Clarification from Company on certain information being circulated in social media regarding

“Promoters of Company taking large interest free loan from the Company”.

Await analysis of Welspun Enterprises.

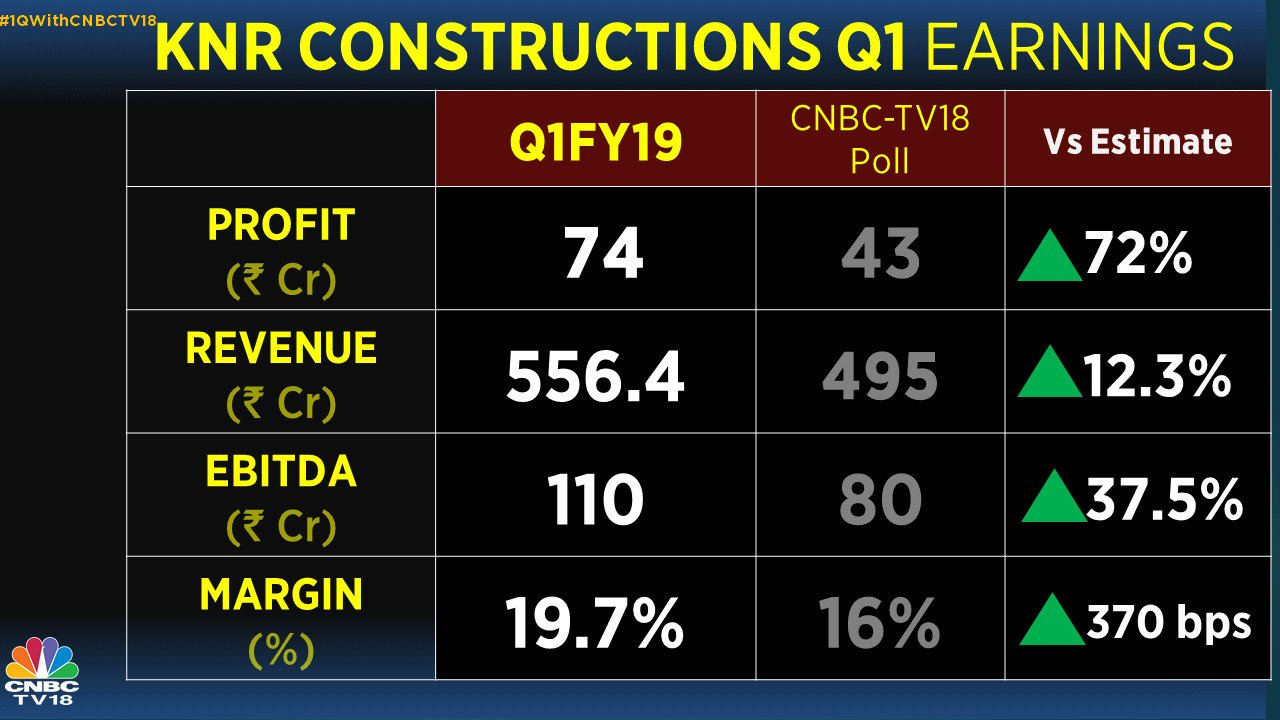

Very good analysis from Dr Vijay Malik on KNR. Gives an insight on what all things one should look at while analyzing Infra players. Must read …

