Can it be beneficial for Indian players as well?

IMO, all these discussions about China capacity cuts is just meaningless. They need to show the world that they are doing something or they will keep getting wrap on the wrist on the trade front. One needs to follow actual production which is elevated and will remain so. Has China steel import threat gone away? a clear no! Also, when China capacity utilisations are not even 80% how does it matter if few tens of mt capacity is shut for various reasons. Steel prices depend on raw materials and market tightness. China domestic market has incrementally tightened but capacity cuts has little role to play here.

1 Like

I think the hikes are happening due to import curtailment. The price hikes will support raw material price escalation. Overall in the short term margin appears to be supported.

Disc: Invested in SAIL

Even though the net realizations and EBITDA per tonnage was down it was known to market and was priced in. What do you think is the primary reason for sharp fall today ?

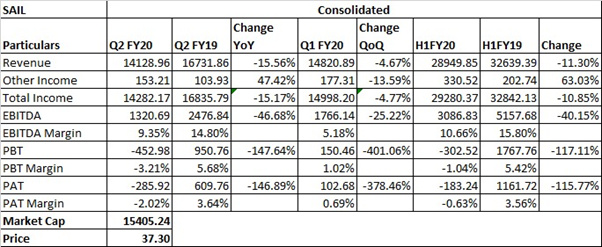

SAIL Q2 Results!

Concall:

So briefly about the market conditions, the steel industry is witnessing very difficult condition. There’s a lack of demand in the market. Prices have been slashed significantly. And the international prices also have come down from about USD 489 for cold rolled coils by about almost $100. This has lasted about 8 to 10 months. And it is hurting the margins of products because we also have – of course, the fall has been more in the flat products rather than in the long products. It has fallen everywhere, but in the flat products, the fall has been a series in this range of around 16% to 19%. And our biggest market where SAIL operates is construction and infrastructure market, where since March, there has been a decline there about 15% in this sector. All the other sectors like automobile, white goods, they have also seen their output contracting.

If we compare our results with Tata, JSW and GSPL, almost all of them have shown negative growth in PBT. The difference is that, in fact, of course, we’ve slipped into minus because we didn’t have much of a margin in the first place. So this is where we stand now. And there are some, of course, positive signs, that is a rebate which was coming almost to the tune of INR 1,000, INR 1,500 every month since April. So in the month of October, it seems to have flattened out. And low rebates have been passed on in October. In fact, there are – there is some news that there’s a pickup in the – especially in the [longer rate] by about INR 500 to INR 600. And this could be a blip or maybe it could sustain also. We hope it sustains.

The government has also announced a number of measures like the Pradhan Mantri Awas Yojana and the construction of roads where about some INR 1 lakh crore has been budgeted. The World Steel Association has also revised the growth upwards in October in 2019 to 3.9%. And some other schemes of the government which has been announced, but they are yet to actually hit the road, especially in the highway sector and the housing sector, the sectors which actually impact SAIL more rather than automobiles and all that. So with that coming and the prices at least stabilizing, we’re hoping that the third quarter and maybe more of the fourth quarter, things will start improving. There is some marginal uptick in the demand. The demand is slightly picking up. Our inventories have started liquidating a bit, but we’ve cut back production because of our large inventory. We consciously cut back production because it’s producing and putting to stock. That was hurting the financials a lot, and therefore we have consciously reduced that scale of operation. If things improve, then again we’ll start picking up.

One is that government has allowed SAIL to sell its ire ore lumps and fines in the market up to 25%, and that is expected to bring in a lot of, not only cash and also profit. Also, government has allowed SAIL to sell the sub grade fines which we are holding, which is huge, which is like some 70 million tonnes in all our various mines, and it has a good demand in the market. So we are in the process of taking all the statutory clearances and the environment clearances, and we’ll go on other things necessary so that we can start selling that. That is actually a waste product. It fetches a good price in the market. The quantity we are holding is massive. And if the sale of the sub grade fines coincides with the pickup in demand and a pickup in prices, I think at least Q4 onwards, we should start seeing something good.

