Yes, wtg suppliers will pressurize margins of crane suppliers. We need to

ask few questions - 1). What is the contribution of crane costs to overall

project costs? If this is low, squeezing them will not impact their

profitability much 2). Is there sufficient supply of cranes in market for

the huge projects that will come up under SECI bid? If not, crane suppliers

will have higher bargaining power

Happy to understand different views to understand this better

The cost to erect one MW plant is around 5 cr. If someone is setting up a 250 MW plant, the total cost is 1250 cr. The total crane hire charges could be around 5-15 cr i.e. 0.5%-1.5% of the total cost.

I am sharing the Ambit report, just to show that IPPS are still making good Incremental rate of Return despite low auction prices in SECI auctions…this should lay to rest doubts regarding IPPs going into losses or the margins of WTG makers getting squeezed to nothing.Ambit_Utilities (POSITIVE)_India Wind Power - Staging a comeback!_15Mar2018.pdf (170.4 KB)

Not only are the IPPs making good IRR / ROE, they are expecting to be rewarded by the market when they come out with their IPOs in FY19.

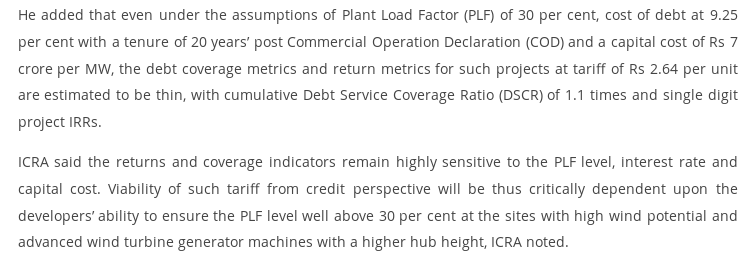

The calculation here is flawed as it takes PLF @30% while wtg now have 40% plf in TN and Gujrat. Further PPA is for 25 years and not 20 years as assumed by ICRA.

Finally ICRA assumes 7 crore per mw price, if that assumption is correct then WTG makers will have windfall gains and we need not worry at all. We are not investing in IPPs but in WTG and sanghvi only

Thank you for sharing your views and reports. Few observations :

In a financial model for calculating IRR, any revenue post 20 years hardly impacts the IRR. Even after 15 years, the impact is not much (not more than 1-2%)

Project cost works out to 6.5-7 cr/ MW. Confirmed from industry sources.

4000 MW has been auctioned by SECI so far. Sites are in Gujarat and TN with estimated PLF of around 35%

I have closely seen the solar asset creation play by IPPs and it is not going to be very different for wind. It is all about deploying large amounts of capital, create a large capacity and sell it to pension funds directly or through listing for long term , steady and predictable revenues/ returns.

So, IRRs tend to be low. I am definitely not discussing investing in IPP. But the way it worked in solar, was it led to very very low margins for EPC players. I do not expect it to be different in wind. So, I will not invest in a WTG supplier.

Height is > 110 mtrs. I am keen to understand who are competitors of Sanghvi that may have cranes > 110 mtrs and their size, presence, etc. Given the specific requirement of 110 mtrs + cranes and 4 GW + of capacity to be built in next 24 months, Sanghvi may even be able to charges higher margins (instead of pressure on margins )

Height is > 110 mtrs. I am keen to understand who are competitors of Sanghvi that may have cranes > 110 mtrs and their size, presence, etc. Given the specific requirement of 110 mtrs + cranes and 4 GW + of capacity to be built in next 24 months, Sanghvi may even be able to charges higher margins (instead of pressure on margins )

Yes i am even upbeat on above statement as most of the latest capex was in this category.

Sanghvi has 90% of the cranes in the category of more than 100 tonnes. And Sanghvi has 70% market share in this category. So even if there are any competitors, they cant make much of impact i believe.