5 Likes

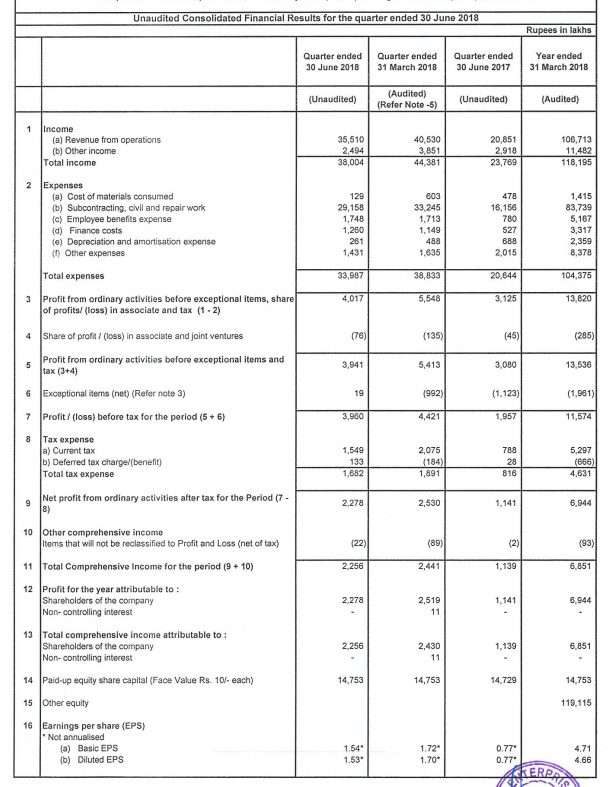

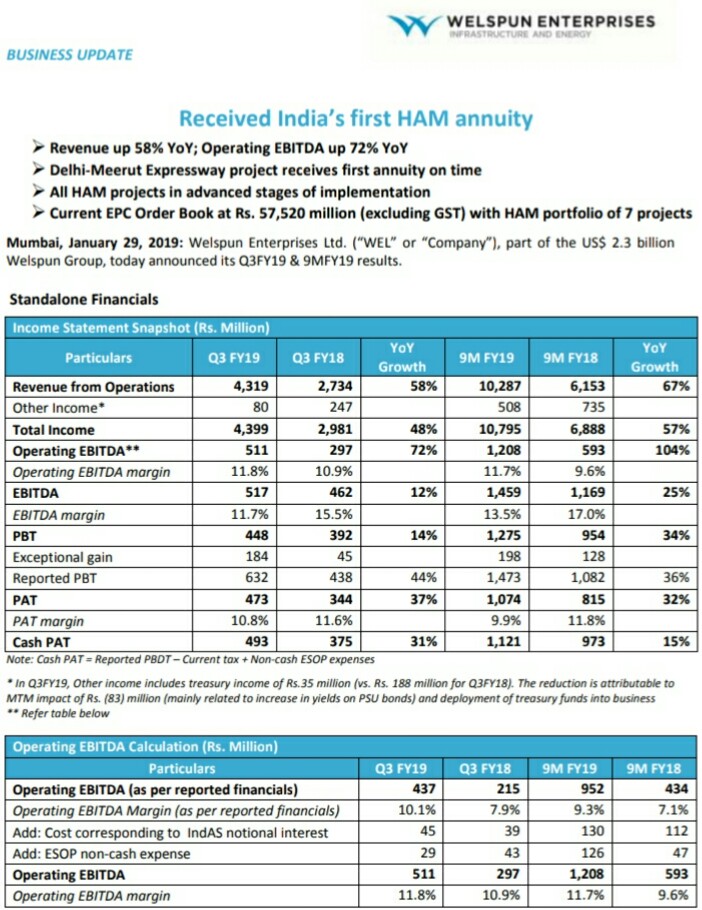

Quarterly results for Welspun Enterprise. Good YoY growth shown.

Here is the result and a brief Investor PPT PDF

https://www.bseindia.com/xml-data/corpfiling/AttachLive/8bee2691-b6e5-4b36-abc4-f6a2585b261d.pdf

Good cash in balance sheet which would enable them to bid for more HAM projects. Company is confident of excellent growth for next two years. Couple of months back Promoters buying was also there in this counter.

EDIT : As of now cash per share comes around ~ 47 Rs. We are getting remaining business at 108 Rs based on today’s closing price.

Disc : Invested recently

3 Likes

Guys, you must read AR-FY18 of Welspun Enterprise

http://www.welspunenterprises.com/userfiles/file/WEL%20AR%202018%20web.pdf

- Gives good understanding of their own business

- Outlook on overall Infra growth in country

- Really detailed cash flow statement

There are a lot of related party transactions, which I dont understand much. If someone can help on that if everything looks ok, it will be great.

