The seci tranche V results are out. Under subscribed by 800 MW due to connectivity issues. this is good as developers are behaving rationally in bidding after confirming the availability of connections. There will be less delays in completion of projects.

To watch out for is hybrid 2.5GW tender scheduled, results to be out in August second week. that should be oversubscribed considering incentives involved.

Sanghvi_Movers_AR_2017-18_R.pdf (1.2 MB)

The annual report for the year 17-18 and now is open to discussion.

Hi All,

Company has announced Q1FY19 results. Also, they have published an investor presentation.

Click here to see the results and click here for the presentation.

Regards,

Yogansh Jeswani

Disclosure: Invested

Can anyone please share FY18 AGM Notes?

C P Sanghvi present at the AGM

Want to reduce debt by 50% in 2 years.

Last seci wing auction got muted response and got cancelled.

Issues on the ground… evacuation facilities lacking.

Guidance reducing amongst wind turbine oems.

Sml reducing their guidance. 150cr order book at the beginning of the fy. Currently 105cr.

May see 3000 to 3200 mw. Cu below 65% and yield could be 2% for fy19. Do not see yields below 1.5%

Gujarat seeing movement. Mah no work.

Contribution from other industries going up… railways, civil structures, irrigation projs, metro projs, working with LnT. 12 verticles working on.

Reliance not putting cranes in the market.

Crane life 100tn and less is 15 yrs and over 100tn is 20 tn from accounting perspective.

Planning 110cr debt repayment in current yr.

Planning disposing some immovable prop and cranes to pay off debt further.

Did lot of cost rationalisation. Reduced some personnel.

Rishi looking at fleet mgmt, maintenance, some clients, purchase of spares. Basically looking at purchase.

20 - 25% fixed cost of rev.

3% yield is passe. Best case now can be 2.6-2.7%

65 to 70% cu needed to cover all costs.

Interest cost up by 10 to 20 bps but overall lower coz of debt repayment.

Guys

The turn-around story in wind sector gathered pace 6 months back and has lost steam in with the Q1 results of Sanghvi/Suzlon/Inox Wind coming out

This post on my blog might help us take the discussion further

Comments and suggestions for further research welcome

I was invested in this from 2013 till 2016. Not tracking this right now, had noticed certain things about the management which I think people will need to consider before investing -

The management is prone is exuberance at the top of the cycle. You can see this in 2008 and 2014 as well, they tend to take on too much debt, build excess capacity and once demand cools off you will see losses for 4-5 Q’s. Cyclical nature of the business is anyway known but what is surprising is that management has not learnt from their mistakes in the past.

On one of the conf calls in 2014 a lot of questions were on this - 700 Cr of capex is being done, bulk of it being funded through debt, how confident is the management that capacity utilization will be hygienic? The answer was that market info is confidential and that it cannot be revealed. Any management that repeats the same error twice is a problem, it becomes a pattern that will get repeated again and again.

My sense is that in stocks like these timing becomes very important, especially the exit part. This is not a story one can look at with a long term horizon since the terminal value accorded to this during a down cycle will barely take into account earnings and will be based mostly on replacement cost. Do keep this in mind and buffer accordingly

Just posting a new item that is relevant to the topic under discussion

Gujarat has framed a land utilization policy for win-solar projects.

Hello @sjain_13,

Do you know if WTG suppliers will go back to their previous profitable numbers in FY20?

Do you mind checking with industry experts please?

Understand that FY19 was not really a turnaround year which the wind industry was expecting, due to additional problems like lack of inter-state transmission.

Wondering if this would be a problem for FY20 too.

If that problem is fixed or if we have signs of it being fixed, Sanghvi Movers can be a good cyclical turnaround opportunity.

I see they have already started clearing their debt in FY18 and there is a fall in interest costs in FY19’s quarterly results. I expect them to clear their debts further in FY19 using their CFO to reduce their interest costs further in FY20. This should enforce the turnaround further.

Thanks in advance.

Disclosure: Interested. No positions. Not a SEBI registered advisor. Not a buy / sell recommendation.

Excerpt from the Q4FY19 press release by Inox Wind

Common transmission network (central grid) in Bhuj, Gujarat is ready

This is the 765 kV evacuation network part of the Green Energy Corridor.

