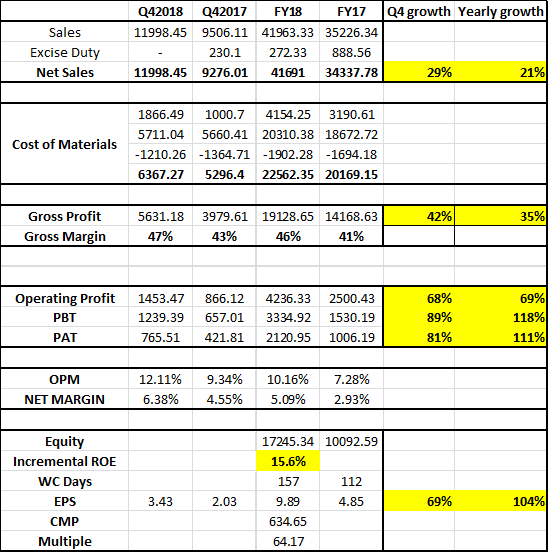

Safari has posted a good set of results again. Operating Leverage impact is apparent. The good thing is the growth in the gross margins which is a good sign in a competitive environment. YoY it has improved from 41% to 46% and Q42018 it is 47%. The Operating Margins have also improved from 7.28% to 10.16%. There is an all round improvement in margins.

The topline has grown more than the industry average (15%) at 21% YoY and 29% QonQ. VIP which usually publishes results before Safari has opted for the first time to publish results after Safari ( VIP results are tomorrow ), so one must compare performance against VIP. The growth in sales has clearly been driven by aggressive WC investments which have gone up from 112 days to 157 days so that is something to ponder over and a negative.

The incremental ROE is 15.6% which is ok and still needs a lot of improvement

All in all , its an aggressive performance in a competitive market.

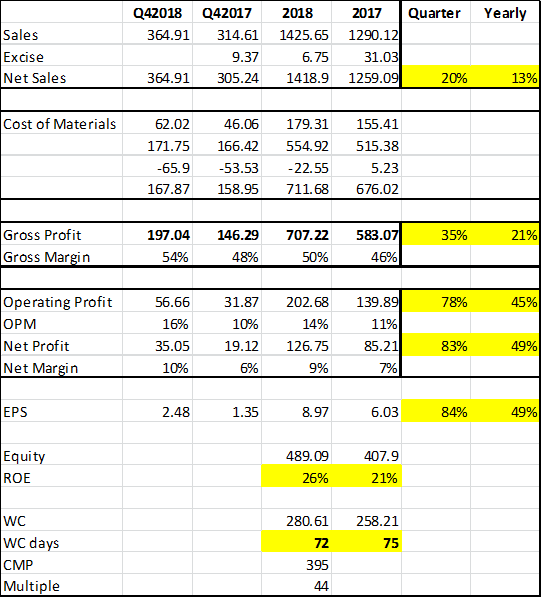

VIP is also out with its numbers and they are also very good. The working capital days have reduced to 72 days for VIP from 75 compared to Safari which have increased. The ROE numbers for VIP have improved to 26% from 21% earlier. Infact, its incremental ROE is upwards of 50%. The VIP topline however has grown by 13% in sharp contrast to 29% of Safari. All in all a great show by the luggage industry.

While the title of the news story says resume padding - the resume irregularities are just a small part of the short sellers report. Hong Kong based, Samsonite is a large player in the luggage market and indeed in India as well. It seems that auditors of its indian subsidiary have resigned 2 times and its on its 3rd auditor in 3 years. Add to this there are some questionable purchase accounting tricks and inventory valuation gimmicks claimed in the report.

The main allegation that caught my attention is the channel stuffing through its indian subsidiary bagzone and compares Samsonite to a mid level “walmart” kind of a brand. Its inventory turns in Asia are 5 - 6 months which are roughly similar to those reported by Safari but VIP has reported at 80 days in 2017 - so there is a gap there.

All in all its a great report and gives a lot of insight into the business

It’s good to see Safari being promoted by Social Media Influencers.

Internet is a cheaper and a focused alternative to reach one’s target customer, a good facilitator to a business without a fat purse for marketing dollars.

