FY17: Corporate presentation

http://www.rpglifesciences.com/downloads/presentations/RPGLS_Corporate_Presentation_FY17.pdf

FY17 Annual Report:

http://www.rpglifesciences.com/downloads/annualreports/RPG_Life-Science_Ltd-AR_2016-17-for-WEB.PDF

FY17: Corporate presentation

http://www.rpglifesciences.com/downloads/presentations/RPGLS_Corporate_Presentation_FY17.pdf

FY17 Annual Report:

http://www.rpglifesciences.com/downloads/annualreports/RPG_Life-Science_Ltd-AR_2016-17-for-WEB.PDF

Company reported below average set of numbers in FY18Q1…

http://www.bseindia.com/xml-data/corpfiling/AttachLive/62bc237f-62ed-4252-9331-d3ecb76f6e70.pdf

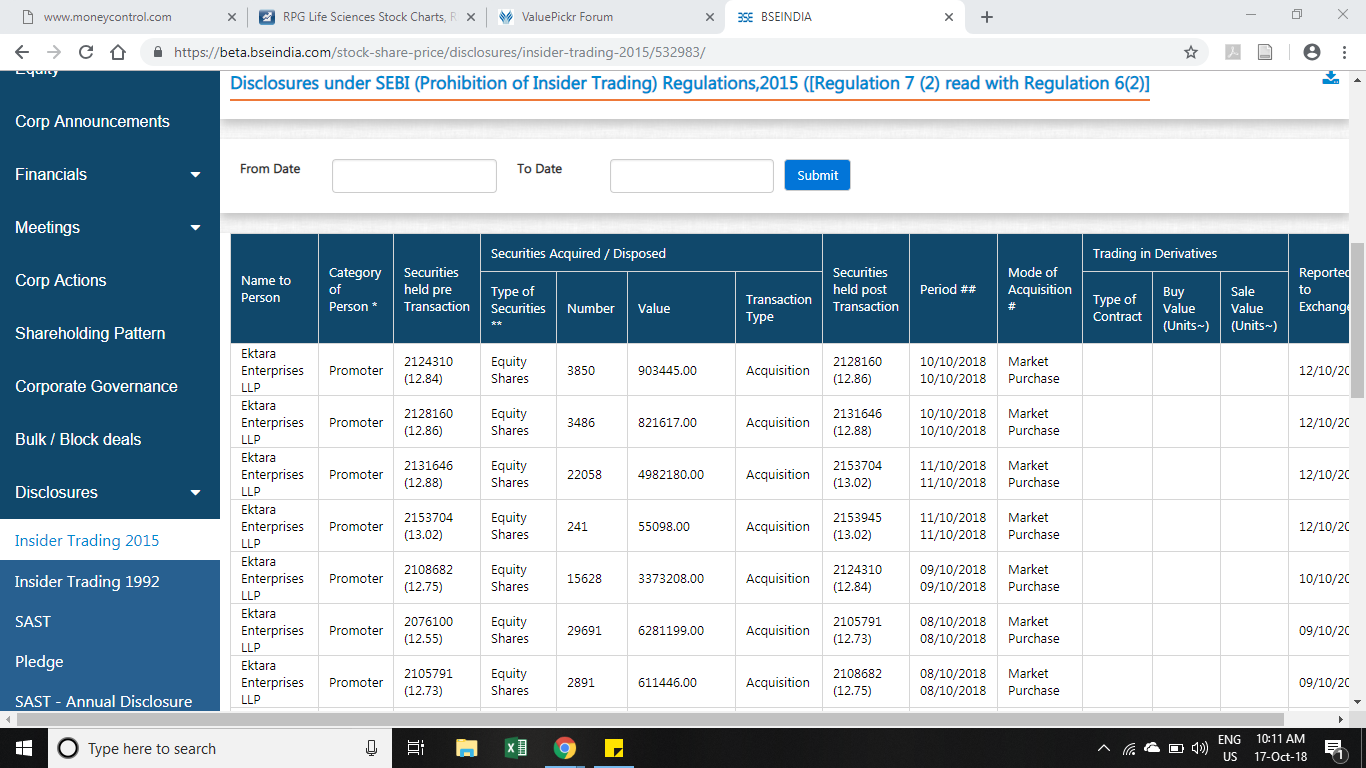

Something is going on the RPG Life . The promoters are continuing to raise their stake in last 2 years.even when price moved up from below 100 to above 300…Last purchase done on 12 Sept when price was 400+ .

