Sharda raises funds, looks they will repay the high cost funds from promoters (10%).

Con call transcript, company confident about the cost to either remain steady or tend to come down, no more escalation. China market, according to management is turning from sellers market to buyers ( more suppliers are available), looks the bad time is fading away. NAFTA region performance is very good and regarding trade war between US and China, Trump will try to avoid farmers as they are his vote banks and if he does, prime victims will be Chinese companies.

I was looking at this company because the following seemed nice

Agrochemicals space is currently growing fast due to exports picking up and this company exporting to US and NAFTA, LatAm countries was a big plus

P/E of 18 for a company with 20% Sales growth and 22% Profit growth last 3 years (as per screener).

RoCE of 49% and D/E of 0 looked excellent.

Promoter holding of 75% as well was a big plus.

It ticked a lot of the boxes in my checklist but these kept me out.

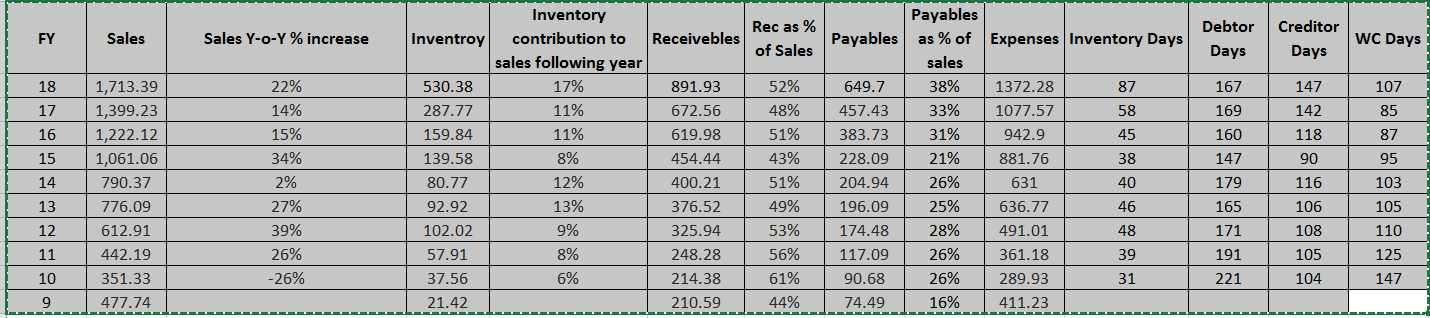

FY17 to FY18 PAT growth has been nil despite topline growth of 22%

OPM dropped from 23% to 18%. Effect due to Crude?

Inventory increased from 287 Cr to 530 Cr between FY18 and FY17.

Receivables at 892 Cr (672 in FY17) with the inventory pile-up means this company is having trouble managing its working capital.

This is apparent when looking at short-term loans - Its now 170 Cr from being nil in FY17. So the D/E of 0 doesn’t hold anymore.

Receivables + Inventory - Payables i.e WC was 500 Cr in FY17 and is now 772 Cr. That’s quite a big jump.

Debtor days was 175 days in FY17 is now 190 days so the deterioration in receivables isn’t proportionate to sales.

Inventory turns was at 4.87 in FY17 is now at 3.2. There is a clear deterioration on all things related to working capital here.

I think this balance of old positives and new negatives are captured in the price as well beautifully as it rests on FY15/FY16 top. The H&S pattern could breakdown if the market doesn’t see signs of improvement going forward or the support could hold if the inventory build-up is justified by the sales going forward.

The whole asset on balance sheet is intangible asset. In a FmCG kind of scenario, the brand gives comfort regardimg the true monetary value of asset. How do you derive that comfort here ?

Sharda neither manufacture nor develop anything rather they buy where is cheap and sell where pricier, that is what Sharda call themselves " Asset Light Model" company. The only real asset Sharda hold is " registrations" and this model generates profit with out much investment. The risk part is, any country/region can keep Sharda away but not a developer/research company. The story is same for generic pharmaceutical companies which enjoy the cheap cost of production in India.

OPM was dropped due to the crack down in China due to pollution control causing lesser suppliers which

continued through out FY-18 and definitely, as you mentioned, crude has played a part.

2.Expecting a good Q4 high inventory level was build up in Q3 ( Con call Q3) and Q4 , capital was borrowed

(short term )from promoters ( Con call Q4). Company has posted ever best Q4.

3.Inventory turn over remains high , probably expecting better Q1-19 or as you observe longer receivable

days which is a cause of concern. Q1 and Q2 inventory levels will provide better idea about receivables.

I am also waiting for Q1 to make sure the worst is behind us.

Current price scenario, most probably is due to, utterly negative sentiments prevailing towards mid/small cap stocks which may continue until FIIs turns positive.

As far as Sharda Cropchem is concerned, the expenses of procuring a licence to distribute its products ( registrations ) are put on the balance sheet under the name Intangibles. These are an integral part of their business and are also part of the capital employed in the business. These need to be included in calculating the return ratios.

This counter is looking attractive at recent levels. My query in screener is mentioned below. Evidently a fundamentally strong stock. Any particular reason for hitting the lower circuit? Tried to figure out through surfing the recent news. Couldn’t find anything specific.

YOY Quarterly sales growth > 10 and

YOY Quarterly profit growth > 10 and

Market Capitalization > 1000 AND

Average return on equity 5years > 20 AND

Promoter holding >= 40 AND

Sales Last Year >= 10 AND

sales growth >= 10% AND

Debt to equity < 0.1 AND

Average return on capital employed 5Years >30 AND

EPS last year >20 AND

Return on equity > 20 AND

Net cash flow last year > 1

I have done some analysis on Sharda and what I found is that while their receivables are always remained at 50% of sales where as payables as % of sales has been consistently increasing. This shows the confidence of business as suppliers are confident of taking the money back with delays. Also, WC days has been reducing consistently every year.