Its worth spending your time. Eagerly waiting for ARs of other good companies in this sector.

Disc : Invested in Welspun Enterprise

1 Like

Results have been strong by almost all the listed road companies but price of all the road companies have taken a beating and substantially lower than all time highs. Price movement has not been encouraging since past 3 months.

There was a news item that NHAI is nearing its drawing limits. Until further sources are tied up, disbursal to Road construction players will be hampered. Input costs (cement , steel and others) are steadily going up which will curtail the profitability figure of the players. May be this is hurting the sentiments.

1 Like

i think the risk here is political.What happens to these orders If BJP doesnt come back to power.Invested in Welspun enterprises and Dilip Buildcon

Agree…and does not look like that Risk is going away soon. Reduced my position to the sector over last few weeks.

Weslpun Enterprise

Highlights of Q1 FY 19 results

Key Highlights

- Current portfolio of hybrid annuity model projects consisting of six projects is amounting to about Rs.7000 Cr

- The current order book stands at about Rs.5600 Cr, which includes escalation and change of scopes

- Completed the Delhi-Meerut package one in a record time of 19 months as against the scheduled time available of 30 months and eligible for bonus of 11 month and this was the first company to complete a project of hybrid annuity model within the country in a record time.

- Company have been able to achieve appointed date for two of the projects, which are namely GagalheriSaharanpur-Yamunanagar (GSY) and Chutmalpur-Ganeshpur and RoorkeeChutmalpur-Gagalheri (CGRG).

- The appointed date for GSY project was on January 26, 2018 and by the end of June 2018 and company have achieved more than 20% of the physical progress, so the project is progressing well. The first milestone of the 20% payment milestone was achieved 71 days in advance of the contractual schedule and expect to improve further post the monsoon completion .

- In CGRG project the project achieved its appointed date on February 28, 2018 and achieved 15% physical progress at the end of June 2018 well ahead of the contractual schedule.

- There are two other projects which company have in the order book

o One is Aunta-Samaria. This project is primarily a bridge project with about eight kilometers of road in which company have achieved financial closure and awaiting for the appointed date. Appointed date is expected to come in Q2FY19. Company has already finalised all major subcontracts for road as well as for the bridge and company is fully mobilised at site and company has started the development work at the site . Company expect to give a push to this project after the appointed date is achieved within this quarter.

o Second is a hybrid annuity model project that company have in Chikhali-Tarsod in Maharashtra. Company has completed the acquisition of the stake of 49% from Vishvaraj Group in January 2018. Company have also obtained the financial closure for the project and expect the appointed date for the project to take place in Q2 of FY2019 and company expect it to take place in middle of August 18. The EPC contract, the subcontractors have been finalized and the site is mobilized and the developmental work has been started. Company also awarded the single largest project of the Company Sattanathapuram-Nagapattinam in Tamil Nadu on July 5, 2018. - At the HAM level company did bid at Rs 2004 Cr and company is currently awaiting for its signing of the concession agreement, which should take place by the middle of August 2018 and this project should start operating on the ground level in Q4 of 2018. That is as far as the road hybrid annuity model is concerned.

- In Infra space , company is working on a significant project that is Dewas Water. Company have received the appointed date for the Dewas water project on Mat 07,2018 and company has started the execution. At the end of June 2018, the progress was somewhere around 10% on this particular project

- Out of the whole set of projects that company have both in hybrid annuity and the Dewas Water other than the project, which the LOA was issued on July 5, 2018 are financially closed as well as the EPC contracts finalized with the subcontractors and hence the clear visibility established for the completion of the projects.

