Hi All,

Please find the takeaways from S.H. Kelkar IPO meet,

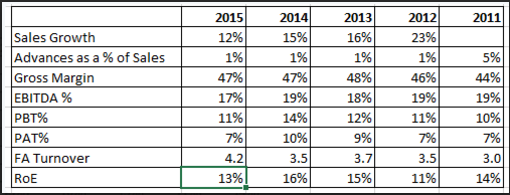

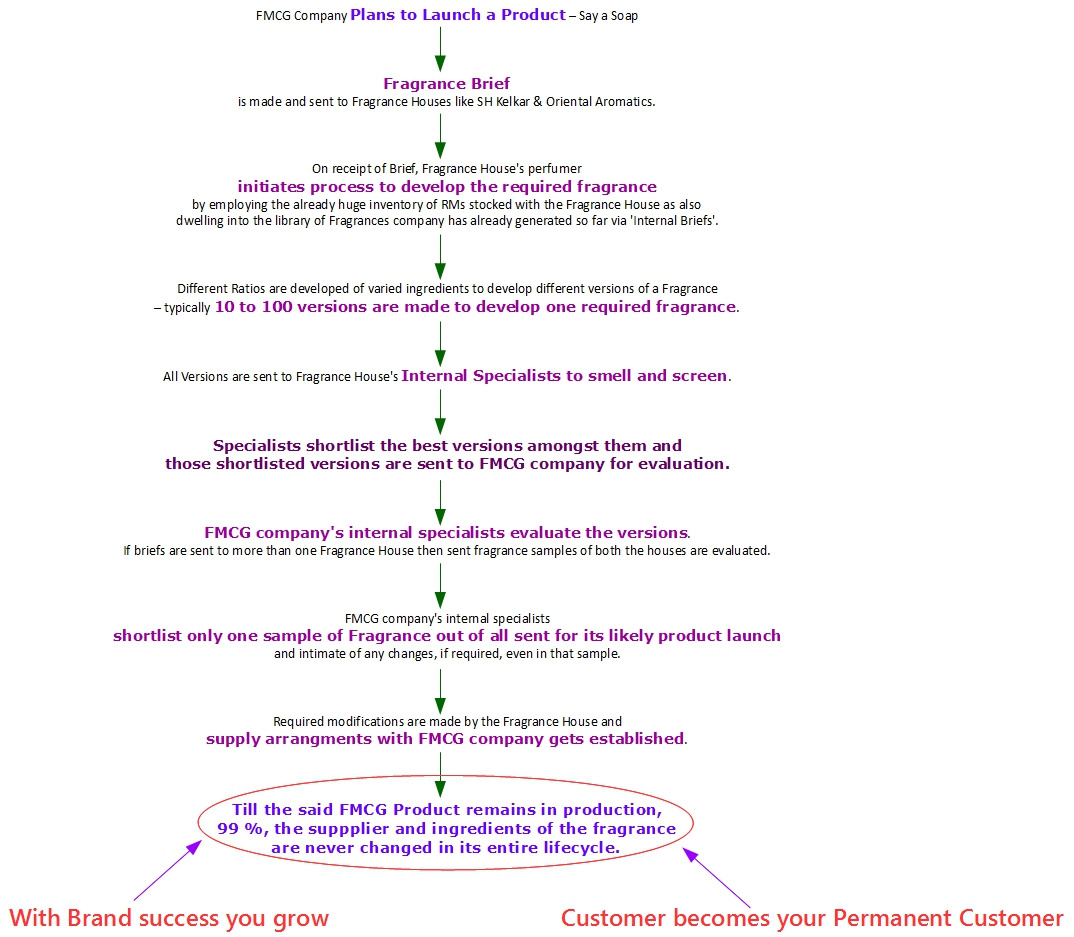

The co. has a longstanding reputation in the fragrances and flavours business,its application can be found in every 1 of 3 products that we consume or use. The co. deals with 95% of FMCG cos. in India covering Multinational,National,Regional and even Local cos. Fragrances is mainstay business and Flavours is roughly 1/8 of the total business currently. The business is very sticky in nature,the co. is a sole supplier to Cinthol since 1952 for example. The co. has a range of 9000 odd fragrances and 40000 odd prototypes. Fragrances involve a complex manufacturing process typically requiring 40-80 ingredients and a multi-step process with laser like precision to churn out one fragrance. The co. sources 1500 ingredients in total. Diverse use of ingredients and proprietary processes complemented by unique infrastructure give the co. an edge over competition and makes products impossible to replicate. The co. is very R&D focused and always looking to add new variety of fragrances to its range and for the same,it employs 12 perfumers who design and synthesise fragrances. Perfumers are master-crafters and a real asset to the co.,there are only 1000 odd perfumers in the world. The co. has also developed molecules which help in manufacturing multiple fragrance compounds and is in the process of filing patents for the same. The co. has 4000 odd customers out of which roughly 2000 are shops and distributors with 20000 touch-points. The co. also started retailing of fragrances in small packets which generate 7% of sales currently. 70% of revenues is from made-to-order for a customer and rest is from made-to-stock wherein someone could buy 2-3 fragrances,mix it up and develop a new fragrance an sell in the market. The growth in the past few years has been 16-17% out of which 10% approx. is coming from growth in existing FMCG products for which the co. is supplier,2%-3% from new FMCG products added and rest from price realisation going up. The co. expects to grow similarly going forward or slightly better going forward. The co. spent 200 cr in CAPEX to expand facilities and modernisation in last few years and would require only maintenance CAPEX going forward for a long time. Current capacity utilisation is 40% and current capacity can help treble sales from current level. Requirement of WC won’t be proportional to increase in sales going forward as certain level of raw-material is treated as fixed in nature and it can support even higher sales maintaining the current level. Fixed Asset turns will improve as capacity is utilised going forward. Reduction in WC and improving Fixed Asset turns would give a fillip to ROCE. The management seems decent and there’s a competent guys running the show,Mr. Kedar Vaze.

Link to RHP,

http://www.capitalmarket.com/pub/dp/dp23313.pdf