Safari Industries and VIP Industries coming out of ASM from tomorrow (30th Oct, 2018).

Source: BSE (formerly Bombay Stock Exchange) | Market watch - Download

Annexure.xls (57.5 KB)

Refer Annexure III in the above file.

Safari Industries and VIP Industries coming out of ASM from tomorrow (30th Oct, 2018).

Source: BSE (formerly Bombay Stock Exchange) | Market watch - Download

Annexure.xls (57.5 KB)

Refer Annexure III in the above file.

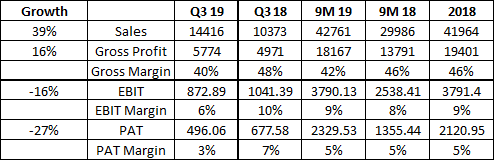

Good Operating performance continues from Safari. Half Yearly Gross Margins maintained ~44%. Nice improvement in Half Yearly operating margins and PAT margins.Good topline growth as well.

Quarterly margins have decreased sequentially and yoy as well indicating many things. Unlike VIP which follows the average cost method, Safari follows the FIFO method, so lower cost inventory gets expensed first and higher cost later ( assuming an inflationary environment ), causing fluctuations in gross margins quarter on quarter.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/5654eafe-caff-405d-aa8a-f71a665e3ccb.pdf

Lastly, it looks likely that safari could close fy19 with an EPs of 15. This coupled with a further drop in share price will bring multiples closer to rational levels forming a good strong base hopefully. Once there is some base formation the intent is to summon up the courage to add.

Best

Bheeshma

Disc - invested

Hi Bheeshma,

The total operating expenses have been more or less the same on qoq basis. The only reason operating margins were higher in Q1 fy19 was because of a very high sales no. on an absolute basis, ~150cr.

It was also good to note that receivables have come in control keeping in mind a very strong sales growth witnessed in the quarter.

It’s good to see a 120 cr sales mark in an ersthwile okayish quarter, talks of the tailwind or the tipping point this industry has hit. I’m excited to see what they post next quarter owing to the festive season and multiple online melas. The change in inventory no. could be one clue but let’s not read much into it.

Cheers.

Disc. - Invested

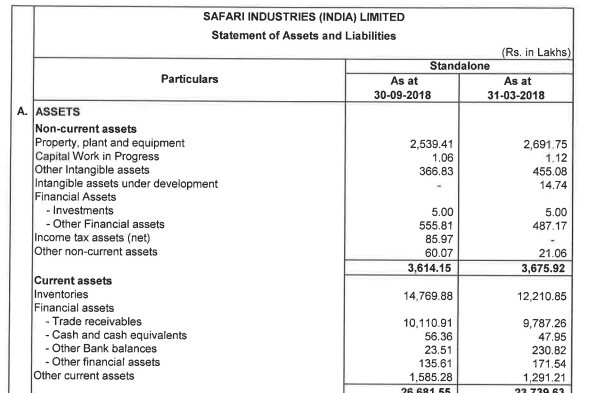

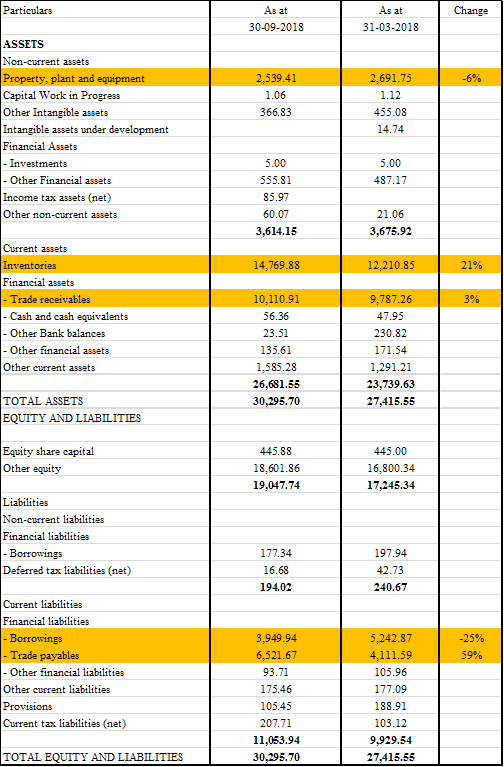

Yes, on the balance sheet front - there are signs that tied up operating cash has been released. Inventories + receivables ( the two main operating assets) as a group are up by 13% while payables are up by 59% viz a viz Sales growth which is 40-45%. Receivables is up by only 3% indicating good collections.

Short term borrowings as a result of this cash flow are also down by 25% , but compensating for that are the higher interest rates leading to a slight increase in finance costs.

Improvement in balance sheet is a good sign.