Oil & Gas Business Highlights - There are five blocks in totality, which are two in Kutch, one in Mumbai, one in Palej, which is on hold and one is DSF block offshore close to the Mumbai block. Other than the Mumbai block all blocks are under appraisal program. The two Kutch blocks, currently a deeper section is being drilled in one of the blocks and company expect the result to be out by Oct 2018 of the current appraisal program of Kutch one and Kutch two blocks. In terms of the block in Mumbai, which is MB-OSN-2005/2 company owns 100 %. In Kutch block the operator is ONGC and in the Kutch block company is holding a PI of 25 % participating interest is 25% and on the Kutch block two participating interest is 30%. In Mumbai Block company participating interest is 100 %. And company is awaiting for government approval to enter into phase two of the exploration program.

- In terms of the latest block that company acquired in B-9 which is adjoining block to the Mumbai block it is a discovered field and hence it straightaway will go for a field development. Company expecting the field development to proceed as per plan and the first gas to be out in the year 2021-2022.

- The main stay of the Company is right now the hybrid annuity road projects and currently focusing more on national highway. The current order book outlook is that there are about 40 HAM projects announced by NHAI, which should be bidded out in this quarter and the next quarter totaling to about Rs.40,000 Cr. Company plan to bid very selectively in the these projects amounting to may be about Rs.30,000 Cr and company expect to win bid to be in the same ratio as it was in the past so as far as the outlook is concerned the business has a substantial order book and has a clear visibility for the turnover for the next two years.

- The pipeline of the order is strong and we should have wins much more going forward and the business is in a situation where the outcomes can be reasonably well established ahead of time.

Financial Highlights - Revenue grew by 73% to Rs.347 Cr from Rs.200 Cr last year same quarter.

- EBITDA grew by 25 % to 46.3 Cr from 36.9 Cr last year same quarter. Out of this reported EBITDA of 46.3 Cr in this quarter, operating EBITDA is 37.6 Cr, which is 120% higher than what was there last year same quarter

- PAT grew by 28 % to 27 Cr compare to last year same quarter

- Cash PAT grew by 14 % to 32.3 Cr compare to last year same quarter

Standalone Basis

o Net worth has increased from Rs. 1,457 Cr as on March 31, 2018 to Rs. 1489 Cr as on June 30, 2018

o The gross debt has also come down from Rs. 66.4 Cr to Rs. 50.6 Cr

o The cash and cash equivalents for the quarter ending June is Rs. 487 Cr plus there is Rs. 219 Cr of the temporary funding that company have done to the subsidiary which otherwise company could have drawn by way of a debt at the subsidiary level and this money could have been repatriated back at the parental level, so this in a way, is free cash available to company on demand, as and when company want. This has been done to minimize the interest cost at the SPV level and in turn make treasury operations more effective , so adding up both cash and cash equivalent total 706 Cr is available for deployement.

o Long term liability stands at 51.1 Cr compare to 30.3 Cr as on June 30,2018. The net current asset which was additional receivable for the additional funds deployed in the SPV or subsidiary have gone up from Rs.105 Cr to Rs.277 Cr, which can be easily brought down by Rs.219 Cr as and as an when company want and the other long term investment have gone up from Rs.726 Cr to Rs.800 Cr,

o Company have two adjustments in the operating income One is purely Ind-AS calculation, which is Rs.4.22 Cr, which was there in the other income, which is notional under Ind-AS and there has been a corresponding cost of the same amount Rs.4.22 Cr, which is in other expense. Since both of them are notional for the purpose of operating EBITDA, it has been excluded and also there is an another adjustment of a noncash item of Rs.4.82 Cr, which is there on account of ESOP so after taking both these numbers and adding back to in the EBITDA the operating EBITDA stands at Rs.37.6 Cr, which is 10.8% at the Company level. Now company all projects are not yet started , company mentioned that t in two of the projects company is waiting for the appointed date which will happen in Q2 and the other project is also likely to start construction in Q4, so thereby the operational operating EBITDA, which is 10.8% is certainly likely to go up significantly.

o There is another thing that company do on the SPV side to have enough liquidity on the SPV side. Company have cash reserves being created at the SPV level, which is also available as an operating income. so as and when the cash position in these companies are comfortable they can also be taken an operating income, so in a way at a company level company have visibility of 12% to 15% at operating EBITDA level.

