Thanks Vikas for the links. I think it will be interesting to look at the production data in their ARs and work out the cost structure. It’s no doubt a potential stock once the oil trend reverses which is likely to take a while.

Results are out.There is an increase of ~5Cr in amortization , otherwise net profit is at same level as Q2.Where can we find Production volume and net realization per Barrel data for this Q?

Does anyone know if the charge “amortization of hydrocarbon assets” relate to new wells or does it refer to both new wells as well as exisiting ones?

Amortization expenses are for older wells…Cost for new wells get added to Development of Hydrocarbon properties in Balance Sheet.Check last quarter Result in Bse.http://www.bseindia.com/xml-data/corpfiling/AttachHis/Selan_Exploration_Technology_Ltd_081114_Rst.pdf

Not sure why this data is not present this Quarter.

Does this mean that the cost of production for Selan is all P&L items excluding “development of hydrocarbon properties?”

Well According to my understanding Yes.If you check Annual reports, in P&L statement they declare the expenses for Development of Hydrocarbon properties cost however it gets transferred to “Development of Hydrocarbon properties” and not considered as part of expense.This expense is later amortized in P&L statement.I am not an expert and this is what i understood from reading the AR,so I may be wrong as well.

there are costs of finding and drilling a well which are capitalized. if after the drilling the well turns out to be a dry well, it expensed immediately, otherwise the cost is capitalised.

the costs are then amortized over the life of the production of the well to match the costs and revenue. this amortization is started as soon as the well is placed into production - so it includes all wells - old and new.

this amortization is not to be ignored just like you will not ignore raw material cost when calculating gross profits

4 Likes

Dear Rohit, thanks for the clarity. I had read a report which spoke about cash cost of exploring oil. This said that almost 99% of the oil companies dont lose cash even if oil stays slightly below $40 per barrel.

Would you know on where Selan stands on the cost curve of cost of extracting oil? My calculations say that the cash cost of extracting is about $17 but with the amortization and depreciation expense (non cash items) total cost including cost for new exploration crosses $40 per barrel. I wonder where Selan falls in the cost curve?

Abhishek.

Hi abhishek

first a disclosure: i used to hold selan, but sold it a few months back. So in the spirit of transparency i am not recommending a buy or sell or any specific opinion.

I think the concept of cash cost of extraction is incorrect. Analysts use it to justify the unjustifiable. To give an example, lets say a company spend 10 Mn usd to find and dig a well. That the F&D cost which is capitalized and then passed through P&L via depreciation.

Once you dig the well, the cash cost is the cost of pumping oil from the well - manpower, materials, overhead etc. This is bound to be very low and it is not the correct metric to analyse a company. To an analogy, the cash cost or incremental cost of wireless service once the network service is a few paise per min. Still one would not evaluate a telecom provider on this cash cost ? A company may make money on cash cost basis, but how will get required capital to fund new wells, considering that oil wells are a depleting resource.

In case of selan - i dont know their cost per barrel. There is very little shared by the company - they dont share their reserves, estimates or any other costs. Simply dividing the capitalized cost by volume produced will not give a good number because this number could under-estimating the incremental cost of production. Lets say the company drilled the good wells first where the cost of finding and exploration is less. Now the company is moving to more marginal fields. In that the backward look cost understimates the future cost. The reverse could also be true.

So frankly i have no idea and have not found any source for getting this number. I will happy to be pointed to some source of data where this is available or can calculated.

6 Likes

Recently I worked on Selan and thought to update it - Key issue is opaque nature of the management which does not much give any indication what is happening in terms of exploration activity. Posting the work here for VPs - hope its useful

Company Description: Selan Exploration Technology (Selan) is an independent E&P company engaged in onshore exploration and production of crude oil and natural gas. The company owns five oil and natural gas fields with proven reserves. Of these five fields, three – Bakrol, Indrora and Lohar – were awarded to Selan by the government in 1995 and Ognaj oilfield and Karjisan gasfield in 2004. The company is yet to start activities in the Karjisan and Ognaj fields.

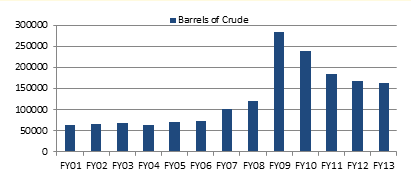

Proven history of production ramp-up: Company during its first phase of enhanced oil recovery (EOR) project (2002-2009) has ramp-up their production from 65000 barrels in FY02 to 282745 barrels in FY09. Post EOR, production started to decline further (see chart) and came down to 168000 barrels in FY13 (after FY13, volume data is not available). As per FY14 Annual report, Company drilled 10 new wells in FY14 and applying for approvals to drill more wells. However, since last 2 years production data is not available, one cannot understand whether there is any growth in production.

