Results… One time gain… Leads to profit of 300-400 crores… in books

Highlight being US exports started…

Sequent is on it’s path to become market leader in VET API…

Europe profits and revenue growths look healthy at 40%

Exited sequent with an avg selling price of 120. Recently it collapsed to around 47. Have re invested in other stocks not planning to re enter sequent. It may give a good return from these levels in 3 years provided they are able to show consistent profits.

What is your rational of posting your selling price around 120? This would have been long ago. Why post now when company has posted a good set this q4?

1 Like

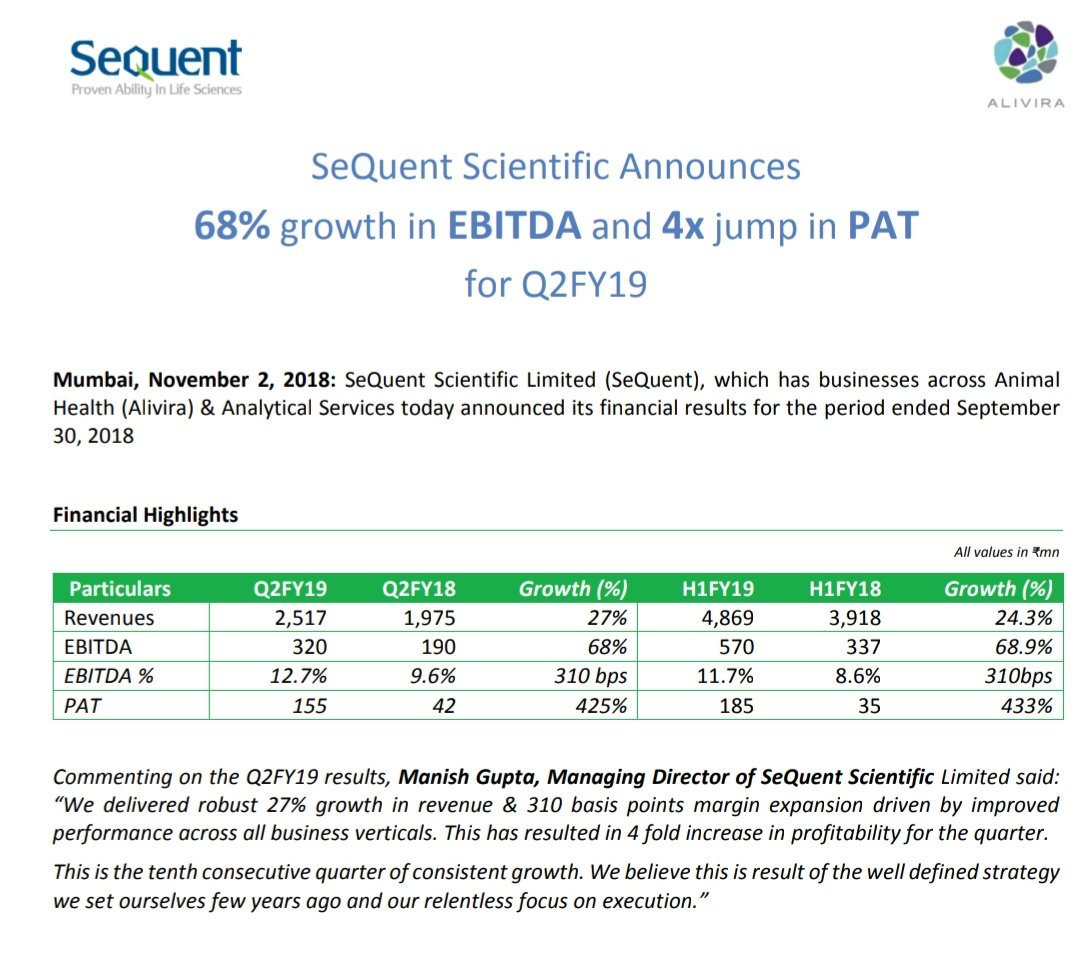

Concall Highlights:

Key: In FY19, the formulations business should continue to grow driven by volume growth in existing products, new launches and geographic expansion, while the API business should also benefit from better pricing driven by entry into the US market and an overall favourable pricing environment.

EBITDA margin: was up 200bps YoY. EBITDA margin is sustainable and poised to improve over the coming years. Other than Turkey, there is immense scope for improvement in EBITDA margin across other geographies. Company has grown 18% yoy in the European market where industry growth was in single digits.

German acquisition: Bremer Pharma will be consolidated into SSL’s business from 1QFY19. Immediately, Bremer Pharma will be leveraged for its presence in emerging markets, while in the medium to long-term the intention is to leverage Bremer Pharma’s facility for commercial manufacture of injectable products being developed by SSL at its R&D facility.