I may be speculating here but not sure if they want to make this as their vehicle to healthcare sector for all future investments

Disclosure - invested from 150 level

Good results from RPG.

YoY Revenue up by 16% and PBT up by 76%. On QoQ basis, PBT increased from 47 Lakhs to 750 Lakhs!!!

other highlights from results announcement

Highest quarterly sales and highest quarterly operating margin in last 3 years (ref - screener). Also highest quarterly depreciation in last 3 years which means capacity addition started paying off! With kind of promoter buying seen in last 2 years, I guess this company is going to go places!

I do not get what is happening to this company.

The results are not bad, but still the stock has been beaten by nearly 40-45%.

Anyone has got any views on this company which rings some alarm bells?

what is the investment thesis here? I had a quick look at screener nos. EBITDA in early teens, ROE in single digit and PE is in 30s. What is the justification for this high valuation?

Its a bet on promoter stake increase! You may call it a gamble but sometime it works

Rest of RPG group companies like Ceat, Zensar Tech and KEC International have started doing quite well so there was hope that next in line would be RPG Life! Considering the fact that entire pharma industry is facing headwinds of pricing pressures and increased inspections, it may be a while when it will started showing result on consistent basis!

Promoter buying started again from 1st Oct onwards. see below

Around 70,000 shares purchased by promoters in this month.

Was just randomly checking the news on the stock…

came across this… RPG Life Sciences targets Rs 1,000-cr revenue in 5 yrs | Business Standard News

Looks like another example where the walking the talk didn’t fall in place.

The company seems to have changed their strategy recently betting on chronic drugs.

Led the company is being now led by Yugal Sikri, who has been a vetran in this field for almost 3 decades.

The company, being a part of the renowned RPG group, is available only at Rs.650 cr market share.

Worth a look at this stage.

Disc: Recently invested.

@Marathondreams Hey! I just started my research into the company and seems like its doing well based on management, their financial ratios, increasing operating margins. Profit seems to be increasing faster than sales, so operating leverage is playing out in the company. My guess is because the company was executing initiatives like digitization, cost cutting and paying off debt (until recently they paid out 24cr + in debt per year).

I do however have a few concerns.

Management has been changed a few times in the company, so there is no stability in leadership, vision and therefore execution of their growth strategy. This has obviously hampered the stock and resulted in volatile movements where it went all the way to 600+ and started its decline back to 145. Frequent churning of management also resulted in them not being able to stick to strategy and delayed their plans to enter US markets (as US FDA audit was pending)

Even though promoters are increasing their stake, its a very small part of their giant $3 Billion conglomerate. Risk of agency costs.

Management doesn’t walk the talk. It went to claim that they will have 1000+ cr in revenues in 5 years. This was in 2016, its been 5 years since and revenues have yet to cross half of that target. They are below 400 cr.

Their products haven’t been extraordinary and they don’t seem to be making efforts to get into higher margins or upcoming areas within pharma world. No mention of complex APIs. They do produce some niche APIs but that too for generic business. I think this is again due to a lack of targeted strategy on R&D and due to frequent churn in management at the top.

Since you have been following the company for a while, would like to know your thoughts on how they have evolved and where do you see them going? Are you still invested?

I sold off all my shares few years back, when I found out that they are more talk, less action. It felt like nothing was moving in this company. Not tracking it for past 2-3 years.

Thank you! That’s been my assessment as well.

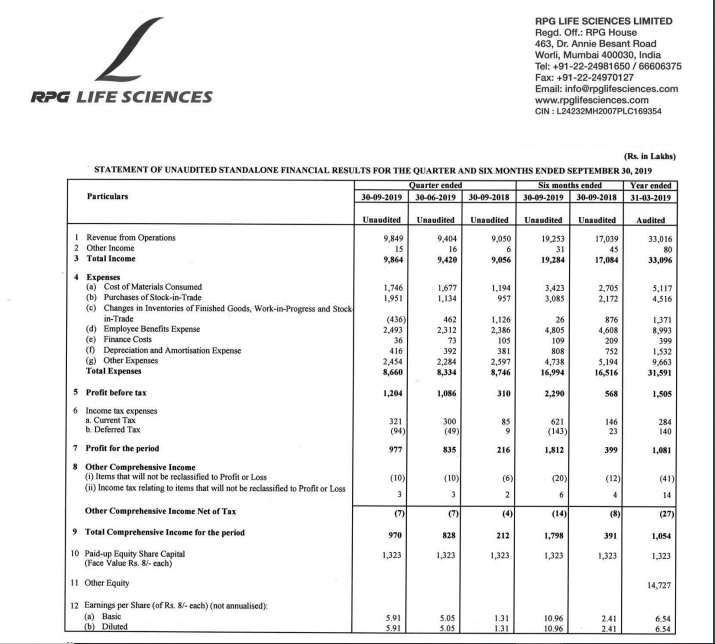

Descent set of results. Awaiting management commentary during the concall.