This will mean at least 4000 MW of projects at Bhuj will now have a smooth commissioning over the next 12-15 months

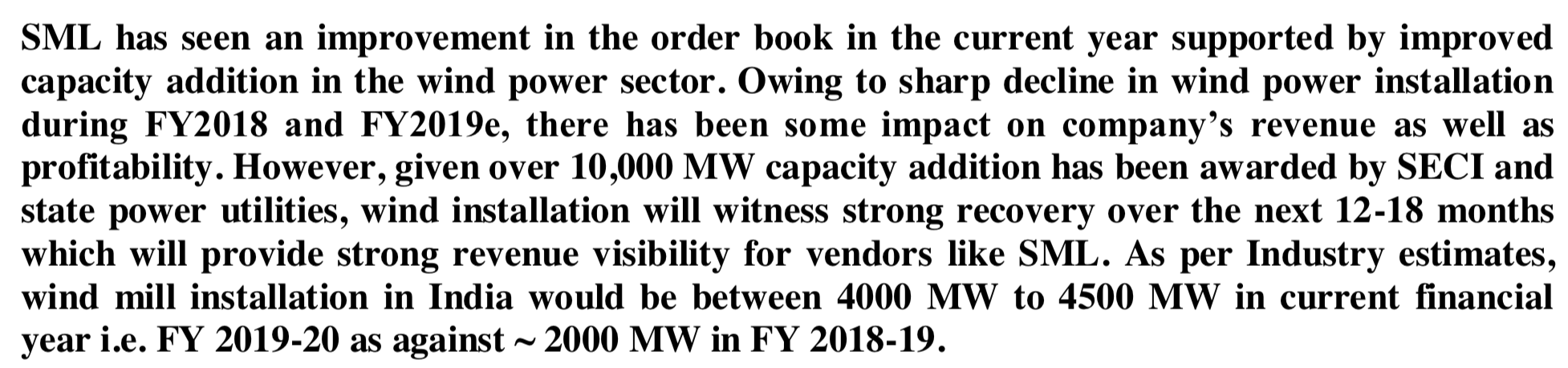

In Fy2016, wind energy installation was 3.5GW and Sanghvi’s turnover jumped from Rs.308crs to Rs.530crs. Even in Inox wind concall they said around 3-5 GW can be installed during the year Fy2020. If this happen we can see huge jump in turnover of Sanghvi movers.

Even yesterday, Allcargo’s project division show good jump in Turnover and profitability and one of the reason was revival in Wind energy.

All green shoots are there Lets hope the best.

Prashant

Results and presentation are out.

Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/5f8d50eb-966a-4873-9d19-18e0daa11411.pdf

Presentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/fa4853c2-0608-4cb6-a5a0-62990fa8ed0a.pdf

Points to note:

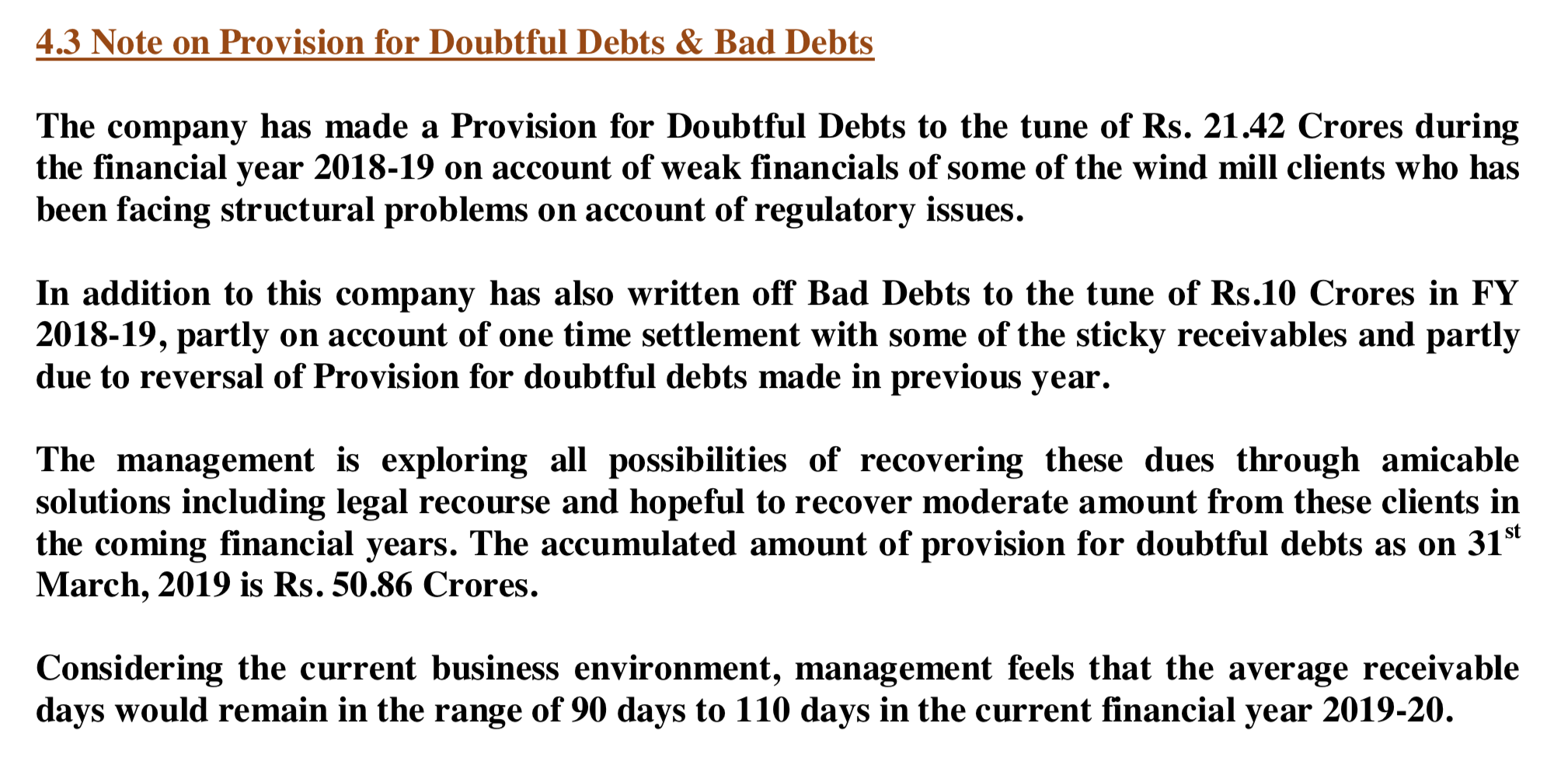

- Provisions of 28 crores! Pasting screenshot from the presentation. Any idea which client is defaulting here?

- Wind industry is going to recover in FY20 as per management and management expects top-line growth of 25% and most of it would come from H2FY20