Q&A

- What is the bid size of the Dewas Water project in Cr ?

o The total project as an EPC/new project is about Rs.70 Cr. There is an old project, which is getting transferred along with it, so the total project cost in terms of the value that it will be about Rs.145 Cr in totality. - Kindly provide the completion date for the GSY project and the CGRG project?

o The projects are scheduled for 24 months, as far as the projects are concerned they should be completed as per the concession agreement by January 25, 2020 is the GSY and the CGRG is February 27, 2020 those are the scheduled completion, but company is way ahead of the targeted schedule. - What was the early bonus amount company get for Delhi-Meerut expressway ?

o It should be closed to Rs.28 Cr in totality out of which 50% will be shared with the subcontractor - What could be the EBITDA margin for the whole year ?

o Range of 12 % - What will be the operational margin if company add the two projects which is not running currently ?

o It will go to 10.8 % - What is the company vision for the Gas and Oil segment in next four years and what kind of investment company is planning to do even company have strong cash and cash equivalent, any strong CAPEX plan going ahead apart from the current that company have made in blocks and when can the revenues be expected ?

o Commitment to this space is 175-200 Cr not beyond that going forward. In terms of strategy company don’t see in a foreseeable future that company will be associated with this line for a very long time , company want to monetise these assets as and when the appraisal programs are over and the results can be settled back.

o The first revenue can be in FY2020 from the B-9 block in the far end of FY2020 - Any management thought is there to reward in the form of buyback in the near term ?

o Company hybrid annuity model of road project is doing exceptionally well, company is sitting at an order book of about Rs.5600 Cr and like the orders of inflow of about Rs.5000 Cr which gives company an equity investment opportunity of almost like Rs.1000 Cr going forward and the use of the money is available for company so company will not think on it. - Did company had recorded any of the bonus from Delhi-Meerut Project ?

o The Delhi-Meerut project bonus has already been accounted for because the project has already achieved the PCOD and it was accounted in last year only nothing has come in current quarter. - What would be the site level margins for company for the projects that company is currently executing ?

o The site level margins are in the ranges of around 15% to 18% on the projects that company is currently executing. - Is it fair to say that the differential between the site level margin and the operating margin of 10.8% is a fixed cost of the overheads of the head office and everything and hence the margins will improve to 12% just because the scale doubles up?

o Yes As the apportionment of the overheads goes on to a larger base, the EBITDA margins will show upside trend. - How is the competitive environment is it a little bit higher or is it reasonable?

o In terms of competitive environment the weaker balance sheet players are finding it difficult to do the financial closures of the existing projects, hence the competitive environment should ease off rather than become more intense and nonetheless company is a very clearly disciplined bidder. Company will not lower its profit margin expectation just to win a project. Company believe that there is enough work in the market and company is currently focusing on NHAI there state highways, there is enough work in the space, which will allow company to get the returns as expected and company is not going to compromise under any circumstances. - What sort of order inflow company is targeting ?

o Company already have Rs.2000 Cr of an order this time as the project and expect additional Rs.5000 Cr approximately to come - There are so much report that public sector banks are not really going ahead with the guarantees that are required, so how robust is the acquisition slate with regard to the projects that are already awarded ? The incentive which was recorded that does not get accounted into the standalone entity is the understanding right ?

o Two things, as far as the challenge of bank guarantees and the challenge of financial closures are concerned, all the project which is in hand of company have submitted the requisite bank guarantees and are financially closed other than the project that won on June 5,2018 in which company believe that company will do financial closure well ahead of time that is given. Company don’t see same challenges as other are seeing because of the historical reasons or weaker balance sheet. Company is also disciplined to not take substantial orders when company financial closure on the on-going or in hand projects has not been done, so that discipline has been maintained in the Company, so company is not very much concerned d about the nationalized banks not issuing the bank guarantees that challenge has not been hitting company as of now. - What is the kind of IRR range that and does company see it coming down with more and more players competitively bidding under the HAM model?