I would request you to reconfirm the above figure with your industry sources. If this figure is approximately correct, then we can expect a steep rerating of WTG makers - Inox wind and Suzlon. Its an outright good news for investors in Suzlon and Inox wind…everybody is now fearing that the per mega watt cost of WTg may have come down to around 5 crores…but 6.5-7 crores per mw is a fabulous figure

Checked with 2 sources - Vestas and an IPP. Cost is around 13-14 cr for

a 2 MW machine

Wind project cost has 2 components - 1) machine or wind turbine which

costs around 5 - 5.5 cr (2). Land, permissions, evacuation, transmission

which costs 1-2 cr/MW depending on project size, location, etc.

Not sure, but it is possible that some wind mill suppliers may have sold

some projects at lower cost bcos orders were abysmally low last year and

there would have been some unsold inventory, and given that there is high

debt on books of inox. This is a guess and for sure it cannot be 5 cr all

inclusive. But this pricing is not a norm and wud not continue since 5.5 GW

has been auctioned.

Some IPP also acquire their own land bank and undertake Epc, development

on their own. In such a case they can buy machines at 5 cr/MW and WTG

supplier looses on development revenues

Not sure, but some wind mill suppliers would be selling at 5 cr /MW and

taking separate orders for Epc and development in their subsidiary or

associate firms and this revenue may or may not be part of consolidated

revenues for listed company. For investing in suzlon or inox, u need to

check this part.

