S.R.Industries Ltd.manufacturing sports shoes for MNC.brands like PUMA,FILA,Umbro,Future group & many more reputed brand.current market cap is around 10 croe @ cmp of ₹.6.70/-. Total secure & unsecure debt around ₹ 40 crore.last year (2015-16) no major growth in top line & reported negative bottom line.but last three quarters performance of this year showing turn around.(possible).

I recently received response to my emailed questionnaire from management & it sound interesting.here is the copy paste of email response.

Dear Mr. Shinde,

Thank you for your email showing your interest in finding out more details about your company.

Please find detailed response to your questions below.

You may please call up or visit our website www.srfootwears.com for more information.

Best Regards

Amit Mahajan

On 17-03-2017 17:26, sanjay shinde wrote:

Dear promoter

This is Mr.sanjay shinde.I am a shareholder of S R Industries ltd.I recently browsed your website www.srfootwear.com. & also checked your annual report 2016 & conclude that your doing something interesting. I have few question as a shareholder please answer.

(1)Q) who is your customer?give revenue break up Answer - We are working with MNC clients such as Puma, Future Group and Fila. We are also in discussions with some more brands for tie-up.

(2)(Q) what is annual capacity ? Give break up (Answer)product wise Our Annual capacity is rated at over 3 Million pairs. The break-up product wise can be varied, depending on category wise demand.

(3) Debt figure?

A)We are enclosing the 31 December results which provide the Debt details.

(4) please provide export figure

a)Exports are currently low but are expected to rise in coming quarters

(5) operating profit margin & net profit margin?

(Answer) Existing profit margins are available from the quarterly results. However, these are expected to rise in coming quarters as debt levels fall, and topline rises.

(6) what is your topline & bottom line target for next ((year?

answer)We hope to achieve a topline of Rs. 65 Crores in next year, and net profit should be around Rs 5 Crores

(7) Number of employee? We have approximately 700 employees

(8) what about dividend to shareholders? We certainly hope to pay dividend to our shareholders. However, due to high levels of debt repayment, we do not foresee dividend payout in the next year.

(9) is it possible to turnaround this year? As per the results of 31st December, the company is in profit and we fully expect to remain in profit this year. We further expect a better performance in the coming quarters.

(10)Q. what about product quality you manufacturing?

Answer:- We are working with some of the most quality conscious brands and are supplying high quality products to them.

my knowledge of financial number analysis is very poor I request senior forum member please list your views on this company.

Sector perspective

India is the largest global producer of footwear after China, accounting to approx 13% of world footwear production, which is close to 16 billion pairs. This means that the average consumption globally is about 2-3 pairs/person. India produces approximate 2,000 Million pairs annually in different categories of Footwear. India exports about 115 million pairs, thus nearly 95% of its produce meets its own domestic demand.

With an estimated global population of 7-8 billion, India constitutes a share of approx 15%, which means 1.2 to 1.3 billion feet needs to be covered from heat, cold, injuries, protection etc. Footwear sector is a very significant segment of Leather and Non Leather products in India.

Size of Indian Domestic Footwear Industry is estimated to be worth 20-25,000 crores where leather and non-leather Footwear per capita consumption is estimated to be approx 1.1 pairs. In addition to this, Slippers (Hawai Chappals) segment is close to 10000 crores with per capita consumption are estimated to be 1 pair.

Our immediate Asian Neighbors reflect good per capita consumption between 3-4 pairs, whereas the developed nations such as US, EU, UK etc. enviably enjoy a far better per capita of 7 to 8 pairs.

The challenge for Indian Footwear Industry is lit large but anticipating India to become amongst top 5 Superpowers in 2030, our consumption rates can reach as high as 7-8 Pairs. In such a scenario, India would need to produce anywhere between 8-10 billion pairs consider yearly population growth.

Consolidating mid-term status by 2020, the potential target for Indian Footwear Industry will equalize consumption pattern of 3-4 pairs. With six/seven years to go, we need to scale our production from current level of 2 billion pairs to nearly 5 billion pairs at a CAGR rate of 30-40%.

Favorably for us, India ranks No.1 in milk production & we have the largest resource of cattle population in the world. Additionally, on the strength of raw material available domestically, the large pool of skilled and unskilled manpower, we have all the capability to take this challenge head on.

Given this backdrop of homogeneous potential it would not be an exaggeration to say that Footwear Sector is today, on engine of incremental growth. With global integration of Indian Industry, rapid change in lifestyle, income growth at bottom of the wealth pyramid, Footwear industry is expected to grow leaps and bounds

(source of above sector perspective is ETRetail)

Disclosure:- invested for long term.

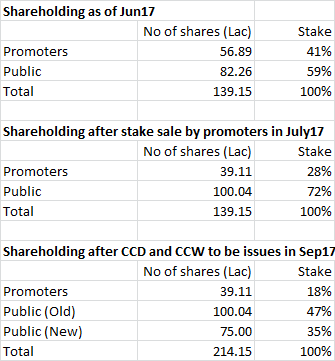

Shareholding as of Jun17

Shareholding as of Jun17