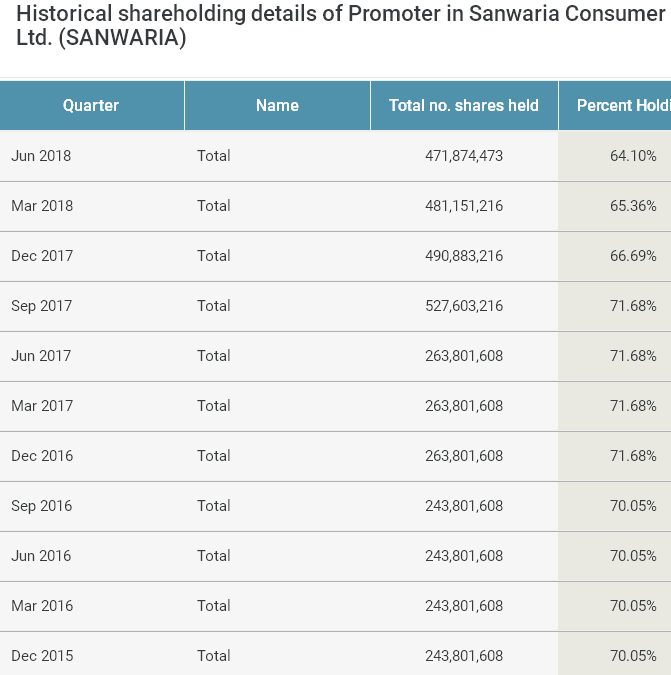

It’s a known story they are fraud, there were changes in Recent shareholding pattern (March-2018) about 1.3% shares they transferred to non promoter, not sure what is the purpose of the transaction and also there is no filing or details submitted to stock exchanges as part of Listing obligations. I feel the price movement it is purely operator driven. The only real beneficiaries are Promoters and Operators.

According to Audited result which came overnight , Profit is 21 cr instead of 35 cr. A big difference.

Also, due to higher equity, annualised EPS is lower for Mar 18 than in March 17.

The difference is true and the difference is almost 14cr and also there is no auditors report included. They have submitted audited results to the exchange on Exchange Received Time 31/05/2018 03:50:57 which is delayed and also early morning around 3:50 AM not sure who was working till then.

Think about the EPS after equity dilution promoters equity infusion 100cr @ 35 Rs and 400 cr QIP. Not sure which PE firm is going to subscribe for this QIP with lot of discrepancies and corporate governance and No transparency.

Co’s have submitted un-audited with 100cr PAT during market hours and Now Audited results with 86 Cr PAT they have submitted with one day delay and 3:50 AM (May 31) in the morning. Again the sole beneficiaries are Only the promoters.

Now seeing the market conditions Auditors have become cautious about the reporting numbers with co’s like in the case of Atlanta, Vakrangee, Manpasand.

If it is the same with sanwaria, many investor may not get complete exit during downfall.

Someone asked why promoters are selling at current depressed rate but buying via preference shares at 30

They said non core promoters are selling

The call didn’t allow all participants to ask questions but my question was why are core promoters not buying from non core promoters if non core promoters are selling

Historically if you see few years back price went quite high on good sale and then came down

Promoters are definitely cashing out at higher price

This might fall heavily on continued promoter selling

One of the most dishonest promoters I have come across on a call and the way they were making up figures on the fly

Well if the market cannot absorb even 2.5% of this super-hot stock over 6 months then this is indeed garbage!

When the biggest decline of 5% in Promoter holdings happened in a single quarter, share price went from 6 to 23, between sept and dec 2017, whereas march and june 2017 were already spectacular results!

Remote Excuses to beat about to justify some observation!

I would personally avoid any company that micro-manages the stock price, to make it look “at right level”. I sure hope the management has better things to focus on!

Promoter buying (preference) shares directly from Company at 2x market price gives the money to the company, and not to their own family. This only gives me bit more confidence in this garbage!

Look at what happened to DBL

Can you talk about the auditors’ position? There are a lot of rumours regarding quitting, Can you clarify?

These rumours that have been going on, I do not really know how they started but they are completely unfounded, completely baseless, completely false. Something like this is absolutely shocking to us but I guess in today’s day and time with markets being jittery, anything and everything takes off without any base to it.

They sent the concall transcript to the Exchange. They always do a concall every Quarter now and publish it.

Basic points:

Preferential shares @ Rs 35 of 100 Cr, issue is pending approval of Exchange/SEBI but money has been given by promoters to the company!!

they say that they have bought shares like this at premium to market in the past also.