Iron Ore Lumps/Fines: Okay. So there are 2 things. In September '19, the government issued 2 circulars. One circular said that we can sell our normal production, both lump and fines, the things that we consume in the plant, and there is a capping on that. What we can sell is 25% of what we produced in the previous year. So in '18, '19, we produced 28 million tonnes of iron ore. So now this year, we are permitted to sell 7 million tonnes of iron ore. This is good ore. Next – and here there is a 2 years gap, but – 2 years time, that we have to sell this 7 million within 2 years. This is [luckily] the good material, which fetches a very high price in the market. But the thing is we – because we have our own steel plant, we won’t be able to sell too much of this good material. We will be selling something, we’re already in the process of issuing tenders. Wherever we have surplus iron ore fines, that we’ll be selling. And we’ve also made plans for generating a little extra material, extra lump and extra fines that sort of after feeding the steel plant, any surplus that we have, we can sell in the market where it fetches a good price. But what we’re really looking at is the sub grade material, the generated fines and the tailings which we have accumulated over the last 50, 60 years, and where we were not permitted to sell, but there was a good demand from the – with pellet plant maker for this material. So they wanted this material, we had tonnes of this material, but there was a barrier which prevented us from selling. Now that government has removed the barrier, there is no embargo either on quantity or on type. So we can start – only the statutory clearances, as I said, are required. So the initial time line that we promised will start auctioning from February of next year. But this material is lying in various mines, so as and when we get the clearances from the various states, we will start dispatching from those states. For example, in Jharkhand, the model code of conduct has started because of the election. So the Jharkhand clearances will take a little time, but we also have mines in the state of Orissa and Chhattisgarh where we expect the clearances to come. And the mines in these states will start selling first. So this year, probably up to March, we won’t be able to sell very much, but we’re planning lot of sales in the next financial year, '20, '21 and so on. The amount, again, it’s very hard to say. The asset 70 million tonnes is – has not been assessed. So we need to physically verify the quantity. It may be – it may not be 70, finally, when we get it surfaced through drone and all that, it may be 60 million, 65 million. But the price that we find from the IBEF price surplus are – vary from 700 to 2,200 depending on the Fe content. So even if I take an average price of 1,000, it’s a lot of – it’s a bigger one. See, our mines are mechanized. So we – so far, we’ve been producing to the extent that we need for consumption because there’s no point in producing and keeping tonnes of open stock. And so we are – actually, we used to a keep a control on the generation of ore at the mines, but now that we have one more avenue open and we have enough reserve, so we’ll be increasing our contractual quantities to produce more of lumps and fines. We have the capacity. We used to curtail our production to the extent we need to consume. So now we can expand a bit more. But at least that can’t be done overnight. We need to put certain things in place, we need to give some more contracts, we need to clear space for dumping them. So some things are required, but then we’ll be ramping up our production so that we can also sell some portion. So far, what you had said, this situation will never end.

Cost Cutting Initiatives: The kind of initiatives, what we have been taking we’ve been discussing, actually, these are falling into maybe 2, 3 kinds of categories, if I didn’t talk about starting with the fixed cost. Obviously, the most important thing before us is the employee cost. On that front, we’ve been taking measures like bringing – coming up with the VRS schemes, another thing to reduce the manpower number. Plus the compensation side, we cannot control being a government company. We are guided by the EP guidelines and all. So those, we cannot fully take into account, but we are looking at reducing the numbers, naturalizing them and redeploying then reverse approvals by [scaling] and all and controlling the recruitments as such. And as soon as the production would increase, the certain impact of the fixed cost would also itself come down. Coming to the variable cost, definitely, there are certain areas like, most important of them, again being the coal consumption and the other raw materials like iron ore and all. So coal rate, coke rate, what – the rate has decreased and [consumer] coal is also coming down over the period. As we shift to these new capacities, these get ramped up, we shift fully to these from the old facilities, the efficiencies would improve. So the conversion level for these inputs and all also would come down. Apart from this, the other conversion costs, the administrative cost, we are taking measures to control them in whatever way possible, like the power cost or if you talk about security costs and other related costs.

