CONFERENCE CALL - from Capital Markets

Salzer Electronics

Sales can grow 25% in FY 2017 with 50 basis points improvement in OPM

Salzer Electronics held its conference call on 12th Feb 2016 to discuss its results for the quarter ended December 2015.

Rajesh Doraiswamy, Jt. Managing Director of the company addressed the call:

Highlights of the call:

During December 2015 quarter sales grew 30% to Rs 90.20 crore.

PAT grew 57% to Rs 3.4 crore.

Exports accounted for 29% of sales.

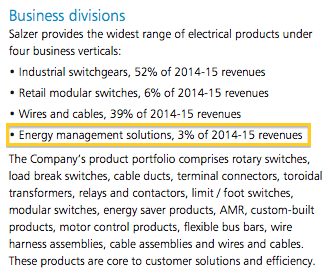

Industrial switchgear business accounted for 48% of sales and it grew 10%. This is in line with the company’s strategy of focusing on profitable and high growth products.

Building products business accounted for 5% of sales during the quarter and it fell 25%.

Copper business accounted for 36% of sales during the quarter and it grew 41%.

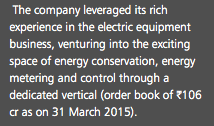

Energy management business accounted for 11% of sales during the quarter and it grew 789%.

EBITDA grew 24% to Rs 10.1 crore.

EBITDA margins stood at 11.2% down 53 basis points largely on account of product mix, higher contribution from copper business and one time consultation charges and Rs 60 lakh test fees charged during the quarter for new product developed for transformers General Electric. Testing happens for any new product that is developed in third party lab.

For the nine months sales grew 27% to Rs 262.30 crore.

PAT grew 52% to Rs 13.10 crore.

Exports accounted for 26% of sales.

Net worth stood at Rs 195 crore against Rs 107 crore as on March 2015.

Total debt stood at Rs 105 crore against Rs 937 crore as on March 2015 mainly due to increase in short term borrowings.

For the nine months Energy management business accounted for 12% of sales and it grew 368%.

During the nine months the company had technical alliance with Trafomodern. Trafomodern, an Austrian company-one of leading manufacturers of transformers in Europe.

The company will start production in first or second quarter FY 2017 from this tie up.

Salzer will use Trafomodern’s technology and design to manufacture Dry Type, Air Cooled Transformers, Chokes and Inductors in India.

The company also did successful capital raising through QIP whish saw well diversified representation and demand. 55% was allocated to FIIs and 45% to domestic mutual funds. Proceeds will be used for new product development and growth plans of the company.

The company has 5 manufacturing units located in Tamil Nadu & Himachal Pradesh.

It has more than 15 products catering to Industrial / Building / Automobile segments.

The company owns distribution network in local and global markets and it exports to 50 countries.

The company is amongst few players in India, to offer total & customized electrical solutions.

In-house manufacturing facilities with process capabilities ensures better product development and customization,

The company is the largest manufacturer and market leader in CAM operated rotary switches

The company enjoys strong customer relationships across the world.

It is the preferred supplier to GE, Schneider and only approved supplier of Nuclear Power Corporation

The company is the largest supplier of rotary and load break switches to Indian Railways.

The company has wide distribution network for international and domestic markets.

L&T gives it access to over 350 dealers in India. This apart it has its own network for modular switches with 50 stockist in 4 southern & western states

The company also has direct network across 50 countries with 40 international distributors.

Net WC improved from 145 days to 133 days/ the management is looking to reduce this further to 110 days by end of FY 2016.

Increase in exports and new products and customization will be future growth strategy.

It plans margin improvement through increase sales of high margin products and increase in exports especially to the fast growing markets of US, Africa and Middle East.

Energy management business has huge growth potential.

The panel business that the company does has lower margins. Revenue from panel business jumped from Rs 1 crore per quarter to Rs 2 crore in Decmeber 2015 quarter.

During the quarter, Asia (excl India) accounted for 21% of sales. Europe, 3%, US, 3%, India, 71% and others, accounted for 2%.

For the nine months, India accounted for 75% of sales.

There was no major fluctuation in copper prices.

Venture into new project/ product development will also be its future growth strategy.

DC Load Break Switches presents a high potential as there are very few manufacturers in the world. The company’s switches are the best available in market. The company already exports good volume to Europe & US.

Debtors days stand at 94 days.

In Switch gear business the company expects to grow 25% for the full year 2016. Till nine months it has grown 30%.

The company will start in FY 2017 the capacitor project by investing Rs 12 crore. In FY 2017 itself it will generate sales of Rs 4 crore.

Capex for FY 2016 will be around 19 crore.

Long Term Borrowings stood at Rs 17 crore against Rs 18 in FY 2015.

Total sales from L&T distributors grew from 110 crore in FY 2015 to Rs 87 crore in nine months. L&T contribution has dropped from 40% to 33%. L&T business is growing but as a % to total sales it is falling.

GE and Schneider revenues grew from 2.2% in FY 2015 to 4.5% during the nine months.

OPM is expected to improve 50 basis points in FY 2017.

By 2020 the company plans to achieve sales of Rs 1000 crore. New products will drive growth. With new products the company hopes to grow 20% each year and double sales in 5 years. It hopes to add Rs 250 crore by way of contribution from new products.

Sales can grow 25% in FY 2017 with 50 basis points improvement in OPM.

Sales from TLT can contribute to Rs 6 crore in FY 2017 and this is going to be continuing business.