3rd February’17, Mumbai: Shemaroo Entertainment Ltd. appointed Zubin Dubash as COO - New Media Business. He will be responsible for driving the New Media business and scaling it up.

Zubin Dubash is a Senior leader with 20+ years of success in managing businesses in mobile applications, telecom, and digital domains. Before joining Shemaroo Entertainment Ltd, he was working in the core team of Apps Daily Solutions, as Chief Product & Strategy Officer and played an active role in product creation/innovation, strategy and Strategic partnerships. Prior to this he was at Tata Docomo as Vice President/Group Head- New Businesses. He has also worked with companies like Vodafone etc earlier.

Shemaroo signs licensing deal with OTT player Viu for content. OTT based

entertainment is gaining traction. Looks like digital and new age channels

are about to grow much better for Shemaroo.

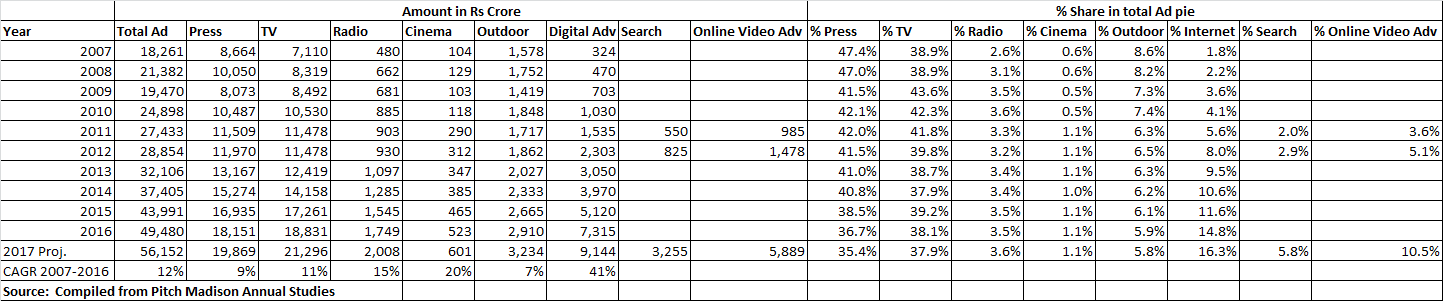

Some more interesting data about Overall advertisement for India (being projected at around 13% for CY 2017) with Digital advertisement forecasted to grow at 25% in CY2017 reaching to Rs 9,144 Cr. The growth rate in digital advsertisement is expected to slow down from 43% in CY 2016 to 25% in CY2017.

Interesting to read impact of Demonetisation on Advertisement spend in Nov-Dec 2016 and also full recovery in advertisement spend by April 2017.

Shemaroo Management did highlighted lower ad spend as one reason for lower growth in Q3FY17 in conference call as per my memory.

Over the years, Share of digital advsetisement has increased from 1.8% in CY2007 to Projected 16.3%. Within a decade, it has become third largest category for advertisement, just behind TV and Print Media advertisement.

While the data for non-search (or online Vido streaming) is not differntiated for all the years, growth of search advsertisement is growing at lower rate then online video advertisement. In projection for 2017, Online Video ad would account for 10.5% of total ad spend while search ad would be balance 5.8% of Digital ad. Since Shemaroo fortune are directly linked to Video advsertisement, it would be interesting to see till what time Digital advertisement record around 25-30% growth rate as industry.

Thanks for digging. Looks very interesting. Yes, management had indicated in concall that even for digital advertising, demonetization had a strong impact. This data corroborates that. More interestingly, I find that Online video advertising is gaining lot of traction and that is likely to continue in CY17. This kind of validates what Shemaroo management has been saying that with increased internet speed and falling rates for data usage, Online video consumption will benefit the most. I think online video advertisement spend is a very good proxy for the rising consumption of video.

‘The film Mirza Juuliet is produced by Falansha Media Pvt. Ltd and is being presented jointly by Shemaroo Entertainment Pvt. Ltd and Green Apple Media.’

I got this from one of the filmy site. It’s not entirely clear if they are co-producing it or what’s the arrangement.

Since on conference call managment clearly said no new investment/film in past, I would look forward to next quarter call to get more understanding on the subject.