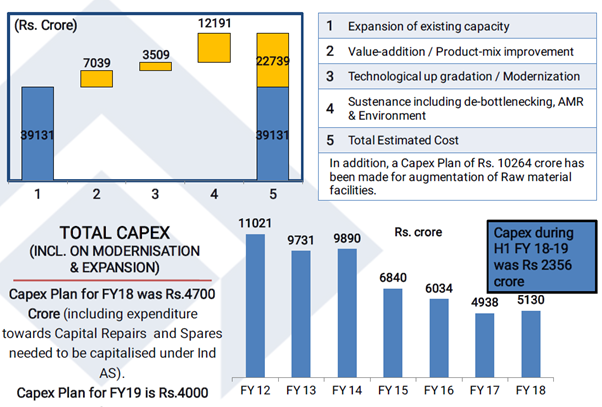

Capex Plans: The guidance – I’m going to say, on the raw material side, we had CapEx of close to INR 10,000 per tonne, close to maybe 1,500-odd up to now. This is majorly because the 2 most important mines, that is Gua and Chiria. These are not having the easy clearances now. So we are not able to really move anything ahead of those line – these mines. Also, Rowghat, we had planned something, but now that we have gone for the NDA route in Rowghat, so that CapEx altogether for Rowghat at least may not be required. Coming back to Gua, we have got certain clearances – forestry clearances in the current year. So as soon as we – sorry, the lease mines – leases have been clear for us. The forestry clearances have come from 1 or 2 leases out of that. Only one of them that is the Durgaiburu lease which is pending now. So once that comes up, we would be taking up CapEx and we will approve the leased area. This would help us to ramp up the production from the other leases of the Gua mine. Chiria is still pending, and then when we get it, we’ll definitely look at the CapEx from that side also.

Closing remarks: So basically, we are all hoping that the market improves. There are some signs that it’s improving. We hope these signs are [seen] and things improve. And maybe in the last quarter, we’ll be able to post a good profit, with good prices coming, the demand picking up or iron ore sales picking up. And definitely, we are hopeful that next year is going to be good, but we are hopeful for Q4 also.

1 Like

Nice presentation @Lajja_Shah. Though it is common perception among the investors that a PSU can not create substantial wealth for investors in the long run, the turnaround in SAIL’s

performance on some important quantitative fronts seems to present a promising picture with improving fundamentals of late.

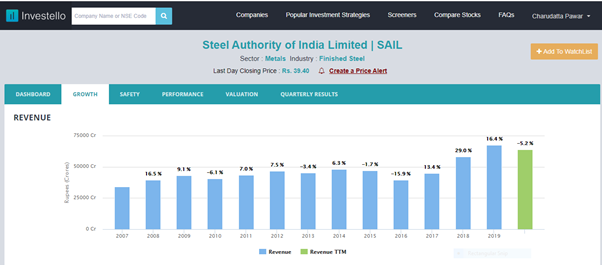

Let’s analyze the growth of SAIL in last 10 years .

Following is the chart for revenue of SAIL :

As from the graph, we can see that though revenues were not on consistent growth trajectory for initial stages of last ten years, It has been increasing since last four years which is good sign reflecting the improving sales figures.

