Based on the updated chart and a number of assumptions (mainly that compared to the previous year, revenue will change in proportion to change in “export value”–this is approximately true for the last two quarters and SNCL is the largest exporter), I am expecting a revenue of around Rs 60-70 cr from MAP.

ODB2 may contribute (as high as) Rs 30-45 cr (250mt * 3 months/12 * Rs 6000/kg is Rs 37.5 cr).

Disclosure: Holding. SNCL is 3.5% of my portfolio now after share price has fallen to 715.

I am expecting a flat Q3 sir. Total sales around 85 crores. Let’s see

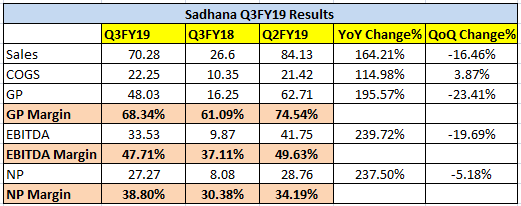

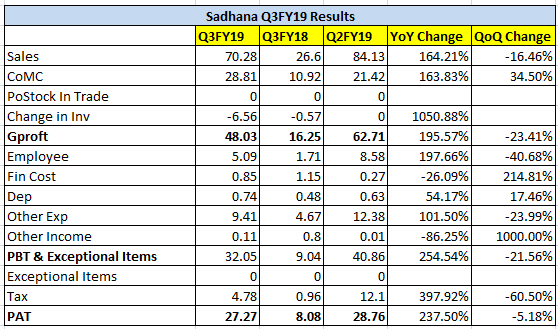

Lower gross margins and revenue, as expected, because of lower MAP prices. Lower tax this quarter has bumped up bottom-line. Adjustment to bottom-line with appropriate tax would be prudent. Will be interesting to see when will margins come back to normal levels.

What is the reason for lower MAP prices in Indian exports? Is it a short-term trend or a more persistent trend?

Considering that SNCL claims to have 90% market share in the domestic market, is it reasonable to assume that SNCL long-term contracts have a big part in determining the export price from India?

If yes, it would be good to know the MAP import/export prices in China, US or other importing countries. Does anybody know how to get that? Then, we can determine if the lower MAP prices is a short-term trend or a more persistent trend.

Another interesting part is the ongoing process of acquisition of Spidigo Net, right after completion of the acquisition of Strix Wireless. Does anybody know what’s cooking there? A few years earlier, the company tried to venture into computer networking but it did not work out very well. But, it means they have some experience in the field.

Spidigo Net and Strix Wireless are completely irrelevant to chemical business, is there a company related history to justify this?

They are trying different business to get diversified.

There have been multiple lower circuits. Anything structurally off with the business ?

No idea—the business seems intact. However,

- BSE Smallcap Index has hit 52-week low.

- Market does not seem to like the company’s new diversification into networking.

Disc: holding.

No wonder the risks are significantly higher with small caps.

Its not feasible to contemplate potential reasons for a share price to go down by so much. Rising 20x with favorable macros and then falling by 60% on account of diversification ?

Disc : No Holdings

A bit about SNCL’s foray into networking. As per SNCL Annual Report 2009-10, Lifestyle Networks Ltd (LNL) was a partially owned subsidiary of SNCL.

LNL in Joint Venture with Chandra Net Pvt. Ltd. has been able to successfully role out

fixed wireless network of 90 sq. km. in Ahmedabad under the brand name of ‘SPIDIGO’. The network started functioning from September 2009 and has more than 170000 customers.

As per Spidigo - Linkedin:

Using state-of-the-art Wireless Multi-Radio Mesh Technology from Strix Systems, Spidigo offers unmatchable connectivity and speeds.

Having covered the city of Ahmedabad Wirelessly, Spidigo is rolling out Wireless Networks across India and strives to be the number one ISP in the country.

Abhishek Javeri, who is the MD of SNCL, is listed as Executive Vice-President at Spidigo and he is also listed as the MD of Strix Wireless. SNCL has acquired Strix Wireless and is in the process of Spidigo acquisition.

As per the above information, it seems that Strix and Spidigo are a result of continuation of the same technologies/projects as in SNCL’s subsidiary LNL in 2009.

Although the offerings by Spidigo in Ahmedabad seem to be unmatched in pricing, the reviews from customers of Spidigo are not good at all. My guess is that the company did not want to raise debts, and in lack of funds could not afford to provide good customer service. Now the company is using its funds from the chemical division for the networks foray.

Thanks for details about network branch. What kind of network it is? Broadband 4G home? How is the sustainability of this in future if big players are poring money like Jio, Airtel. This is probably intermediate service between Jio and customers, which leads to work with very thin margins.