Hello Friends,

Some excellent points have been already discussed here. I hope to add some incremental value.

I am writing down some Pros and Cons of this investment idea and hopefully you can provide your thoughts on them.

Pros:

I asked myself what is so compelling about Shemaroo? What value does it add to its customers and suppliers and what stops its customers and suppliers from short circuiting Shemaroo? Part of the answer could be that it’s a highly fragmented market- many suppliers (Content Providers) and many customers (media channels). So its hard for Amazon to have many conversations with Red Chillies, Nadiadwala, Balaji and the likes for procuring content. It would be easier for them to talk to say 3-4 sources such as YRF, Dharma and Shemaroo. Likewise for a content producer, it may be distracting and expensive to have a sales team and a legal team to form alliances for selling rights. A company like Shemaroo makes it easier and even less expensive for both parties; Shemaroo has said that it has good relationships with both sides, one that has been cultivated over decades. Plus, having sold rights for thousands of movies, they probably know the legalities much better than others. These softer issues make Shemaroo a valuable, trusted and needed partner. In one of the Annual Reports (2011 I think), Shemaroo had said that 60% of the content gets sold directly between content creators and channels and only 40% is Shemaroo’s addressable content space. In 2017, with more OTT players coming in and more small content creators, I think Shemaroo’s value would have only gone up. And these intangible strengths don’t show up on the Asset side of the Balance sheet; its kind of hidden.

The management in the Annual Reports and Concalls,have said some of the following: a> admission of mistakes b> talk of love for the business c> discipline to walk away from deals that they think are not going to be profitable. I am fairly new to investing and I don’t know if these are genuine feelings or mere sound bytes.

And like what has been already discussed, I do think that in 2020 and even in 2025, there is going to be a demand for quality entertainment. Even more so than in 2017. However, I think the regular Star, Sony, Zee kind of channels would need to offer more and more on demand content. Entertainment is not a team sport and people that are used to watching content anywhere anytime any device will be more demanding. So I see a big shift coming where people may stream more more content from mobile/ tablet/ computer onto the TV for viewing. This content may very well be saas-bahu serials, but I think I’d rather watch it at a time and place convenient to me than the chosen by the channels. So a big shift in consumption behavior and preferences. This may affect TV channels but not content aggregators like Shemaroo.

Cons:

Does the Management have an unlisted company that competes in the same space, leading to conflict of interest? I found a mention of this in this article, but I don’t know how to verify it.

There are a lot of loans from the Management to the business. This information ins available in the Annual Reports. I think in the long run, this can be lead to a source of conflict of interest.

In the very first discussion, there have been mentions of the Promoters being directors of companies that defaulted on payments.

Would love to hear your thoughts on these.

Disc: I am quite interested but not yet invested in it.

Good write up… Thanks…

In addition, the data consumption in India has just started. There is a

long long runway for it. And in the coming few yrs, the on demand

entertainment on personal devices such as smart phones will grow

exponentially. And shemaroo, even if it takes a 0.5% share will do very

well. You rightly said - the demand is guaranteed in the many yrs to come,

and it can only grow exponentially…

Have been tracking this for some time to enter at a right price.

Of late, it has been on a downward trend. Does anybody have any information on whether there is any change of plans by the promoters?

At the current and future trends, this is one of the company’s which has a

potential to have manifold end users. Due to cheaper mobile data plans,

many OTT players, cheaper 4 G phones, and the structural change of having

the entertainment in the hand palm. In my view, even in case company is

unprofitable, the sales will continue to grow thereby making its MC/Sales

always look good. I read that the promoters are making a film and that

could be a reason for recent downtrend. Not sure what kind of a film they

are making. With Q4 results expected in Apr/may, the company should get

back to the good times and nos.