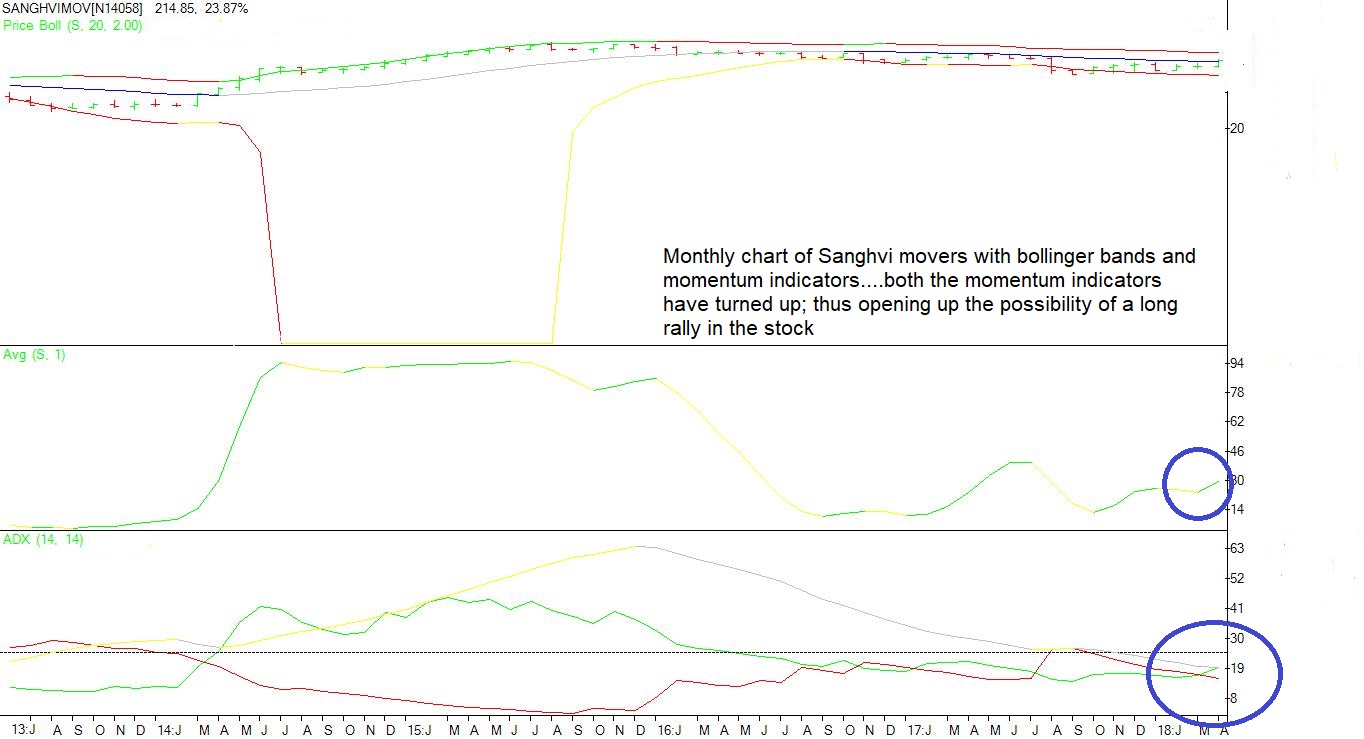

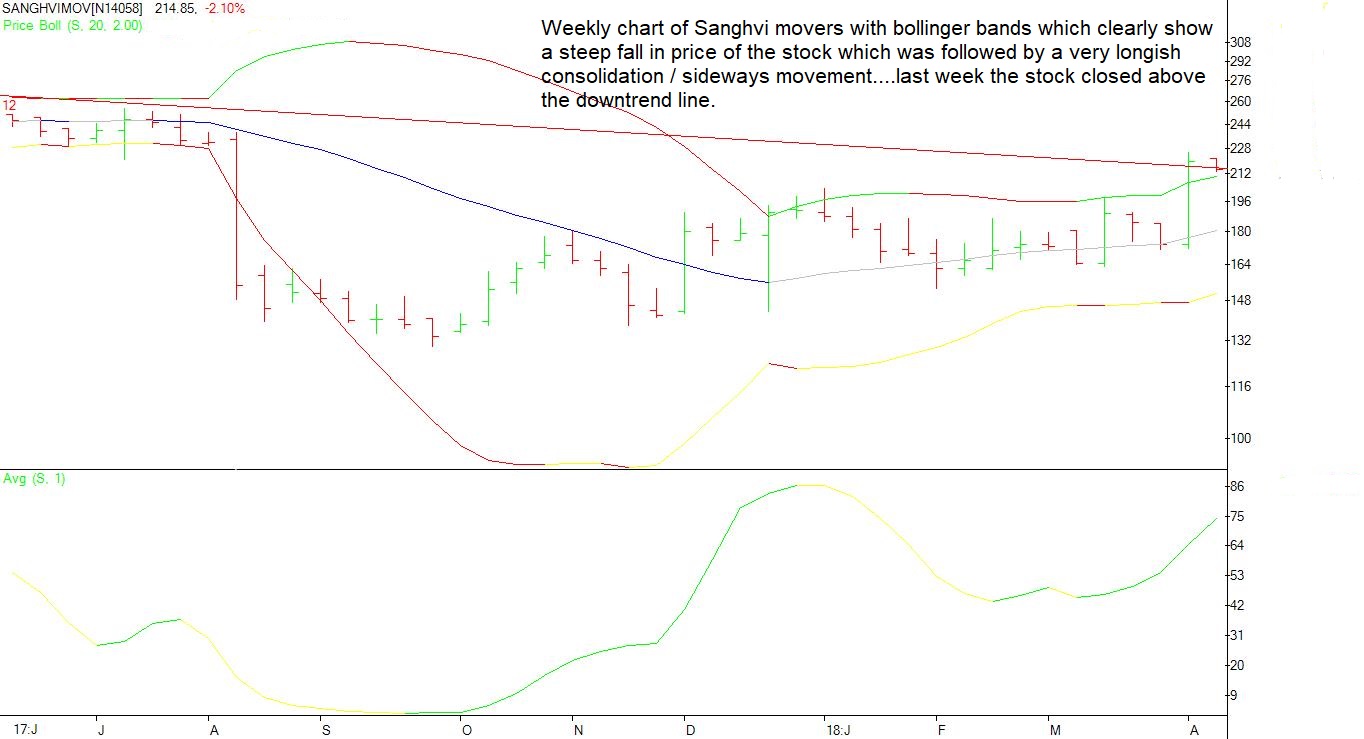

Hi, by looking at the Sanghvi Movers chart (few days old chart), it seems Inverted Head & Shoulder pattern completed and break out is already happened around 1 week of April 2018. From here I expect the stock to be in bullish trend.

Disclosure: I have invested in this stock.