It depends how we want to justify our bet. This is like unilateral way of looking at things. Selling from non promoter classified and buying into promoter classified holding is just a case of syndicated trade.

Hi, This is clear case of circular trading. Also good way to display it. Can you tell from which source did you get this informative graph? Its very helpful. Thanks in advance

You can use Tofler to find out about these private entities and how they are related

This seems to be an orchestrated case and the management seems to be compensating themselves not just for running the business but also the stock prices. Had listened to the management during a concall in 2015 when they were discussing a QIP and the attitude of the management was very poor. I would try to dig that out and put up the transcript. Also looking at the fundamental performance over the last few years this seems to be walking a tightrope. Also can someone explain why they pay no cash taxes. There seems to be too many discrepancies between statements and actual facts.

Kenneth Andrade of Old bridge capital buys 1.48 lakhs shares ( 0.8%) of

Shakti pumps in a bulk deal on 31st July 17 in NSE at Rs 476 per share…

http://www.kslindia.com/equity/bulk-deals.aspx?id=13&EXCHG=NSE

1 Like

Good to know that. However, as Rakesh Jhujhunwala always says at the end of discussion, I reserve my right to change of opinion, probably Kenneth may also say after 12-24 months. If Kenneth doesn’t, then all investors shall be happy.

The point is not about to who invested. In many cases in 2003-2008 boom, you find creamiest investors invested in not so great business. At current price, Kenneth see value and investing. However, that does not give comfort with the kind of action management shown in past.

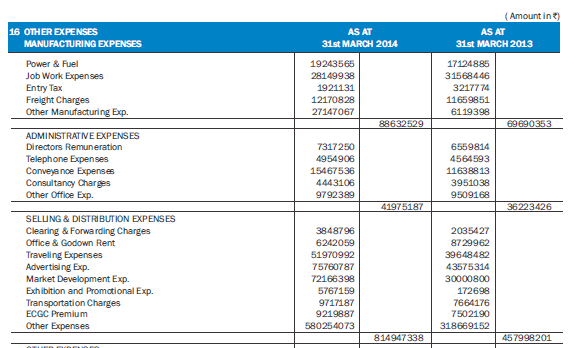

Enclosing schdule 16 on Page 55 of annual report of FY2013-14 for Shakti Pump

On Total sales of Rs 296 Cr during FY14, the company has other selling distribution expense of Rs 58.02 Cr i.e. more than 20%, With Total Selling expendture of Rs 81.4 Cr i.e. 27.5% of sales. Only this fact itself was sufficient for me to decide whether to invest in the comapny.

Finally, everyone has its own risk profile and investment style. It does not meet my investment criteria but that does not mean no-one should invest. I have my limitations and I work in area determine by my limitation. Wish all the best to everyone who has invested in the company.

12 Likes

Shakti Pumps had a great run from 150 odds to 550 majorly on its solar pump business optimism. Even though i am positive on the company on its future growth, the valuations according to me are all built in into the story and is trading at crazy valuations.

Disclosure - Have booked 50% profit at current valuations.

Stallion asset recent management meet:

2 Likes

"Having considered all the facts and circumstances of the case, I, in exercise of the powers conferred upon me under Section 15I of the SEBI Act read with Rule 5 of the Adjudication Rules, hereby impose a penalty of `1,00,000/-(Rupees OneLakhonly) on the Noticee i.e., Shakti Pumps (India) Ltd., under the provisions of Section 15A (b)of SEBI Act for failure to make the disclosures within the specified timeline. The said penalty imposed on the Noticee, as mentioned above, shall commensurate with the violation committed and acts as a deterrent factor for the Noticee and others in protecting the interest of investors. "

Today during review my holding in Shakti pumps, read annual report, very rosy picture. Validated by following presentation from International Solar Alliance. ISA have start price discovery for 5 lac solar pumps at 10000$/pump. That only coming as opportunity size of 3.25 lac cores. This is about only solar pumps, they have traditional business of normal pumps.

As rightly pointed out by members, promoters may be siphoning money in terms of other expenses/ related party, but when I compare other expense for FY17. Shakti have approx. 20% of sales as other expense, KSB have approx. 24% of sales as other expense. May be this is the standard in this type of company. But if solar pumps get traction then company can benefit exponentially. Of course stock, increased multifold, but looking at future, opportunity size is HUGE.

Appreciate from fellow members to point out, what I am missing here…

http://isolaralliance.org/docs/ISA_03_August_2017.pdf

Disc: Invested since 4 months

Mics. Expenses Written off of 23.94 cr is given in FY17 Consolidated Cash Flow Statement. Anyone knows any detail about these expenses??

This seems a BIG opportunity if it goes through.

Kenneth increasing stake in the company after announcement of this scheme. https://www.pradhanmantriyojana.in/kusum-yojana/

http://www.aceanalyser.com/Conference%20Call/131431_20180131.pdf

Shakti Pumps India Limited Q3 FY18, Earnings Conference Call”

1 Like

35 entities had manipulated the share price of Shakti pumps as per SEBI.

https://www.sebi.gov.in/enforcement/orders/sep-2018/adjudication-order-against-35-entities-in-the-matter-of-shakti-pumps-india-ltd-_40291.html

With KUSUM Yojana taking off one can see a sustainable 25 to 30 % growth in the company for a long period of time of 5 to 7 years.

I expect the stock to re rate from this level

The Company has come up with Q2 results and probably it seems that they have now started getting the benefits of KUSUM. Consolidated Sales during Q2 is Rs 237 Cr as against Rs 469 Cr during entire FY 2019-20.

Q2 300920.pdf (662.7 KB)

4 Likes