Disc - Invested

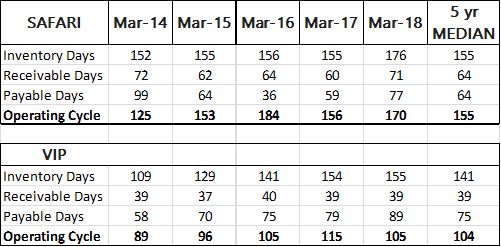

The operating cycle for safari and vip gives some additional insights into the sector

Luggage is characterized by a longish operating cycle, which means that working capital requirements are high in this sector and growth will necessarily mean additional investments in working capital.

Source : raw data is from screener, calculations are the authors.

Inventory days , is the biggest component of the operating cycle and requires the most attention for a Luggage co. Inventory days has been steadily increasing for VIP while for Safari it has remained constant.

In fact, in 2017 it was the same for both the cos. 2018 was a year with inventory stocking it seems and inventory days is higher, but broadly there is a increasing trend for VIP. Both the cos are roughly similarly matched in terms of this parameter, if you look at very recent history. Both the cos take similar time to sell luggage

Payable days, are slightly better for VIP than Safari but not by a huge amount however, 10 days additional leeway given by suppliers is a meaningful. However, Safari seems to be making some progress here as it scales up. Broadly though, since sourcing is the same cos are not different here.

Receivable days, however is where it lags VIP and clearly VIP is doing a far better job at collecting cash from its customers. The days receivable have remained remarkably constant for VIP at 39 days in the last 5 year period highlighting its domination.

The table highlights that Distribution is the area where Safari has made rapid progress and is now able to sell inventory in the same time it takes VIP to sell it.

Best

Bheeshma

Safari uses FIFO for inventory accounting while VIP uses weighted average, we need to account that also looking at the inventory days, in a normal inflationary trend Safari will always have higher inventory days than VIP.

Yes, there is some variance in the working capital ratios that I have calculated vs the ones in the credit rating report. So it could be due the accounting methods followed. The plus is that they have utilized 44% of bank limits which is good and gives them room to grow. This industry is working capital intensive and will always need access to short term credit. As long as the coverage ratios are within manageable limits its all good. To me thats a key moniterable as I would rather have moderate growth than a stretched balance sheet. So far the mgt has achieved that balance nicely and hopefully it will continue to pay equal attention to both p&l and balance sheet

Best

Bheeshma

I am relatively new to this thread. However, this response should be taken with a pinch of salt Established brands have a tendency of writing off new brands or technology and ultimately have to eat up their words with embarrassment. This is particularly prominent about tech disruptions across industries.

Coming to Mi, they have built a strong customer base and would not be surprising if they gain a foothold in the luggage market. Also, I do not see any technological innovations (smart luggages) from the incumbents and it is something Mi and the likes can easily leverage to enter the market.

My views are purely from a customer’s stand point along with a decent understanding of the retail world.

Disappointing results from Safari

38% increase in sales whereas 28% decrease in profits (YoY)

Safari came up with a mixed set of results in line with its counterpart VIP industries. While the 9M & 2018 results are stable with a PAT margin of 5%, the YoY margins have been impacted primarily due to raw material costs. The good news is increase in sales YoY. The 9M PAT of 23.29cr is more than the full year PAT of 2018, so even if the co finishes Q4 with the same nos as the last Q4, it will still do a growth of 35% to 40% for the full year. Overall, the business is stable with stable margins and is growing well. Raw material hits are part and parcel of the business and are likely to be transient and temporary.

Hi @bheeshma,

Good to see your analysis. I was scared seeing the results. But your words helped restore confidence.

I had the following doubt.

While it is known and evident that the crude price had affected the margins of VIP and also Safari, if we see the below image, there is a huge rise in expenses due to purchase of traded goods. The raw material price was higher for the Sept 18 quarter. Does rise in “purchase of traded goods” is an indication of the effect of crude prices or is there something else to it?

Basically its the combined effect of rupee depreciation and addn 5% customs duty that govt levied from Sept 18 onwards.

good to see safari change its website from safari.in to safaribags.com , in line with the vip site - vipbags.com

Yes Q3FY19 was difficult for luggage companies due to a depreciating currency and increasing crude prices.

However this is one space, where unorganized to organized shift is quite visible post GST. Safari and Aristrocrat (VIP brand) have been posting great volume numbers.

Q4 margins may also be a bit subdued however post then it should normalize. Good stocks to hold in consumer discretionary space.

What is the theory behind Margin normalization post Q4. Is VIP and Safari going to take some price hikes?Or there are some other triggers as well.

Yesterday I was watching History Channel and came across an ad of Safari Bags.

I was pleasantly surprised to see this nicely done ad.

While searching for this ad on youtube, I got to know that they just uploaded it 12 hours ago.

Happy to know that they are doing the right things to increase visibility which might add to their top line.

@bheeshma How does a TV ad translate in terms of expenses for such a small company?