Disc: Invested. Biased.

This stock seems to have entered in radar of Aditya Khema of Incred Healthcare PMS and SOIC.

What prompted me to study this company was hint by Ishmohit.

All ratios have started improving, ranging from Pat(% of sales), EBITA (% of Sales), ROCE, ROE etc

The company seems to be focusing on branded Domestic market and emerging markets specially Myanmar.

It is market leader in immunosuppressant drug (92% market share)

Nephrology, oncology and Urology seem to their focus areas

Sharing the latest results of RPG.

YoY excellent performance but muted results on QoQ.

Any views?

regards,

dr.vikas

RPG Life sciences --Q4FY23–Earning Call Highlights —2nd May23 :

–Mkt is growing at single digits , the data says its at 7.9% with price growth leading the growth contributing about 5.1% , new introduction 2.3% & volume growth is tardy & flat. But we are growing higher --volume growth is 13% , the price growth is 5% and new introductions are 2% so put together the domestic formulation biz is registering a healthy 20% growth vs 7.9% growth of the mkt as reported by IPR.

–This yr has been a milestone for us , sales for the first time have crossed 500Cr+ , EBITDA 100Cr+,Cash in Hand 100Cr+, 1000Cr+ Mkt cap.

–first product in our portfolio Naprosyn+ becomes the first 50 Cr+ Brand Franchise

–for the 4th consecutive year we had YnY upward trajectory i.e sales has grown consistently more than the mkt for the last 4 yrs , all profitability metrics EBITDA / PBT / PAT all have registered YnY consistent uptrend superior growth , both PAT & PBT multiplied & grown 6 times in the last 4 yrs. Margins have grown consistently YnY

–EBITDA is 21% in FY23 , PBT from 4.4% in FY19 to 17.9% now. PAT is up from 3.2% to 13.2% now.

–Cash flow has also grown i.e from -14.5Cr in FY19 , we are 115.2 Cr this year . All of the above with a very strong hygiene which is an industry benchmark.

–Q4FY23 YnY revenue --14% growth

–EBITDA YnY --20%+

–PBT YnY --26%

–PAT YnY—38% and margins in all showing upward trend.

–We have 3 segments --domestic formulations / international formulations and API

–We have 67/68% coming from domestic, 17/18% coming from international formulations , & 15/16% coming from API.

–In Q4 --both formulations ( Domestic & International ) grew by 19% , API was sluggish due to order pattern by the customers and some inventory adjustments by one of our top cust. for one of our top products

–This is the best year for net working capital also i.e we had 48 days of net working capital which is 13% to our sales which is the best in the last 5/6 yrs.

–Ops highlights --new products launched in FY19 contribute 28% to our sales

–The New Product Denosumab Sales ~5 Cr in the very first year of Launch

–The New Rheumatology Franchise grows to contributing significantly to Specialty Sales

–Next 3 yrs domestic formulation outlook ? —Product portfolio rejuvenation is the first of the 5 pillars which we have identified as biz improvment. We have focussed on 3 subpillars (1) How to rejuvenate & maximise our legacy products as they contribute 67/70% of our turnover --so we have decided to have lifecycle mgmt strategy

so we have launched close to 9 line extensions for legacy products and they are growing much ahead of the mkt at 16/17% thanks to lifecycle mgmt

(2) focus on speciality biz --we have Nepro as dominant segment so strengthened it and as part of lifecycle mgmt for our immunosuppressant basket we have decided to branch out to Rheumatology which has usage of immuno suppressant products which were earlier being prescribed only in Nephrology & now we are also getting into Rheumatology & now we are foraying into dermatology & gastroenterology not in mass but in specialty side & the

( 3) is Chronic portfolio thrust.

–Chronic is not that big for now , this is the area we have to strengthen it . It contributes 11/12% --cardiovascular. Another chronic therapy which we are focusing on is urology which is contributing 2/3% to turn-over.