There are some risks as well. The main one that i can identify is the longish working capital cycle. Luggage is a consumer durable and the replacement cycle for its products is rather long maybe 3 - 5 years or even more. Even so, VIP has a much shorter one.

Currently the co is in the mode of expanding its reach but over time the key differentiator in the luggage sector will be the brand as all products are roughly the same. By brand i dont mean the ability to charge more but developing a line with different price points and varying product perceptions in line with customer needs.

Sudhir Jatia has done a good job and from the looks of it the culture of the co has also undergone a transformation. In a sales oriented co, the culture is all important and often the main difference between a good co and an average co.

Thanks for the info. ASM framework is to check volatility in stock prices i think as margin requirements are 100% + 5% circuit. Not aware about reasons behind volatility except expectation of good numbers in line with VIP.

Very good numbers again for Safari. Topline up by 49%, Operating Margin up to 14%, PAT Margin up to 7.8% ( VIP PAT margin is 12.1% for Q1 ). PAT growth of 272%

I attended the AGM of Safari today and there’s every reason to believe that we are in for good times as far as business is concerned. The market also doesn’t have a reason to think otherwise and that makes me a bit jittery.

Few points worth mentioning are as follows,

-The deterioration in WC is more by design than by default. The co. took a conscious call to advance shipments from China last year looking at rising costs scenario. (One reason for bump up in margins for June quarter is advance purchases made at lower costs.) Forward contracts were closed in advance. (When asked if such calls could also backfire, Mr. Jatia said it’s a call an entrepreneur has to take.) This led to cash flow tightening. The receivables have shot up because March quarter saw revived sales to CSD and increasing quantum of sales to E-Com and Modern Trade.

The WC situation will ease off in due time and is a top priority for the management.

-The co. is at a juncture where it has to take calls between growth vis-a-vis margins and growth vis-a-vis cash flows. The co. is trying to balance out in the best way possible.

-Sustainibilty of margins shown in June quarter is a concern. Management will try best to maintain the same or not let it slide by a big chunk.

-Polycarbonates and Backpacks are doing really well. The sales of backpacks have crossed the Rs. 50 cr mark. Polycarbonate capacity at Halol is operating at 100% capacity, 25% capacity expansion to come up soon.

-The co. will only focus on existing brand and remain at the existing price point as current market offers great opportunity and the co. seems to have hit a tipping point.

Disc - Invested and Biased.

P.S. - I’ve tried my best to present a fair picture but there could be some lapse in my understanding and members should be careful about the same.

Xiaomi launched two new suitcases under the Mi Luggage moniker with varying capacities. The Mi Luggage comes in two variants—Mi Luggage 20 and Mi Luggage 24. All of them feature Bayer makrolon polycarbonate coating on the outside, TSA approved locks, and 360 degree shock absorbable wheels.

The Mi Luggage 20 is priced at Rs 2,999 while the Luggage 24 is priced at Rs 4,299. These will be available from October 10 on Flipkart and Mi.com

I had a conversation about the Mi Luggage launch with Mr Vineeth Poddar, CFO - Safari and some points that were discussed are as follows

We are aware about the Mi launch and we dont think it will make a meaningful dent. The top 3 brands occupy close to 95% of the organized luggage market and that’s not going to change in the short term

The online market is less than double digit currently so while its an emerging channel, it requires huge offline presence.

However, we dont underestimate any brand, big or small.

The tailwinds of GST and migration to branded are still in place and will remain so.

Bheesma , VIP and Safari have corrected significantly over past few days. Today were in Lower circuit. As you are tracking closely, with sector tailwinds and high growth visible do you see right time to nibble further on some stability.Earlier promoter has bought VIP significantly around 400 levels.

Both VIP and Safari are good cos in my view. Vip has good free cash flows and strong brands additionally. Whether to buy or not at current levels depends upon your investing style and temperament which is not a very helpful answer

I think this sector can grow at 10-15% over a reasonably long period and all players within this sector can benefit from it.

The stock has been quite resilient despite high valuation. A few fundamental factors have turned … sharp Fx depreciation has twin impact of discouraging travelers and making luggage imports expensive along with higher taxes. Are we not running the risk of giving back some market share to unorganized sector? They would need to shift manufacturing to India faster than expected.