My guess is brokers get paid on commissions only when trades get done. For Satin that gets ttraded 10k

shares a day, probably not worth their time if their clients (institutions,

hni) can’t buy. So not worth spending time…Other thoughts are welcome!

I am unable to find the Annual Reports and Financial Results of the company. Can someone help me?

Here you go 2015 : http://www.satincreditcare.com/uploads/1459171921_attachment_annual_Book-final-05.pdf

previous ones are available @ http://www.satincreditcare.com/annual-reports.php

Thanks a lot Steven. Any idea where I will get the quarterly results.

Strong growth traction to continue in fy17

Disc: invested

1 Like

This looks like the the sector to be in, it’s available at reasonable valuations due to some unreasonable extent of fear. And opportunity size makes it even more lucrative.

":

:

The Delhi-based microlender raised the money through issue of 32,30,000 equity shares at Rs 130 each and 28,70,000 share warrants at the same amount to the joint fund run by SBI Holdings of Japan and Netherlands Development Finance Company (FMO). "

As one can see, SBI FMO still holds around 32 lac shares and is yet to convert the 28.7 lac warrants -

http://www.bseindia.com/corporates/shpPublicShareholder.aspx?scripcd=539404&qtrid=89.00&QtrName=March%202016

So add 28.7*304/100=87.2 cr into Mcap. So the effective Market cap is 977+87=1064cr.

Also, add 28.7*130/100=37.3 to the net-worth of ~280cr at Dec-15.

Disc: invested

Cheers

2 Likes

the read trhough from SKS call was very positive for Satin. 2 points I would want to flag:

- Mentioned incremental growth driven by under penetrated north - Satins forte.

- Further the key value in the franchise - owning last mile access to rural borrower which is very hard to replace - was highlighted.

I was trying to enter Satin from past 2 days around 305 levels but it didnt came and now ultimate the stock shot up to 330

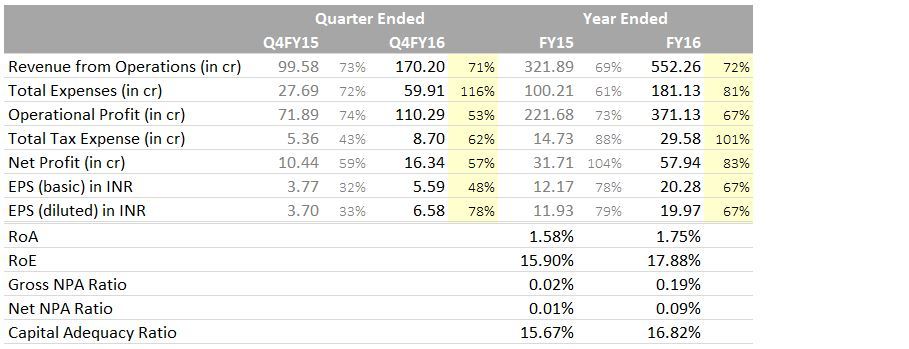

Satin Q4 and FY16 numbers are out. Outstanding growth again. MFI sector looks quite interesting.

Disc: Invested

4 Likes

Thanks for the update. Besides the growth, improving returns are to be noted too…

At Q4 FY16 EPS run rate of 6.6 Rs, FY17 EPS is 26.4 even without assuming any growth. P/E (FY17) of 13x for this growth (>50%) and return (ROE ~20% in FY17) business is unfathomable!

Another way to see the margin of safety in Satin is to look at Satin vs SKS. Both have Rs 6.6 EPS in Q4FY16. Satin clearly has better AUM growth prospects (low base, right geographies, lower ticket size) as demonstrated in recent qtrs. Given the lower profitability owing to lower scale, growth will create scale on funding, opex and improve profitability driving EPS growth even faster. Unlike SKS, it has no Tax benefit inflating earnings, either. Yet at same EPS it is trading at almost half the price/multiple!

3 Likes

Does anyone has some comparison data between Satin and other listed MFI players (SKS, Ujjivan, Equitas) ? Above posts have some comparison with SKS but will be interesting to see it with other players as well. If someone has already done the comparison then please share… it will save me time to draw up the matrix.

Disc : Small exposure to Satin.

Is it just me or are the comparisons on EPS mistaken? As far as my limited understanding goes, finance companies are evaluated on book value and ROE and not EPS.

I didnt get that memo Tushar! Last I checked, valuation was no science. EPS comparisions are no mistake. Many ways to skin the cat. High growth, stable credit cost and earnings growth (all checks) - I use PE andong with PB Note Satin and SKS have similar Q4FY16 EPS and BVPS, so valuation difference exists in both). Different view on these pls use PB Market cap/deposits or whatever else shakes your tree :)To each his own.

MFI_Compare.xlsx (2.5 MB)

sushilkc, I tried to make this work sheet comparing various MFIs like sks, ujjivan, equitas, satin, arman, this is still work in progress. This is not a straight P/B comparison, we need to look at the growth rates, geo presence, sfb license, product mix, aum size, penetration in rural/semi/urban areas, history, gnpa etc. SKS is the leader by a far margin, there is not much to chose between others.

7 Likes

Investor Presentation by Satin:

http://www.bseindia.com/xml-data/corpfiling/AttachHis/A0128945_A7FD_4D32_A667_7E81462BE7BC_184453.pdf

Aggressive guidance for fy17.

1 Like

Hi Sanjay, The guidance is strong in my view but I would not term it aggressive because

- Historic mgmt performance vs guidance

- Satin’s pefromance so far and teh business momentum

- Trends in the MFI industry

- Further tailwinds to Satin vs peers given low penentration in their target markets + no bank license business model change saddle

- Recent monsoon and upcoming elections releasing money (seen in recent elections in other states) in rural economy further greasing growth, keeping credit quality at bay

1 Like

Though elections can be a risk as well. I attended latest conf. call of Arman fin. where the promoters said they are opening new branches in UP & Maharashtra but will be more careful in lending in UP due to elections next year.

Disc: invested both in Satin and Arman.

That’s interesting Vicky. But every state will have an election every 5 years. No matter which state an MFI is in evrry 5 years their business will be exposed to this risk. If this is Arman mgmt view on elections risk, are they not in the wrong business? should they not return money to shareholders and go home - Why risk 100% capital every few years for 20% ROE?