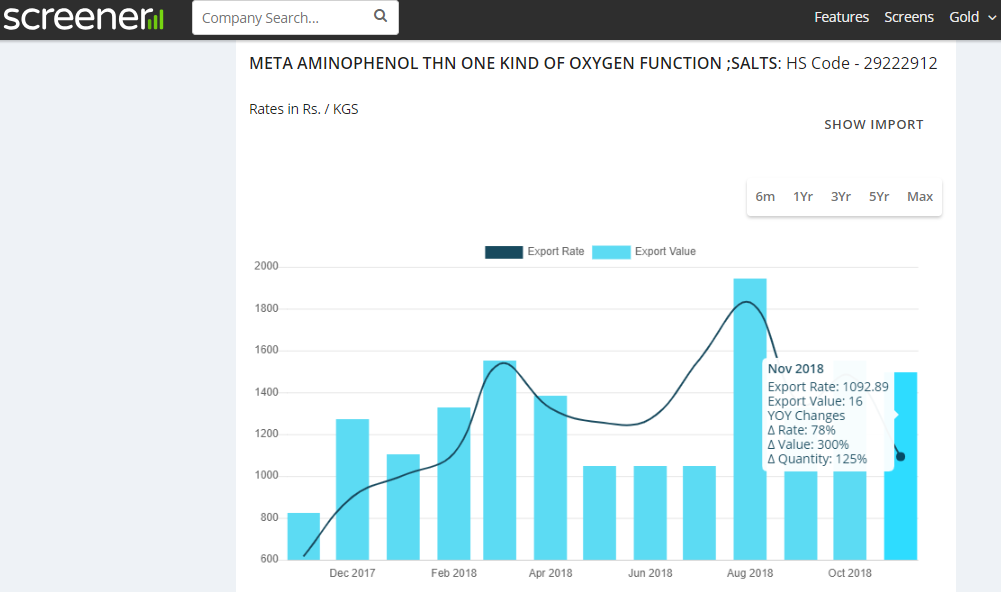

The company has benefited due to a sudden spurt in meta aminophenol price in international market. How is the price trend now?

Regards

Prasad

Prasad, I do not have answers to your questions. I did not understand the point about “intermediate service between Jio and customers”.

As per Spidigo’s website, the company is offering excellent rates, like Unlimited Data at 100 Mbps for Rs 1150 per month. This is comparable to the rates that are likely to be offered by Jio Gigafiber which is likely to be launched in 6 months.

Spidigo uses Wireless Mesh Networking technology. Each of the nodes act as routers in such a network. Failure rates would be lower due to built-in redundancy but error detection and correction would be more difficult. The tech has been used in rescue and military operations since there is no need of a traditional network. The tech is relevant to Internet of Things, e.g., network of autonomous cars. The tech has been talked about for many years now, but it seems commercialisation has become possible only recently. I am not an expert in this and would like to understand more about this technology, including the margins for the company.

There were apprehensions raised about the recent CRISIL “non-cooperation” rating of SNCL which have been put to rest via the recent company announcement. By the way, the same rating by CRISIL can be seen for many companies on Screener—I don’t think it is significant. Please correct me if wrong.

Thanks for explaining it Kalidasa. Hopefully we get more information on progress on this branch, revenue genaration will tell how profitable this business is.

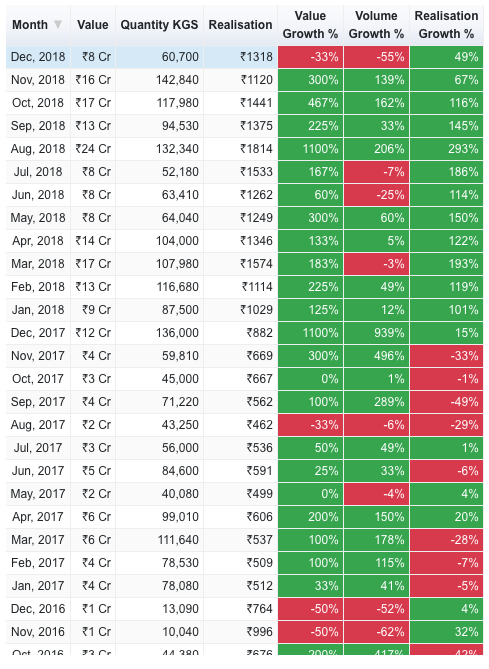

MAP prices seem stable but volumes are down and due to it the value as of the latest data

Phereak

Here is the latest investor presentation was given by the company today. It seems expansion is as per plan, happening through internal accruals. The expansion plan shows management is confident about product demand in future.

The process of manufacturing of MAP, OBD2 and ANDS will consumes probably 10-15000 TPA sulfuric acid. So this is the another product which they will try for backword integration. Sulfuric acid is not expensive but its handling and transportation cost adds up to net cost.

Here is another latest blog on printing dye shortage due to company closure in China.

The reopening of these plants are always risk for Sadhana, probably this is the reason for the recent correction

Prasad, your link about leuco dyes is not the latest but is more than a year old.

This home/office gadget uses thermal paper. Will such gadgets open up an entirely new and much bigger market for thermal papers? Will such gadgets lead to increased demand of ODB2?