’t think there is any contrast. By the management commentary they mean that they don’t buy rights for 1st cycle and restrict themselves to 2nd cycle. But those rights by themselves are bought in 1-2 years of film release.

@desaidhwanil thanks for the reply. i am unable to find the extent of warehousing on aggregated content. on the perpetual content i agree with your point. i guess we have to track how the capital intensity on the new media reduces going forward

The big risk here is: We are all going by what the management says. Management does not disclose much, and we can’t really gauge if they are hitting the internal IRR target of 18% on new investments.

It’s a great business otherwise, as others have explained. (operating leverage, perpetual rights, CPM tailwinds)