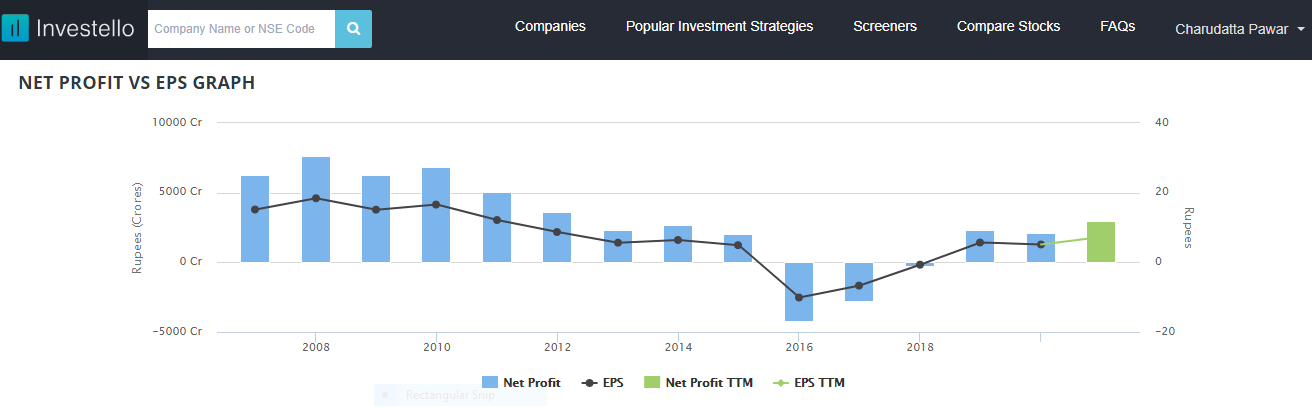

Lets see how the stock is doing on Net Profit front:

Along with revenues , Net Profit should also increase over time to reflect the profitability of the company. So as we can see profits for SAIL are increasing in last four years after being in downward spiral for most part of the last ten years. This indicates that company is improving in terms of profitability.

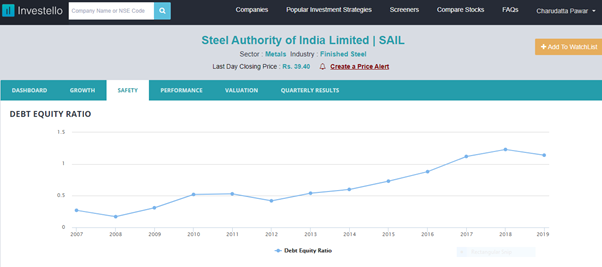

Now lets check for some safety criterion :

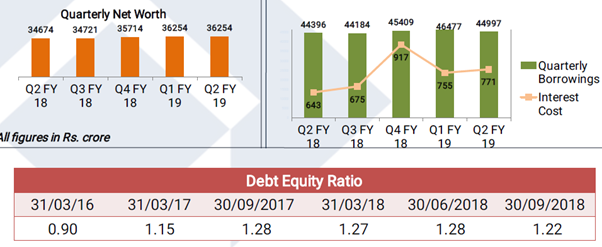

Above graph shows debt to equity ratio of SAIL for last ten years. And as we can see its debt in proportion to its net worth is increasing . Though debt-to-equity levels are not alarmingly high , but still it present a concern area which needs to be addressed.

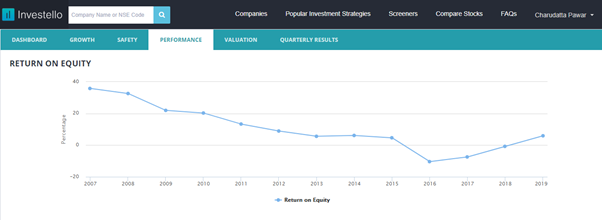

On performance front, SAIL has been improving in last few years when we consider at RoE as performance metric, which is visible in following chart :

From above chart we can say that its profitability with respect to its assets is on recovery track which is a good sign , specialy in the subdued economic circumstances . This can also be justified with another performance metric such as cash flow as represented in following chart :

The above graph indicates that negative cash flow is decreasing on a regular basis since last few years .Then it should suggest that the firm is recovering well, and the long term strategic growth is intact.

So after analyzing various Growth, Safety & Performance metrics for SAIL ,we can sum up that if the debt concerns are taken care in strategic manner, SAIL can realy be considered as Value Stock which possibly can justify the thread title " A Long term opportunity"

3 Likes

The government has allowed state-run Steel Authority of India (SAIL) to sell 25 per cent of its iron ore produced from captive mines and dispose old stock of 70 million tonnes (mt) of low-grade iron ore mines and ores lying at mine heads across the country.