–Margins --Consistently improving since FY19 from 10% to 20% --outlook ahead ? – its a function of both components of the cost i.e COGS and Opex & our cost reduction story is structural i.e basic components of the cost which are contributing greater proportion have been addressed from fundamental standpoint. i.e Org. structure where we have addressed the roles , overlapping of roles , span of control & all this put together has helped us in good % point in the cost reduction.

2) Unrelenting focus on processes which has reduced our mfring cost thanks to lot of efforts.

–Drivers of further improvement in EBITDA Margin is going to be Product mix , scale of ops & those factors which will help us to keep this increasing. The input cost increase has come down to some extent but not to pre-covid levels & that is putting pressure on material cost.

–Aditya Khemka from Incred capital —Employee cost is higher than our run-rate i.e its about 35% growth YnY on our employee cost ,reasons ? --This is largely because of good performance which we had this year so incentives which we have planned for the mgmt is part of this provisions. Yearly the growth is 17% compared to 16.5% in revenue , we are growing now and talent requirement is increasing across the roles and attractive incentive plans. This going forward will be in line with the revenue growth which we see

–Also the International Formulations & API has shown some muted growth , why ? --International formulations is 13/14% growth which is not bad but in API the smallest segment of ours where the product basket is also limited , there we had some inventory correction so we are in touch with cust. and it will not be stretching to Q1 …this was one time correction in this Qtr & It will bring growth trajectory as we had in earlier years.

–Decided that International biz also becomes our growth driver in a step-wise manner for which are investing in the modernization of both plants & working on product pipeline for both international formulations and API Biz & there is a time period of 1.5/2 yrs but we see a good traction from this which might be higher than domestic formulations going forward.

–API was our 3rd priority but with modernizing our plant and product pipeline we expect API also to be a growth driver in 1.5/2yrs hence

–Any plant shutdown for this modernization initiative ? --Yes there would be some shutdown of some blocks but before that shutdown we will have some inventory buildup for the period of shutdown so it sales are not impacted. It will shut down for 3 to 3.5 months but it wont impact our turn-over.

–Capex for FY24 onwards — In the last 3 yrs including this year we had a capex of 100Cr+ in the 2 plants being spent ,this will be over by this FY24 and at the end of it capacity improvement of 40/50% in API & around 15/20% in Ankleshwar formulation plant & more importantly the regulatory approvals from pix and EU regulators should also happen.

–Sajal Kapoor Q --Appreciation for Mgmt for lot of improvement in the Biz on all front in the last 4 yrs since the time new MD joined & lot of initiatives on people side also which many pharma cos dont bother . QUESTION : API biz can be a growth driver after modernization & capacity expansion in this but what gives us the right to Win in this as huge competition in this segment where the core competence is API —We also had similar Qs but with the API situation changing in the country and that we have a API plant since decades now & the fact that we have the infra. i.e R&D , regulatory also in place , we can look at API differently than done earlier by us so therfore right to win will come from 2/3 sources : 1) our strong presence in immunosuppressant, we are one of the major suppliers of brand Azathioprine both on API side and Formulation side so we have a connect with the cust. with whom we are dealing for the past 15/20 yrs and we have good stickiness with them.

2)We have international formulation and domestic formulation products for which we can have backward integration for some of our products , that will help us to improve margins because today we are sharing them with others , tomm. we will not have to share

3) selection of API basket itself . We are not a large player who can compete with Divis etc but we can identify some of the niche APIs which have limited competition , limited DMS filed & we can work on those and connect with the innovators formulators then we have a biz case for us. these are 2 or 3 drivers which are forming the pillars of product portfolio strategy 2) we have a plant already and we have expertise in people in this and leverage it and this biz is more profitable to us so all that put together has helped us in crafting the API strategy & we have been careful in that crafting & deciding which products we will develop & we have been careful and the mkts where we should be entering .

–Gross Margins Q, Chemical prices have cooled YnY & there is price hike that should give us GM so if this is correct then majority of that should filter into the margin , correct ? –

Yes, if RM goes down it will be passed down impacting the margins & the fact is also that we have been waiting for these price reductions and expecting that these input cost will come down to pre-covid levels which barring couple of categories like aluminium foil , to some extent in solvent but in other places not seeing decrease , if that happens ,this should be visible in GM and you would notice that our GM has improved overtime in the last 5/6 yrs but in last few yrs they are stagnant . Input cost has gone up , the material cost has gone up however we have optimisation in mfring overhead so impact on the cost is not that much, its balancing out in a way.