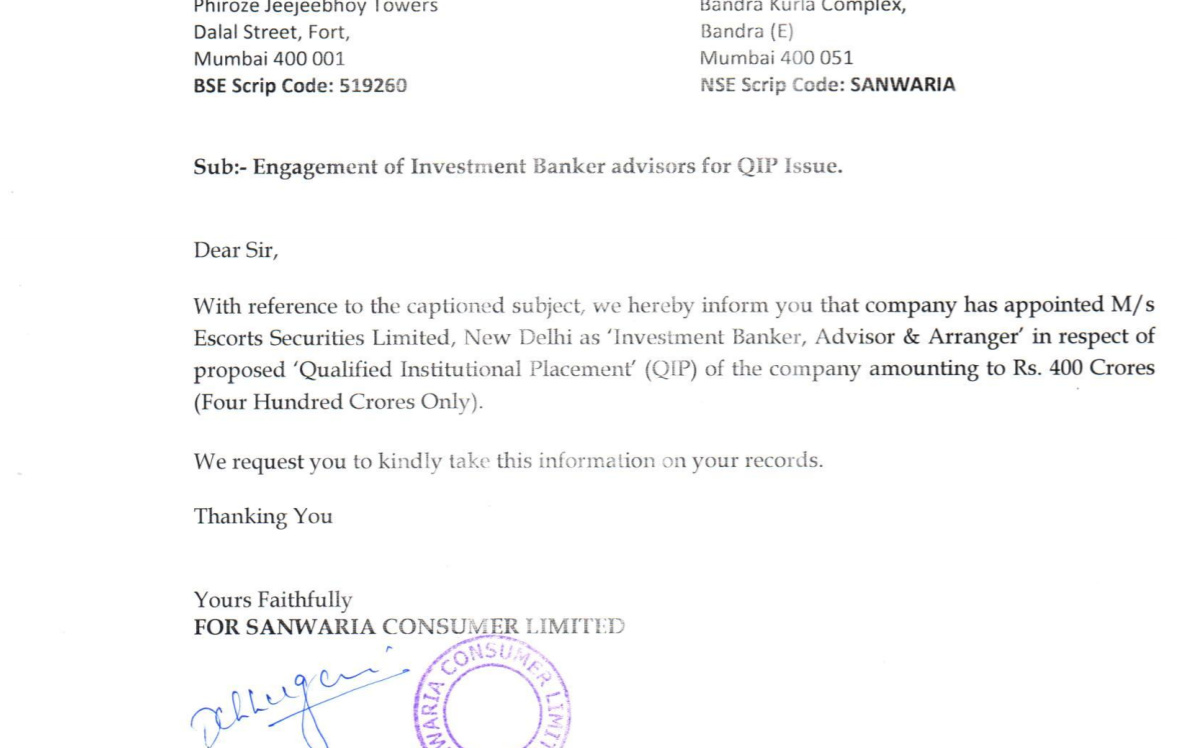

They are trying for QIP of 400 Cr. Several analyst meetings being done already.

Patanjali sourcing only Soya products, now for 2 months only. Rice, oil etc in works. Insignificant contribution to Revenues currently!!

Online shop portal here: https://www.sanwariaconsumer.com/shop/

I could not buy anything, it only allows to add to wishlist! Maybe registration is required?

Open 500 stores in 3 years all over India, 100 within one year in MP/MH.

Guidance is 25% topline growth, they are apologetic about drop in share prices, saying they never advised people to buy above Rs 20.

They have replied in concall to questions about the controversial topics:

- Inventory/Trading: [on pages 6 and 10]

they say their 80% (branded sales) revenues come from oil and rice, in-house products also wheat (no soya!?), hence their working capital has grown immensely, as rice is kept by them for ~2 years. Rest items they do trading in.

- poorly paid employees: [on pages 11 and 15]

They have 250 people working, mainly contracted, hence they put this expense in manufacturing/other expenses. MD was not sure!

Receivables and poor margins could well be because their trading activity might be mostly unbranded commodity play.

I tried to buy some rice and soy chunks, they were charging me Rs 225 per 5 kg for shipping. Prices were good, but with the shipping costs, total loss! They also have an app now for shopping!!

Aside: Ethics was added to the HBS course after the crash of 2008. Too late, IMHO, to teach old dogs new tricks!

Sanwaria has been Registered with U.S Food And Drug Administration bearing U.S.FDA Registration No. 16431247460.51055010-2a46-40c3-86f1-5a3c3bc69aff.pdf (1.9 MB)

Sanwaria opening its own store and that does not feel like step in the right direction. Now in India many of the people buy things online. Even the chain store have very limited set of its own product. they generate revenue by selling products from other brands. I feel it is better for Sanwaria to concentrate on online and chain store to sell its product. Instead they can make their distribute network more stronger . It has to first grow its sales in India itself before spreading wings into other counties(U.S.).

They have uploaded Research Report from Brickwork. Excerpt from there-

“Management is planning to collaborate with

leading online retailers like Amazon and Flipkart in near future”.

I don’t know how much more time they need for this. This has been written in their AR.