The ministry of steel has stated that more than 162 mt of low-grade iron ore are available at mine heads in India, as the regulations do not permit SAIL to sell these materials to domestic end-use companies.

The move by the ministry through two separate notifications on September 16 is seen as an effort to reduce concerns regarding the expiry of mines. Thirty-one working mines of iron ore are expiring on March 2020. SAIL has the capacity to enhance iron ore production from its captive mines by around 8 mt in 2019-20 and 12 mt by 2021-22.

“The government has given permission to sell 70 mt of sub-grade minerals in the captive mines of SAIL,” the ministry of steel has tweeted. In order to increase evacuation from captive mines, the government has allowed SAIL to offload in a year, up to a quantity equivalent to maximum 25 per cent of total iron ore production in the previous year. For this, the company will have to get clearance from state governments. The government expects the move will help SAIL in meeting its own requirements and also meeting the expected shortfall in domestic iron ore market.

One of the major reasons why SAIL was unable to consume low-grade ores was because the company was not having enough beneficiation and pelletisation capacity. Major states that will come under such captive mining areas of SAIL include Jharkhand, Odisha, and Chhattisgarh. The order will be valid for a period of around two years.

On an annual basis, SAIL’s captive mines reportedly produce around 28 mt of iron ore. According to media reports, SAIL’s captive mines have iron ore resources of around 3,700 mt, of which a large chunk is coming from Jharkhand.

any idea what could be the value of such huge iron ore stock and its effect on the short term result ??

Low grade iron ore (I think <58% Fe) is exported to China in the past by miners. There is enough low grade iron ore stock with the non captive miners (kiocl, nmdc and other merchant miners) already. Govt. recent order to allow sail to sell iron ore from captive mines may not be beneficial if it is low grade iron ore.

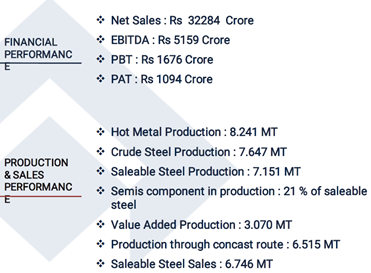

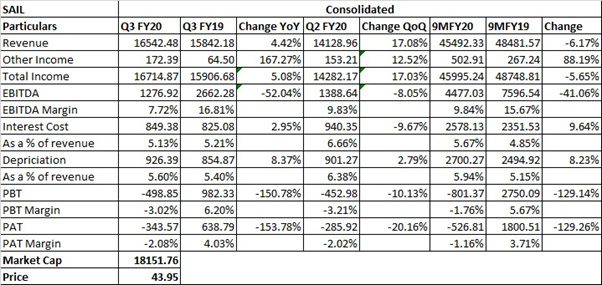

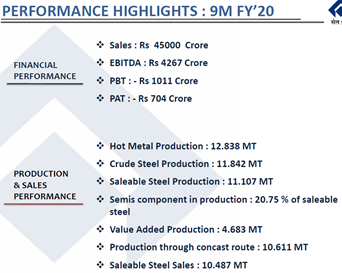

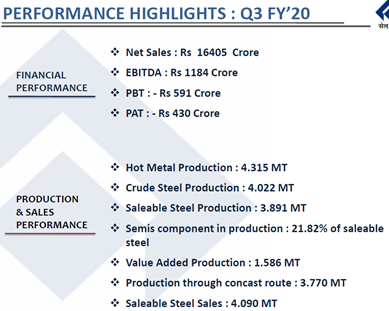

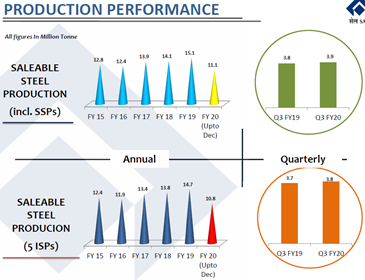

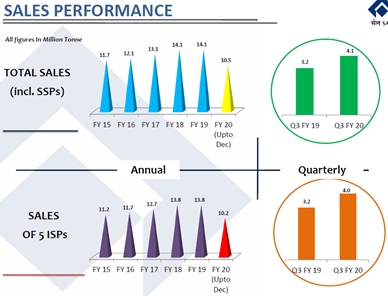

SAIL Q3 Results!