API business: It is on a positive trajectory and SSL will be looking to replace API sales currently in emerging markets with high-margin US sales. Overall, the macro environment is also favourable for API pricing. Real be from US to come in Fy19,20.

LATAM: Animal health business is already generating positive EBITDA and it is closer to the critical mass that will allow further expansion in margins.

Tax rate: expect the tax rate to decline going forward as the company’s business becomes profitable across geographies.

Capex: There is enough capacity to meet near to medium-term growth requirement. Capex of about US$5mn may be incurred in FY19, which will be mainly for maintenance and debottlenecking activities.

Good days back at sequent scientific. The old bull market from 2013-2015 saw a huge jump in the share price from sub 100-1200 levels. After that a huge collpase thanks to exorbitant valuation (PE over a 100), and excessive merger and demerges etc. Now, the new company is looking in fine shape, the mess of the human api demerger is over. Most importantly, all promoter group companies like solara and strides are running we’ll independently - management has sharpened their focus. Biggest takeaway from sequent is to expect an FMCG type play in animal health industry. Market leader in India.

Disc - Invested from 50 levels.

5 Likes

Manish Gupta, Sequent Scientific: Targetting 15-18% Topline Growth; 200-250 bps bps Improvement In Margins Going Ahead

16 API Filings In The USFDA In Animal Health Space

U.S. & EU Will Continue To Be Critical Markets For Both API & Formulations

1 Like

Animal healthcare company SeQuent Scientific eyes Ebitda growth of 200 basis points or more in fourth quarter.

1 Like

Hi All I am really confused about the data of company i can understand because of demerger no one is showing correct data but can you please guide me where i can find the correct data i can see in bse in march they got 300 crore extra profit is it maintainable or one time income?

That was one time gain on demerger. It’s not sustainable income

So that mean they will have an EPS of around 1.5 whole year ? and to the current market price they are available at 46 PE?

Not having one time gain is not like EPS remains same… They we’re in net losses since last few years and now they have turned profitable

Company is growing and so should earnings.

1 Like

A GOOD INTERVIEW. ANYONE TRACKING THE CO?

1 Like

Posting here after a long time. From the outset I would like to state that Sequent is a big chunk of my portfolio. Unfortunately there were many pending issues over the last few years and the stock kept dropping from 100 levels even down to 45 if I’m not mistaken. I will not go much into the financials, we are all aware that the company is ebitda positive from last few quarters and sales are also growing as projected. Promoter is holding 57 plus % and going by the track record they would want to look for an exit in the next few years, possibly a PE fund (pls see the recent news about wochkard giving a mandate to sell its formulations biz to PE). Despite the carnage in the market the stock is holding 70 levels quite well - I am happy to sit it out and watch the QonQ performance of sequent and look for an exit in the next couple of years, while the promoter group firms up their strategy.

Please note - the stock is not cheap at 30 PE so please do your own due diligence. Worthwhile attending the AGM this year to meet the management (it a small event and easy to ask questions)

2 Likes

Sharing Q3FY19 Concall notes where the management told about the future plans and target for the company for the coming years. And also sharing Q1FY20 Concall notes which took place yesterday:

Q3FY19 Concall Notes

- European performance during this quarter was slightly below our own expectations and this is a lot to do with the supply chain challenges in the region.

- New Injectable is launched in EU which is the world’s fastest growing injectable

- also completed our first product validation of another injectable at Bremer facility. This incidentally is the largest injectable product in the world in the animal health space.

- Further our deepening relationships with the global top ten is paying off, while we make an entry in the highly valuable Japanese market with two successful registrations a short while back.

- Our US business continues to grow steadily with the commercialization of second API in that market

- About one-third of the business comes from the global top 10 players.

- I think over 80% of our business would be in pure regulated markets.

- A large part of our growth in API business is coming from better pricing almost I would say 60% of our incremental growth is from better price products and balance would be volume increase.

- we do not chase volumes in our API business and as we get into better price business we let go the lower price business,

- for the next two years we do not foresee any significant capex except in debottlenecking that maybe required in our API business.

- We must get 2.5 - 3 times on assets terms on the API business.

- I am clearly confident of maintaining at least 30% growth rate in the foreseeable future as far as our API business is concerned.

- Yes so I think we have been guiding that our formulation business will be growing at about 17% to 18% over the next two years followed by faster growth thereafter as we benefit from our own pipeline.

- While for the first two years the API will grow a little faster than that close to 25% year-onyear and thereafter it will probably by led by the formulations.

- Target of 2000 Cr revenue by FY23.

- The management is confident enough that they may achieve that target earlier than that.