–Some elaboration on the Pillar 2 & 3 in the 7 pillar slide i.e R&D and Innovation ? —On the R&D side we have R&D for the international Formulations and APIs to be exported , the international biz we have clearly defined strategy to focus on our strength of immunosuppressant basket , we are strong player in Azathioprine & now want to work on micofinoled (? need to check the spelling ) which is bigger in size than azathioprine so first focus in this basket , we want to every single strength and variant for these 4 molecules which is Azathioprine, Micofinoled,tetrolimus and ? , currently the work is on . No. of these variants are under development 2) we are focusing on the product which need special mfring conditions like low RH/Temp , low volumes which doesnt attract the attention of biggies and 3) some amount of complexity in the formulation & there are complex generic products etc are the 3rd category which we are focusing. 4) we have our own API plant and we have forward integration for those APIs and backward integration of formulations so some of the APIs in the tgt list are those APIs as well. This is on international formulation side.

–On API side we have clearly identified certain APIs , which are niche , size is sub 100Mn$ and where the DMS filed are less in no. because the vol. are low thats why we can get better margins so thats our focus on R&D pipeline.

–On Innovation side —we are an old co. 55 yr old co. not with a great track record of growth so basically the old processes, old systems , old formulations was the way earlier so what we have tried to do is involve every single HOD, we have 50+ HODs in various functions to identify what is new way of doing what they are currently doing & we had record innovation projects i.e over 130 odd projects which the teams worked out. All of this is helping people to think differently.

–No. of field force additions in the next Yr ? —We look at the tgt cust. coverage ,with the field force expansion which we took in the last 3 yrs i.e 10% each year we are able to cover all our tgt customers 85/90% except GPs we are also increased our coverage to 30% more than what we were covering , as we enter other therapies we will also add reps accordingly. This 8/10% field force expansion on an avg. per year.

– Scope of investments on the branded side ? --sales force additions will be in line and will make sure 85/90% of tgted customers. We will be thoughtful on the M&A and evaluating proposals.

–GM down sequentially? --Largely due to input cost & 2nd also is that product mix is imp. that also plays a role. Once inventory correction settles down, we will be back to normal.

–Pardon some spellings !

RPG Lifeciences Q4 concall highlights -

Business breakdown -

Domestic formulations - 67 pc

International formulations - 18 pc

APIs - 15 pc

Manufacturing facilities - 03 ( 02 Formulations + 01 APIs plant )

Leader in Immunosuppressants in India

Among companies with < 1000 cr sales, RPG Life is no 1 in terms of EBITDA margins, PBT and PAT margins

FY 19- FY 23 highlights -

Sales - 330 to 513 cr

EBITDA- up 3X

Profits- up 6X

Current cash balance of 100cr. Company scouting to acquire brands. No debt on balance sheet

Q4 outcome-

Sales at 118 vs 103 cr, up 14 pc

EBITDA at 18 vs 15 cr, up 20 pc

PAT at 10.5 vs 7.5 cr, up 38 pc

FY23 outcome-

Sales at 512 vs 440 cr, up 17 pc

EBITDA at 107 vs 90 cr, up 19 pc

PAT at 68 vs 51 cr, up 32 pc

Sales breakdown-

Domestic formulation- 337 cr, up 20%

International Formulations-92cr, up 18 pc ( present in UK,Germany, France, Canada, Australia, Africa )

APIs-80 vs 78 cr

Monthly MR productivity now at 5.5 vs 3.5 lakhs in FY 19

Important management comments-

IPM volume growth continues to be flattish, RPG volumes grew 13 pc

Total IPM growth ( Price + Volume + new products ) at 8 pc vs RPG’s total growth of 20 pc ( v v healthy )

New products launched post FY 19 at 28 pc of company sales ( a big achievement )

Rheumatology sales picking up nicely ( launched 2 yrs back )

Intend to spend 100cr towards plant modernisation and capacity enhancement

Also looking to acquire brands in local Mkts

Product mix and scale of operations may help sustain upwards trajectory of EBITDA margins

Q4 is always a seasonally weak qtr due nature of ordering patterns by clients. Qtrly Sales run rate should rebound from Q1 onwards

Company is strong in Immunosuppressant APIs which gives the company the right to win here

Company wants to develop niche, small mkt size APIs

Don’t intend to go head on against large players like DIVIS on any of the APIs

Intend to increase field force by 8-10 pc / year

Next two focus therapies - derma, GI - because immunosuppressants are used in these therapies as well. So the expansion should be easier

Post the fall in stock price in last 2-3 days, looks good to me. Added today. Tracking position

Excellent results by RPG.