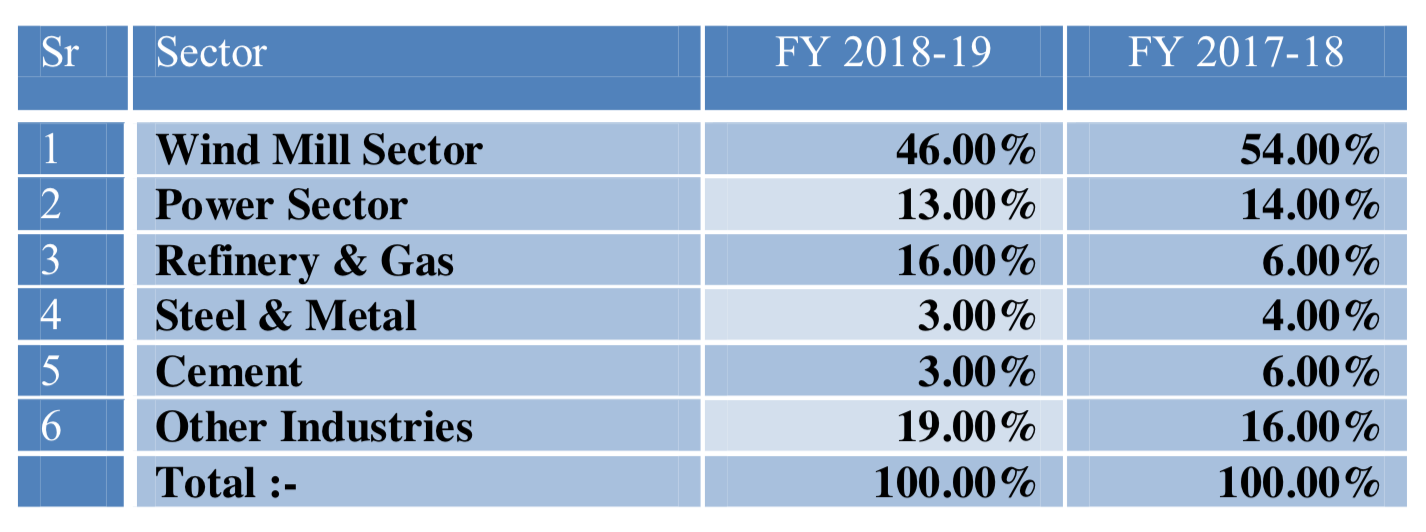

- Refinery & Gas share rose from 6% to 16% in one year. Almost 3x in one year. Any idea which part of gas value chain is driving this? GoI is promoting gas’ share in India’s energy basket and wants to increase its share to 15% by 2030 from current 6%. Policies for CGD, E&P, LNG have been rolled out and good growth is already visible in this sector. We need to understand if this will help Sanghvi. If this can contribute to topline significantly, we’ll have double advantage of wind sector + refinery & gas sector

- Even though the company is reporting losses, it is cash positive and hence reducing its debt. Should provide further boost to EPS next year as finance costs would decrease

Disclosure: Recent entry in March with 3% exposure. May add more if conviction increases.

Having played this story in the past…

Best time to enter is when company is making accounting losses but starting to pare down debt and shrink balance sheet.

The time to exit is when PAT shows a huge spike after 2-3 years of losses and management comes out and announces that the yield on their assets is > 3% per month and hence they are doing a debt funded huge capex to capture market opportunity.

Investors here will do well to study the company performance and share price from 2012 to 2015, history often repeats in such counters

Please do your own due diligence. I no longer invest in such stories for my own reasons - nothing to do with Sanghvi Mover as such

Main issue will be the ability of the customers to pay. It remains to be seen how much suzlon, inox etc will earn from the seci projects. Till their cash flow improves, a meaningful improvement should not be expected from sanghvi.

One of the main parameters to track for the Sanghi Movers stock is to track what is the capacity addition in wind energy is every month

The data for the month of May-19 is out

http://www.cea.nic.in/reports/monthly/installedcapacity/2019/installed_capacity-06.pdf

Wind energy capacity added in

Apr-19 = 190 MW

May-19 = 273 MW

Addition in 2 months YTD = 463 MW

@amey153, thank you very much for sharing this resource!

I got inspired by it and created this table. In previous years, the govt shared only quarterly data for wind power capacity. This exercise has helped improve my conviction.

| Capacity | Cumulative (MW) | Quarterly (MW) | Cumulative (MW) | Quarterly (MW) | Cumulative (MW) | Quarterly (MW) | Cumulative (MW) | Quarterly (MW) | Cumulative (MW) | Quarterly (MW) | Cumulative (MW) | Quarterly (MW) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Q1FY19 (not including June) | 36089 | 464 | Q1FY18 | 34293 | 247 | Q1FY17 | 32508 | 229 | Q1FY16 | 27151 | 284 | Q1FY15 | 23762 | 318 | Q1FY14 | ||||||||

| Q2FY19 | Q2FY18 | 34615 | 322 | Q2FY17 | 32700 | 192 | Q2FY16 | 28082 | 931 | Q2FY15 | 24376 | 614 | Q2FY14 | ||||||||||

| Q3FY19 | Q3FY18 | 35138 | 523 | Q3FY17 | 32848 | 148 | Q3FY16 | 28700 | 618 | Q3FY15 | 25088 | 712 | Q3FY14 | ||||||||||

| Q4FY19 | Q4FY18 | 35625 | 487 | Q4FY17 | 34046 | 1198 | Q4FY16 | 32279 | 3579 | Q4FY15 | 26867 | 1779 | Q4FY14 | 23444 |

One very interesting insight is this is going to be the best Q1 the wind industry has ever had, in terms of MW numbers, over the past few years (including the time before we had the auctions)

Previous best Q1 was in FY15 with 318 MW addition. In FY20, we already have 464 MW addition without adding June’s installation.

Discl: Invested

q4fy18 was the worst ever… is it possible that some capacity got spilled over to this quarter and hence seems high?

The way to look at this is a little different.

The installation does not follow a smooth curve.

Shifting from feed-in (cost-plus) tariff to competitive bidding was a big disturbance (change).

Non-availability of transmission infrastructure is a big show-stopper.

Like I gave mentioned in previous posts, the transmission infra (substation by Powergrid) at Bhuj (Gujarat) is ready.

This has paved the way for installation of 4000 MW of wind projects at one single location over the next 15-18 months.

The fact that installation has picked up in the last 2 months is a validation of the above hypothesis.

Very good source of information. However, as Sanghvi work is in installation of stage of capacity, numbers from this source would have already been reflected in previous quarter numbers of Sanghvi.