- I think the first revenues from US formulation business will start from FY2021 because we make our first filing in FY20 and the first approval in FY it typically takes between 12 to 15 months for the approval.

- Around 2% of gross revenue is spend as R&D

- Around 50% of the revenues are coming from the top 10 global players

- Around 80% of the API business is coming from Regulated markets, which is helping them in getting better profit margins.

- 60% of the growth in API segment is through better prices and the rest is through increase in volume.

- Expectations for next quarter for API is around 30% Growth. And 20% growth overall.

Q1FY20 Concall Notes

- Formulations business grew 14.6% (YoY) driven by strong growth across all geographies (except EU), compared to industry growth of 4%

- Robust performance across geographies, except EU

- Strong recovery in Turkey; recovered with a growth of 82.2% (YoY) - currency weakness continues

- EU performance below expectations with a decline of 2.8% (YoY)

- Brexit challenge continues, impacting supply chain

- Unprecedented weather conditions in parts of EU

- We will get back to track in the second half of this year as we have planned some new launches over there.

- We have now established banking relations in EU and will be able to drive down interest cost leveraging european borrowings.

- 1 US filing during the quarter, total 18

- Expanded R&D team in India, adept to execute 10+ projects per annum

- 20+ new filings in US in next 3 years

- On-track for first US injectable filing in FY21

- There is a bit of seasonality effect on formulation business across various geographies and Q2 is tend to be slow in EU & Turkey due to the holiday season.

- However we expect business back in Q3 & Q4 because at that time the environment is good in generally all the geographies.

- We have started operations in France & Italy from where expenses have starting hitting in P&L.

- We expect italy to break even in the second half of the current year

- While France will at least take 12 more months to break even.

- We have also completed key hiring for the business managers in US for leadership position in this period.

- He is expected to join in another Qtrs time.

- We are confident enough to be delivering 400 Cr+ API business for the year

- We will be developing incremental capacity for API business which will help us facilitating the growth from the later half of FY21, this will be concurrent to our current business.

- We will be seeing a faster growth in formulation business which will start after we start commercializing in the US.

- We will file our first product in couple of months

- We are 1.5-2 yrs away from our first commercializing product in US.

- So you can see fast growth from around late FY 21 or early FY 22.

- Till then 13-15% growth will be there in formulation business.

- Capex will increase in the second half of FY 21

- These will not be the significant ones, these will be just balancing capex.

- We will be adding balancing equipments.

- There is an increase of 13-14 Cr in net borrowings which is a working capital loan as Turkey is a very capital intensive market & hence we needed it.

- Incremental capex for API business will be around 25-30 Cr spread over 2 yrs.

- We have two types of injectables, some injectables are which we produce on our own end in Germany & Turkey and some which we outsource from the other parties both in India & outside India.

- Our 40-50% of the business of formulations come from Injectables.

- 10-15% of the formulation business is outsourced from third parties.

- Like Spain, Benilex where we do not have our own manufacturing unit, we sell injectables which are from third parties.

- The third party distribution business is actually more profitable business than our own manufacturing.

- But there are certain risks associated with third party business & hence we want to have the right blend of it.

- Customer relation is owned by us in third party distribution which is the most significant part.

- Unlike human API the payment of ANDA filing is to be done at the time of approval & not at the time of filing which is very beneficial for us.

- Turkey has always been lower in Q2 due to seasonality effect and so will be this year.

- Turkey will get almost 120 Cr of business in 12 Month period.

7 Likes

Was anyone able to attend the AGM?

Hi,

I am just curious as to why you think the promoters would want to exit?

From Mar 20 shareholding, I see that the pledging has gone up to very high levels.

is it something concerning?

Carlyle Group is acquiring Sequent Scientific.

Open offer to existing investors at 86 per share.

2 Likes

Since current promotor has more pledging,i feel take over is good for the company So that it can focus in biz rather than servicing the debts/cash issues.

My question here is take over by PE firm Is good for minority shareholders or we need to use open offer and exit ?

Holding from much higher level hence seeking experts opinion to take decision,Thanks in advance

Finally after many years of waiting the true valuation of Sequent will be unravelled. I would not tender shares at 86, in fact it is understood that the seller is taking a minimum 30 percent discount as this is a distressed sale.Further release of pledges will certainly help this stock. Usually private equity players enter a company with a 5 year horizon and look to exit with a a minimum of 3X on their capital. Also, please look at Global animal healthcare companies like Zoetis and Elance especially their PE multiples and then look at sequent now that the technical overhang of the pledges are gone. I would gladly even buy the share at Rs 100 with a long term view only. My sense is in the coming days, it would trade well above 3 figures.

8 Likes