Attaching the results and the Investor Presentation below

https://www.bseindia.com/xml-data/corpfiling/AttachLive/55744826-2434-49b7-91fd-a6bb060bb964.pdf

Invested since 600-700 levels and BIASED

RPG Lifesciences—Q2FY24—Earning call Highlights—19th Oct23 :

–For the 5th consecutive year , we have an upward trajectory of growth

Revenue : 154Cr --Growth of 14% YnY & 4.1% QnQ

EBITDA : 39.1Cr–growth of 26% YnY

EBITDA Margin : 25.5% vs 23% inQ2FY23

PAT : 25.9Cr --Growth of 30% YnY

PAT Margin : 16.8% —vs 14.8% in Q2FY23

–In Domestic Formulations we had 16% growth vs mkt growth of 8%

–Biz segment break-up :Domestic Formulations contributed 66% to total sales of H1 FY24

–International Formulations contributed 19% to total sales of H1 FY2–with 15% growth in H1FY24 Vs H1FY23 i.e 56.3Cr

–API contributed 15% to total sales of H1 FY24–with 7% growth in H1FY24 vs H1FY23 i.e 46.1Cr

–Modernization and Capacity expansion plan at Ankleshwar Plant will be completed by end of FY24 --so that we can make it ready for International Regulatory inspections

–Legacy Product Naprosyn becomes the first 50 Cr+ Brand of the Company

–Strengthening Presence in Rheumatology , Oncology & Augmented Product Basket in Cardiology , Diabetology , Urology

–New product contribution in FY23 is 28% which was 6% in FY19

–In Domestic Formulations : we had a volume growth of 8% & price growth of 5%+ and rest is new product contribution

–Gross Margin improvement from 66% run rate to 71% ,why ? —We had consistent profitability frame-work created & its applicable to both COGS and Opex i.e

In COGS we have worked on product re-engineering , 13 SKUs reformulated which has helped us to improve our margins & we are working on other efficiencies , optimised people at plants, these structural interventions have helped us to improve our margins

–In this Qtr we had some product mix advantage in domestic formulations , international formulations and APIs --this has also contributed to Margin improvement in this Qtr

–We are renegotiating the prices with RM vendors and also we have alternate vendor development programs which is helping us to reduce RM price but it will keep fluctuating as per Macro situation

–Capex : 60Cr in FY24 --for both plant modernisation and capacity expansion for Ankleshwar ( formulations ) & Navi Mumbai ( API) Plants

–Evaluating candidates for Acquisitions both in formulations and API side.

—Strong presence in immunosuppressant segment (Azathioprine) in all the 3 verticals for Domestic , International & APIs .

–Our portfolio is divided into 2 : Mass biz & Speciality biz with Mass biz —our product portfolio is consulting Physicans and GPs & that is our strong forte , in the Speciality side --we were strong on Neprology & built up Rheumatology in the last 3 yrs and its contributing 14% to our Speciality turn-over

Then we are also moving into Gastro entrology & dermatology which are in speciality side. On the mass side we are also working in Diabetology & Cardiology along with CPs and GPs & in all of these segments our intent is to have a coverage of 85% of the universe & we have reached we have maturity except in consulting Physicians which is a large segment where we have reached almost 70/80% of the coverage

–Another segement where we are looking at is Orthopedics due to our great performance of Naprosyn

–Mass vs Speciality the Margin Split is similar as in our legacy biz in Mass is also good margins along with Speciality

–In international biz --our R&D pipeline is centring around 3 to 4 areas , one if them is immunosuppressant segment—there are gaps in line extensions and we are developing molecules here . In category 2 we have complex generic products & we have launched one such product as sodium xyz …version

3rd category is those products which require complex mfring i.e those products which need low temp. , 4th category where we have limited competition & these are the 3 to 4 niches where we will be profitable.

–Currently we have close to about 30% formulations being outsourced & in the domestic formulation the new products are outsourced from reputed CDMOs which are well evolved group in the Country and once we launch a product and it gains tractions , then we take a decision to bring it in-house to add some GP% bps due to it.

–In Domestic formulations the smart strategy is to outsource the formulations as CDMOs are quite evolved in this country and they add to efficiency and speed , unless the product is developed due to our R&D , then we will see that mkt gets mfered by us

—In R&D we are focussing on export oriented products & in APIs we are focussing on APIs which would be exported . The domestic formulation R&D is outsourced by us

PS : Some points in the end I may have missed , please refer to transcripts for it when its released .