o Company target IRR in the mid teens range around 15 % or there around depending on target location, duration, etc. As far as the competitive environment is concerned company do not see it to be very intense because the realisation donning upon the financial closure challenges, a lot of players are interested in doing the financial closure before going into the bid market once again. So the competitive environment from the bid side would ease off going forward - When does company see to monetize the Delhi-Meerut expressway project ?

o The way the NHAI guidelines works is 100% sale is possible after the two years of COD and 49% is possible even today much before the COD during construction itself, so company is evaluating various options in terms of the monetization, but not greater than two years that this monetization will happen and one more thing after the project completed it becomes like NHAI risk and accordingly company got the provisional rating done for Delhi-Meerut, which has achieved PCOD and after the PCOD done and NHAI credit phase managed to get AAA(SO) rating for Delhi-Meerut, so the cost of financing or even top-up debt and other things becomes far more easier, which can meet any cash flow requirement, so to that extent even if the monetization really takes place full after two years, a good amount of equity can be returned by way of top-up debt based on AAA (SO) rating that company achieved in Delhi-Meerut and similar things will happen in other projects as well ? - Any concern from government for delay of the payment ?

o No in fact payment is received ahead of time so NHAI as long as the contractor is performing the NHAI is willing to pay and support the completion of the project so company don’t see any concern on delaying of project . - In Delhi - Meerut there was also some repairs in the project so who is ultimately responsible for the repair works?

o The issue was the project was completed and another agency managing utility decided to replace the pipes in the region, which the approval had been taken by the agency from NHAI way before the project was supposed to be completed. Than they went ahead and dug up the side of the roads, since it was a period of monsoon water accumulation started, which resulted in some damages to the roads. The issue is that it was because of an uncoordinated effort by another governmental agency, a work they were supposed to do before the completion of the project they just chose to do after the completion of the project and those repairs are being carried out The project is under defect liability period of the EPC contractor or the subcontractors to repair everything up to 24 months post the completion, so in terms of SPV and in terms of Welspun Enterprises company is protected and company make sure that all issues will get solve before the defect liability period is over and it is at cost of contractor executing the work. So other agencies who are in urban infrastructure space need to deliver they need to do certain things alongside the project they need to do before the project gets completed or else they could lead to certain challenges on the assets that are being built up - On defect liability side , Is there some amount t held by form of some retention for the subcontractors?

o Yes substantial amounts are retained as the defect liability period until. As soon as the defect liability period is not over the money is not released - Did the Bonus was accounted for the first quarter ?

o No, it was accounted in the March 2018 results and it is not part of the Q1 results. - So last year company had of Rs.44 Cr of segment EBIT and infrastructure that included Rs.14 Cr of the bonus number?

o Yes - What is the total equity deployment company is looking for the year in HAM project ?

o Around 867 Cr and these are various projects that company has gone so far and company have deployed almost Rs.440 Cr so there is an additional requirement of almost Rs.428 Cr to be deployed from here on. Based on the construction schedule that company have shared company expect further 300 Cr would be invested during this year and balance 120 Cr in next year. - What is Oil & Gas investment in this year plan so far?

o Company have planned for around Rs.110 Cr of total investment in this year out of which nearly Rs.15 Cr is already invested in Q1, so there might be a balanced requirement of Rs.95 Cr in the balance nine months of this year. - Does company will carry with the overhead cost with normal inflation ?

o Rs.14 Cr run rate for a quarter is what are normal overheads would be and this is what company will expect with normal inflation to continue going forward. - What is the consolidated debt number for the Q1with SPV?