Disc: Invested and have it as 3% of my portfolio…Views may be biased…

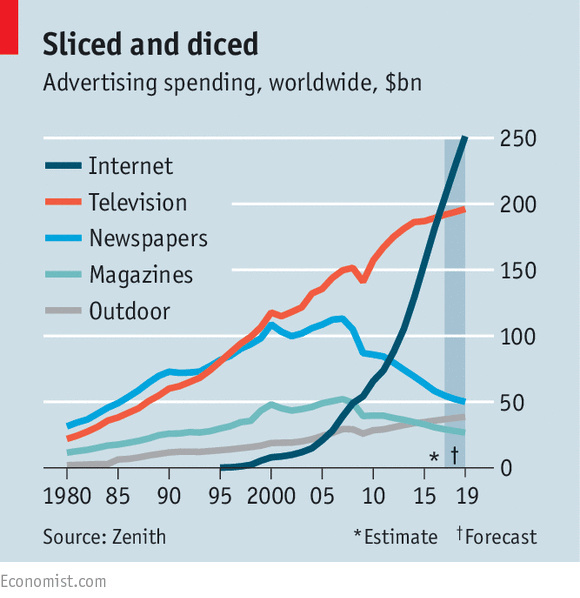

Interesting perspective on Digital advertisement. During CY2016, US Digital advertisement spend has exceeded TV Adv. However, there are certain issue about Youtube and the major customer. Find enclosed economist article on the subject.

Well, Shemaroo has formed an inverted cup and and handle pattern on the charts. Occuring in an uptrend this pattern suggests some sort of bearish sentiment present and prices are most likely to be heading down. However, in a bullish market ive read that these patterns fail. Overall they are reliable though. Also the prices tried to push through the tops at least on 7 to 8 occasions but were not successful. I think for those have a positive long term view about the business should watch the prices closely because i believe that they are on their way down and then buy at lower levels.

If you look at my previous posts, i have always maintained that libraries are good business but shemaroo is overvalued given its scope and scale. But will definitely become more attractive as market cap goes down. Definitely an opportunity at much lower levels.

Appreciate your efforts and observation. Since I do not have any technical expertise, I would not like to comment on that aspect.

For me, more concern some was no major growth in new media in December 2016 quarter and release of some new movie tailor. I would still wait for March quarter as slow down in December quarter could also be due to domenitisation impact. In my previous posts, I did put across report about digital media spending being declined during November December 2016 period.

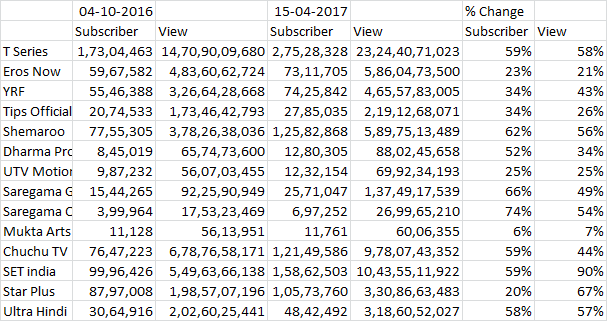

My evaluation of Shemaroo Youtube viewership is enclosed for Key channels over the time and I find that Shemaroo viewership growth has been reasonable over last 6 month or so on Youtube.

Find enclosed my compilation of Youtube data for some Key channels of Youtube over various date:

As one can find, from October 16 to April 17 period, Shemaroo and Saregama have registered the highest subscriber growth. Also, while in viewership data also, Shemaroo growth of 56% during the period, compares very well vis new movie content owner such as Eros now at 21%, YRF at 43% and Dharma production at 34% (even after release of Babubali 2 Tailor)

So, what I infer is that Nostalagia has its own power. Old is still Gold.

On second point, the management did mention about not more than 2% of balance sheet would be exposed to New film production. The Trailor of new film might be forming part of 2%. However, we need to wait to get management revert on same.

Discl: I have invested in Shemaroo and investor shall undertake its own due diligence before investing. My view may be biased due to my investment.

and people that are used to watching content anywhere anytime any device will be more demanding. So I see a big shift coming where people may stream more more content from mobile/ tablet/ computer onto the TV for viewing. This content may very well be saas-bahu serials, but I think I’d rather watch it at a time and place convenient to me than the chosen by the channels. So a big shift in consumption behavior and preferences. This may affect TV channels but not content aggregators like Shemaroo.

and people that are used to watching content anywhere anytime any device will be more demanding. So I see a big shift coming where people may stream more more content from mobile/ tablet/ computer onto the TV for viewing. This content may very well be saas-bahu serials, but I think I’d rather watch it at a time and place convenient to me than the chosen by the channels. So a big shift in consumption behavior and preferences. This may affect TV channels but not content aggregators like Shemaroo.