Q3 FY20 IP:

Q3 FY20 CC:

- Q4 FY20 will see improvement.

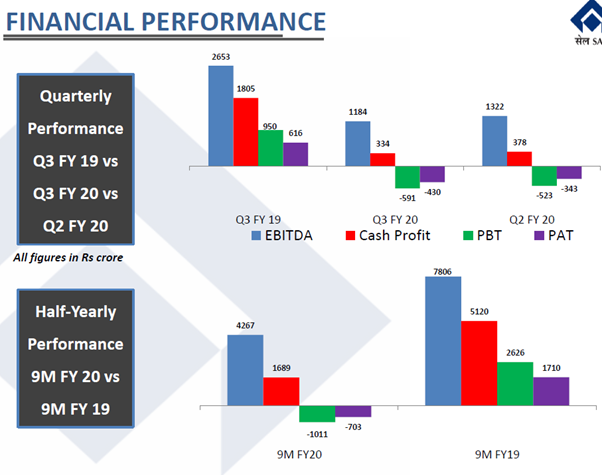

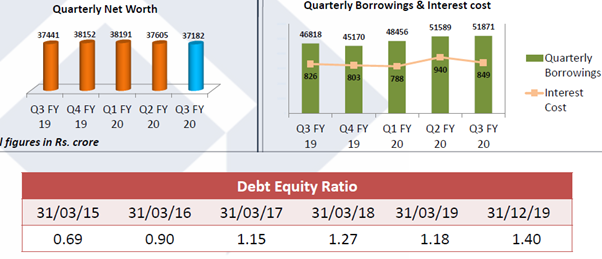

- So the – coming to sale, in particular, our sales volumes picked up in November and December, growth being about 37% over CPLY in November and were 48% over CPLY in December. The finished steel inventory, which had risen to about 2 million tonnes in October, we have managed to bring it down to about 1.3 million tonnes, which is roughly at the same level that it was on 31 March. The borrowings, which had crossed INR 51,300 crores at some point, again, in October, has been brought down by about INR 700 crores till 31 December. And we have posted a loss of about INR 430 crores BT in Q3, which is a reflection of all these things, but hopefully, going forward, the fourth quarter, we expect to be good.

- The steel industry is making a revival. The demand of steel is picking up. Prices have started firming up. The government has made many announcements in the budget, and we are very hopeful that they will lead to an increase in demand. One of them being that investment of INR 103 lakh crores in infrastructure over the next 5 years, that national infrastructure pipeline, which comprises of more than 6,500 projects across all sectors. So this should give a big boost to the steel demand. And there are developments in the waterways, railways, freight corridors, all of these consume steel. INR 107 lakh crore has been allocated towards the transport infrastructure for highways, economic corridors, coastal and road ports. Economic activity along the riverbanks has been energized. 100 more airports under the UDAN scheme has been announced. So if all these really happen, and we are hopeful that it will happen, then Q4 and the year ahead, the next year, 2021, is likely to be good.

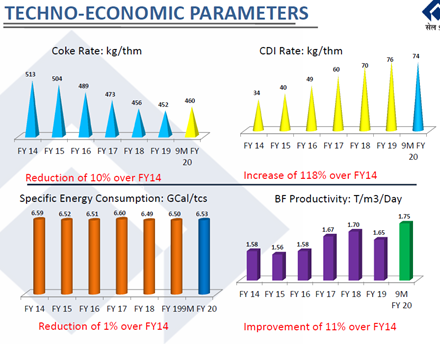

- Coming to the results. The turnover in Q3 has been INR 16,405 crores. EBITDA was INR 1,184 crores, which roughly translates to INR 2,900 per tonne. PBT was minus INR 591 crores. And after ducking for deferred tax assets, the loss after tax comes down to INR 430 crores. There was – there has been some improvements in the techno-economic parameters. And the coke rate has come down by 5%, energy consumption by 2.5%, BF productivity has gone up by 12%. CDI usage has also increased by 40%. Of course, this is subject to the availability of CDI. So we have some supply side issues with some of the suppliers, especially the Australian suppliers. So subject to availability of CDI, we are trying to maximize the CDI usage. And most of the plants are now in profit – of course, now means, I’m talking of Q4, are in profit. So we hope this trend to continue.