FY18 was exceptional due to Chinese government strict regulations lot of manufacturing firms had shut down. In last con call management mentioned that things are turning around and working capital should be back to normal.

HDFC recently increased the stake to around 7.8% while CRISIL report shows that things are on track to achieve sustained growth in medium term. This is backed by increase in number of registrations in pipeline (978 vs 852).

The IPO analysis on business line said that some registrations are in the name of proprietary firms of promoters. Also promoters have stake in group companies in same line of business.

Any change in this position? Somebody can raise this issue in investor meets

The overall gross margins declined mainly due to lower gross profit in European and NAFTA markets

The net working capital days stood at 113 in H2FY20 vs 102 a year earlier

Net cash balance at Rs 199 crores in H1FY20

Participants

Adinath Shares

HDFC

Spark Capital

ASK Investments

Edelweiss Securities

QnA

In NAFTA region winter got extended which resulted in lower usage of agrochemicals and similar was witnessed in Europe

The import duties have been increased in the USA which has not been absorbed by the customers

The import duties have gone up from 6.5% to 25% in some categories on imports from China into USA. The customers are unable to bear this increase so the companies are bearing the brunt

The management is expecting good growth from European markets in Q4FY20

The Chinese producers have been affected due to lower off take in USA and closure of factories due to pollution issues. The management is expecting newer facilities to come up from next year

The capex for FY20 will be between Rs 150-175 crores

The prices increases have been few and costs have been on an upward trend due to which company is facing pressure on gross margins

The management feels that China will still remain factory to world and new manufacturers are not good in terms of quantity or prices

The company still continues to be dependent on China

The forex losses are on account of fluctuations in exchange rates

The management has paid the suppliers as on due date which has been as per the past policies

The company gets 180 days credit from banks for payments to suppliers

The management already runs a tight ship on fixed costs and there is no room for further improvement

Degrowth in European business, NAFTA business and rest of the world impacted revenues

Gross profit declined by 31% yoy and gross margin contracted by 474 bps manly on account of challenging market environment in Europe & NAFTA

Net working capital days stood at 84 days vs 59 days yoy

Participants

• Edelweiss

• ASK Investments

• SPARK Capital

• HDFC Mutual Fund

• IDFC Securities

• Oldbridge Capital

• B&K Research

QnA

Signs of revival are better in Q4 and expecting better performance in the upcoming quarter

The spring weather is appearing to be good and order book position is looking favourable

The trade wars have had a big impact on sale of agrochemicals in the US markets

The prices of technical’s have been stable and in some cases have been declining but demand from farmers have been lower due to higher taxes

In Latin American markets growth is coming from Brazil & Ecuador markets

The rates are lowest in the 3rd quarter and as Chinese customers start purchasing in the 4th quarter the prices start inching up

The restrictions on Chinese factories for production have been eased and now supply is greater than demand

The capex done as on 31st Dec 2019 was Rs 121 crores and for full year basis capex could be around Rs 150-175 crores

Expecting Q4 performance to be similar to last year on a yoy basis

Expecting gross margins to touch levels of 40% overall going forward

The pipeline is good and continuously investing in newer registrations and also receiving them

The market situation is difficult because 75% of market is controlled by 4 distributors and rest market is being fought over by the generic players

Won’t tinker with the business model as of now and core business of getting registrations is working well and expecting better performance in the future

The number of products in the pipeline are 1013 as of Dec 2019

Working capital going forward will be in the same range

The company cannot manage at similar levels with MNC’s and cannot give high credit period like the MNC’s

Procurement policy has remained same over last 2-3 years and the procurement policy should have a positive impact on Q4FY20

Will continue with the older tax rate due to a lot of incentives that remain

Sharda cropchem is not only agro chemical company Also has non core business like industrial belt and conveyer belt business . I believe market doesn’t like non core business . That’s the reason of low PE. But company in highly regulated market like europ and niche product asset light but still market expect something

Current CFO Abhinav Agarwal resigned. Sharda Cropchem has had 4 different CFOs since March 2015, the last two CFOs have lasted less than 12 months each.

I find the operations of the company quite complicated. It has 41 subsidiaries in multiple countries. Bulk of these subsidiaries are operational which means sales happen in multiple jurisdictions (about 35% of their sales comes from sales of these subsidiaries) with implications of taxes related to sales and on profits in each of these countries. It would require quite a large set up to deal with these issues and optimise the tax liabilities as well as deal with multiple currencies and manage the forex part and also deal with regulatory filings in each of the countries.

While scrutinising the accounts, I was trying to figure out the cause for fall in ROCE over last few years. The company capitalises its cost for product registrations and also amortises the same fairly aggressively. But its very clear that while the company has been able to create new product registrations and licences at a fast pace the sales have not kept pace.

Rs in crs

FY15

FY16

FY17

FY18

FY19

FY20

Sales

1061

1222

1399

1707

1998

2003

Net Block

88

130

210

226

372

416

Sales/ Net Block

12.06

9.40

6.66

7.55

5.37

4.81

As a result while the intangible assets have gone up along with the balance sheet size as well, the sales and profits have not kept up. Unless the company is able to drive sales from its license portfolio ROCE will not improve and that is clearly reflected in the stock price.