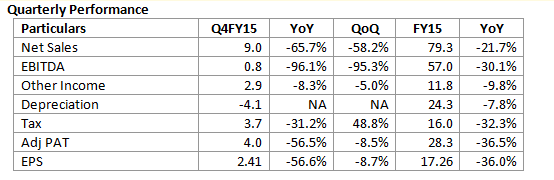

Weak results for FY15 and Q4 Result update: For Q4, Sales, Ebitda and PAT degrew -66%, -96% and -56% yoy to Rs 9cr Rs 0.8cr and Rs 4cr respectively. PAT degrowth was contained on account exploration cost extended for 5 year period leading to writeback of cost this qtr. For Full year, Sales, Ebitda and PAT degrew -22%, -30% and -36% yoy to Rs 79cr, rs 57cr and Rs 28cr respectively. EPS at Rs 17.26/sh for FY15.

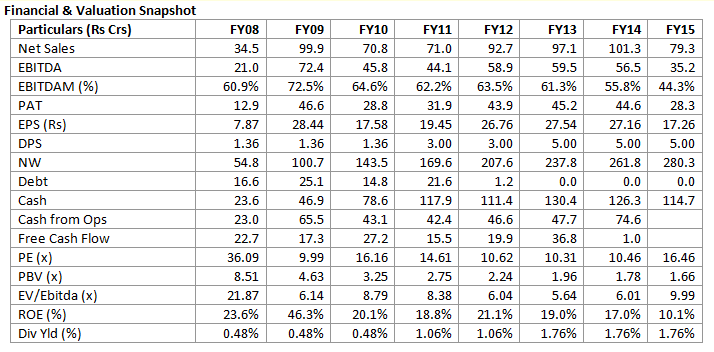

Balance sheet continues to remain strong and constant dividend payer: Company is debt free and uses internal accruals to fund its exploration and development activities. Current cash balance stood at Rs 115cr (Rs 70/sh) and Networth at Rs 280cr for FY15. Further, company pays regular dividend, and has been paying Rs 5/sh dividend for last 3 years.

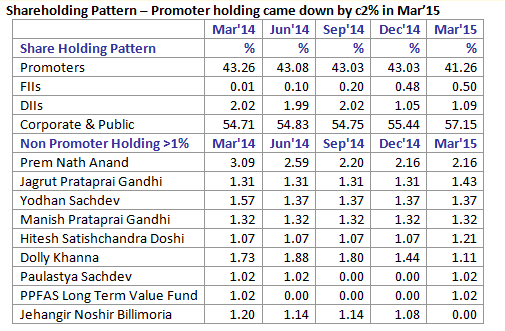

History of Buybacks but promoter turned seller recently: Company has history of buybacks. Most recently in FY13 they bought back 5.78 lakh shares at Rs 274/sh and 2 lakh shares they bought back in FY09 at Rs 140/sh. However, from BSE/NSE disclosure, Company’s promoter (Asha Mahajan – holding came down from 9.25 lakh shares in Dec’14 to 6.36 lakh shares as of Mar’15 and as per last disclosure holding came down to 5.8 lakh shares) is selling shares and on YTD basis (Jan-Jun’15) and sold over 3 lakh shares (1.9% of total outstanding) in open market.

Possible fund raising through equity or debt: In Dec’14, Post sharp correction in crude prices, Company released press release indicating that there will be possible fund raising if crude prices remain subdued for prolonged period to support their exploration/development programme. No timeline provided as such nor any board meeting to effect the same has happened. Company holds Rs 115cr cash which will support medium term capex plan for the company.

Outlook: Given opaque nature of management (no press release, presentation, concalls or meetings), one cannot provide much insight what is happening in the company. From FY09 to FY13 (data is available), production was more or less similar and revenue was moved with crude price movement. FY14 Revenue was highest due to high crude price while FY15 revenue got impacted on sharp crude price fall, but this does not provide any indication on crude production. While, Future production depends on drilling new wells (they drilled 10 new wells in FY14) subject to Govt approvals (also have received few approvals in FY14) which usually takes time and commercializing those wells for production (this parameter is unknown). Even oil reserve data is not provided so as to ascertain the value of those blocks. Promoter selling is a key redflag here.

5 Likes

If you look at DGH data, production from the Bakrol field has clearly increased, while Lohar and Indrora have decreased to an extent (around 33%).