- Most receivables are from Railways

Disclaimer: Invested

1 Like

Nice write-up Sir, bt I see the analysis was done in Feb.

-

What’s ur view of the demand scenario post-covid and how u feel SAIL is positioned competitively for dat

-

I blv u also keep a tab on Steel commodity cycle. Thr seems to be some pick-up back in China, bt how u view the overall cycle pick-up for 2020-25 period now?

“Sail will out perform major steel stocks by a wide margin. Two main raw materials are coking coal and iron ore. Historically the price of iron ore is about 65% of that of coking coal. ie 100 and 65. However now is has moved to parity with iron ore pricing moving up and coking coal prices moving down. That is because 70% or iron ore is imported by China and this steel boom is driving iron ore prices to almost 119 USD per tonne. In Yuan terms the price is up about 42% year on year. Sail has huge captive iron ore mines and to top it up last year to ease the pressure due to the mine auctions the government has allowed SAIL to sell upto 25% of its capacity in the domestic market. On the other hand the other big input cost of Coking coal is down sharply to about 115-120 per tonne or so. Thirdly SAIL is mainly into long products with a large amount of sales so Rails and other steel products to the Indian Railways. Most of the expansions have kicked in and they are stabilizing now. Labour cost has also reduced with VRS etc. Globally steel prices are going up. So with many tailwinds the moment results surprise the market the stock should be on its way to hit 75 very soon. Big brokers who have shun this stock due to the PSU tag will suddenly re-rate the share and then everyone will suddenly show their new found love for this share”

Somebody has posted this analysis in Moneycontrol. I am just reproducing it.

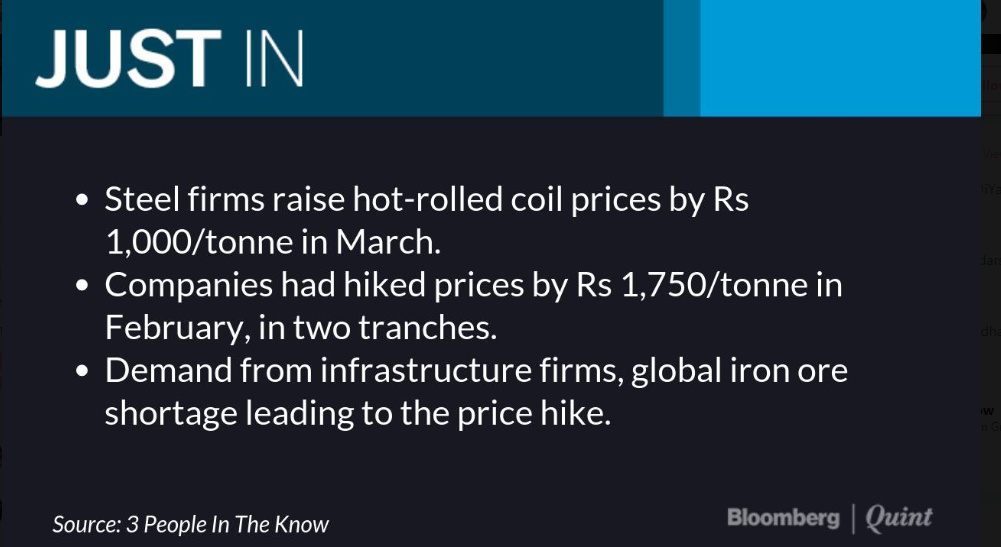

Got interested in SAIL in the last few days as we keep reading about sudden spurt in Iron ore prices and India after quite some time, exporting considerable amount of Iron Ore to China in July and overall twice the steel prices has been increased by all Indian companies in the last one month. I hold Maithan alloys in my portfolio and we are seeking considerable price action in the last few days and for that matter all steel companies prices has increased. Overall, commodities stock are moving upwards.