Here is the average of the last 3 months for all three fields:

Bakrol

Feb-Mar-Apr '2014 Oil 1008’MT Gas 493000 (m3)

Feb-Mar-Apr '2015 Oil 1521’MT Gas 725599 (m3)

Lohar

Feb Mar Apr '2014 Oil 998('MT) Gas 16681 (m3)

Feb Mar Apr '2015 Oil 667 ('MT) Gas 12206 (m3)

Indrora

Feb Mar Apr '2014 Oil 110 ('MT) Gas 5195 (m3)

Feb Mar Apr '2015 Oil 69 ('MT) Gas 3629 (m3)

Overall Gas production has clearly increased, while oil production is stagnant. This is not too bad, because Gas prices have increased, and oil prices have declined.

The key is to unlock what is apparently a high potential of the Lohar field.

The average monthly turnover of Selan was around 6 crores last quarter, which I believe would be accounted for by crude sales at around 50 $ a barrel (approx 7 barrels to a MT), and gas price of 5.4 $ an MMBTU (approx 28 m3 to an MMBTU). So if crude prices increase, you can calculate the likely profit increase.

Regards

Samir

Thanks @samirbhai for production update…can you share the source of these data as i could not find it on DGH site (i am a registered user)…is it not publicly available?? would be helpful if you share the link

No, it is publicly available. Go to DGHINDIA.ORG, Login, Click on Bidding Rounds, Click on Discovered Field Bidding, You will get a list of all the Selan Blocks, along with other blocks. You can then click on any, to get year wise production data.

1 Like

Thanks @samirbhai…got it…missed it completely…thanks again

From page 23 of AR FY15,

“In the case of oil fields at Bakrol, Indrora and Lohar, the original contract period ends in 2020, while in the case of Karjisan and Ognaj, the contract ends in 2030 and 2033, respectively. Under the Production Sharing Contract (PSC), the Government has the power to extend the contract for a period not exceeding 5 years and management is of the opinion that there is a reasonable likelihood of this extension.In the circumstance, effective from the current year 2014-15, the amortisation of expenses has been extended by 5 years, especially keeping in view that the investments made in recent years for drilling of new wells are expected to continue to result in oil and gas production significantly beyond the original contract period. The Auditors have taken note of the above changes in their Audit Report and their opinion is not modified in respect of this matter.”

What happens if the contract is not renewed after 2020, considering that the current government is taking the auction route for usage of natural resources?

Also I don’t like that the company is is extending the amortization period by 5 years, which it probably did in order to increase the reported net profit in the near future. The previous approach of amortizing only till the end of contract term was more conservative.

Disclosure: Invested@Rs.215

Positive points:

- War might start between Saudi Arabia and Iran because of Sunni and Shia conflict.(it might lead to increase in price of oil.)

- A lot of US companies took loans during 2007 commodity boom and they might go bankrupt, later this year.

- Narendra Modi wants to reduce crude oil import. He has called it in a number of speeches. It will lead to easy policy regulation and easy to get contract.

- Oil exporting nations like Venezuela, Russia, etc. are already suffering a lot because of low oil prices. They might go broke in near future. Production cost are already higher than selling cost for a number of countries.

Negative points: - Oil exploration also includes luck. They might not find oil during well digging. They have also missed targets in the past.

- This might be the new normal for oil. As it happened with coal where it could never recover to its previous highs. Governments might be shifting towards renewable sources. With abundance supply because of technological innovation and low demand, the oil might never recover its peak.

These are the points I could think about. Looking for a healthy discussion. Selan has no debt so its placed better to handle this carnage. What are your views on these points or there is any other information that I missed to take into consideration ?

Hello Samir Ji,

Any Idea where is this data now… I think dghindia.org is no more presenting production data ?

Sorry for the delayed reply, Pankaj, but I don’t really follow Selan much anymore. Had a look again at the DGH india site, which has gone through a redesign, and like you, I could not find the data.

However, what I did notice was that in the recent discovered small fields auction round, Selan did not win any blocks or fields. I am really surprised, since this was their primary business model.

It still is a nice business, and if an accounting jock could find the terminal value of their cash flows over the next 10 years (simply extrapoloating the current cash flow less tax), and see whether it is more or less than current market cap, it might be an interesting exercise. Otherwise, someone needs to quiz the management on their plans after the current fields run dry or their contract period becomes over.

4 Likes

Thank you Samir Ji.

Agreed, I was also surprised onto Selan not wining any of the block. Giving a closer look on the blocks available I realized blocks available for auction are not near it’s existing area of operations. Also the terms of this bid have been different than earlier conditions.

But Thank you once again for your reply.