I talked to Jindal power CEO who was earlier in JSPL and he agreed to the above assessment saying its fairly correct assessment when I posted to him. They were selling semi finished products like billets to China till last month as they wanted to ensure cash flow keeps coming and now selling more finished products to customers like Railways as the demand has picked up and obviously margins are also higher.

will this all benefit SAIL as the price looks attractive compared to JSPL or the likes of JSW steel ?

2 Likes

Here are some more signs of the wave that SAIL is “sailing” on:

June 2020:

July 2020:

My reading is that SAIL has had a tough Apr, May. But June onwards, it has seen good times. The share of long products has helped its cause for sure. And the company has truly been trying to make itself more efficient. If you look at employee count and productivity trends, it tells a story. At the price SAIL is trading at, I too believe that the upside is not priced in.

Discloure: Invested

1 Like

What this means is that Jun’20 quarter results may not be great (since Apr and May could act as a drag). So may have to wait till the Sep quarter for all this to show properly in the results. I have no clue on price action though…will the market suddenly decide to price this in even before Sep quarter results are out? Perhaps.

Disclosure: Invested

And…the momentum continues in August 2020.

1 Like

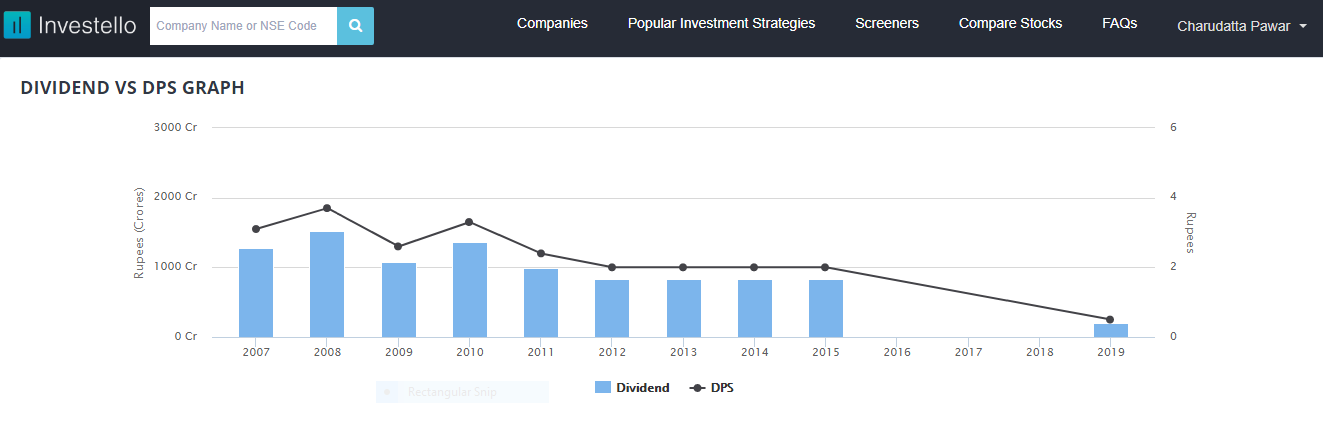

In the last few years SAIL hasn’t distributed dividend for three consecutive years which seems to be in tandem with its financial performance:

As we can see, while distributing dividends they have taken into consideration the financial condition of the company and have kept pace in terms of profitability as well. That’s why no dividend in the last few years unless the company returns to profitability. I think that makes sense (unlike a typical PSU where govt always desires to squeeze maximum dividends every year being a majority shareholder) because the company’s dividend payment policy should be a reflection of its financial performance. There is no doubt that dividends function as a reward for investors, but seeking a balance between growth, safety & dividend is more profound way of generating confidence in a company’s stock.