o 50.6 Cr and SPV is 376 Cr - Does company HAM sector is facing some sort of headwinds with delayed closures and financial closures due to public sector banks so does secondary sale route going in from the crisis project to lucrative return for company? Whether company is looking to acquire any projects ? Why did the Aunta-Simaria project won got delayed ?

o On Financial closure , company is working on 5 projects that are currently being pursued by the Company four of them have already achieved financial closure and significant amount of work has been done in each one of them, Delhi-Meerut is of course completed project, the rest three are all in advanced stage financial closure and everything has been done. Another four projects are there in that zone and in that every project company have achieved financial closure for stipulated time of 45 days to 60 days at most including the documentation so company has not faced any challenge. As far as the large project is concerned which is Tamil Nadu project, which has recently been won, company have got LOI only around 10 days back and company is very hopeful that the base of discussion that company is having with the lenders today. This should also see the financial closure within next 45 to 60 days. So as far as Welspun projects are concerned, there are sort of well bidded projects and company have not seen any issue in terms of the financial closure.

o Yes the company strategy has been both build as well as buy strategy and in that sense wherever the projects are good and it meets company own threshold , IRR returns and everything. Company is very confident of achieving financial closure if that is the only impeding factor for those projects to see light of the day and to that extent six projects that the Company has is mix of f three directly one and three being acquired through secondary route

o In Aunta-Simaria project company has won at a long time back and company did financial closure substantially well in time. e. The challenge is not about anything else, but the client being able to make their own CP, which one of them includes 80% of the land being available. company have taken a view until and unless company see the project being closed once done with the work of the land that company is available and the project closure cannot take place officially on the contract. Company do not want to plough in money and take an appointed date, Hence company have resisted the temptation to start the work and take the appointed date. However NHAI has now come into a position that they can give the appointed date. they are willing to appoint the IIT as the independent engineer for that project. They are willing to take a position on the land although for Aunta-Simaria land is not such a critical issue because it is only 8 kilometer four lane road, the bridge is what is taking the most of the time so company is deciding when to take the appointed date and when not to take because that could put up the business at a risk that company can deploy the funds and cannot get the completion certificates from the NHAI. So that discipline is part of company culture and this is a part of processes. So company will see such delays in case NHAI is not in a position to meet the CP. - Did the assembling block now removed for the Aunta-Simaria project or it is still there?

o It is removed . NHAI has taken a view that they will appoint one of the IITs as independent engineer because independent engineer is a necessity for company to proceed the job. - Did company has finalised any subcontractor in Tamil Nadu project?

o No company will finalized in next 60 days. - There was an article published in Business Standard, which said that Welspun Enterprises to look at 250 billion business in the next two years, currently company have around 70 billion order book, so does company plan to take it triple in the next two years, is it doable?

o Yes on the way now company have 5600 Cr of order book. and the way it was at the HAM level and which is Rs.7000 Cr is company current portfolio. Company expect an additional 5000 Cr in current year. So this is portfolio level issue which will take it to 12,000 Cr . and the year thereafter company expect order book growth and taking about Rs.8000 Cr in the order book for road and about Rs.4000 Cr for the water business, So company will be close to the numbers seen in business standard . - Is the 250 billion order book is cumulative right now at the end of the FY2020 ?

o Yes that us cumulative - what will be the impact of the interest rates on the HAM FCs and the FCs, which are being done as of now that is through the private banks or any other NBFCs and they are happening at what rate?

o Company have a combination of both private and nationalised banks participating including the NBFCs in all company projects and to that extent company cost average i of borrowing is in the range of around 9.5% for the 17-year loan period, now of course when the project gets commissioned and gets re-rated as AAA (SO) so the cost will come down based on that time prevailing market price, so you can see that most of our projects have been achieved, financing has been achieved near to the lowest possible financing rate and even the new project that company has won in Tamil-Nadu despite the interstate movement by almost 1% during the last six months we are pretty hopeful that company would be would be able to achieve the financial closure in and around 9.5% plus some upfront cost. So company will maintain 9.5 % as target interest rate coupon for the HAM project

4 Likes

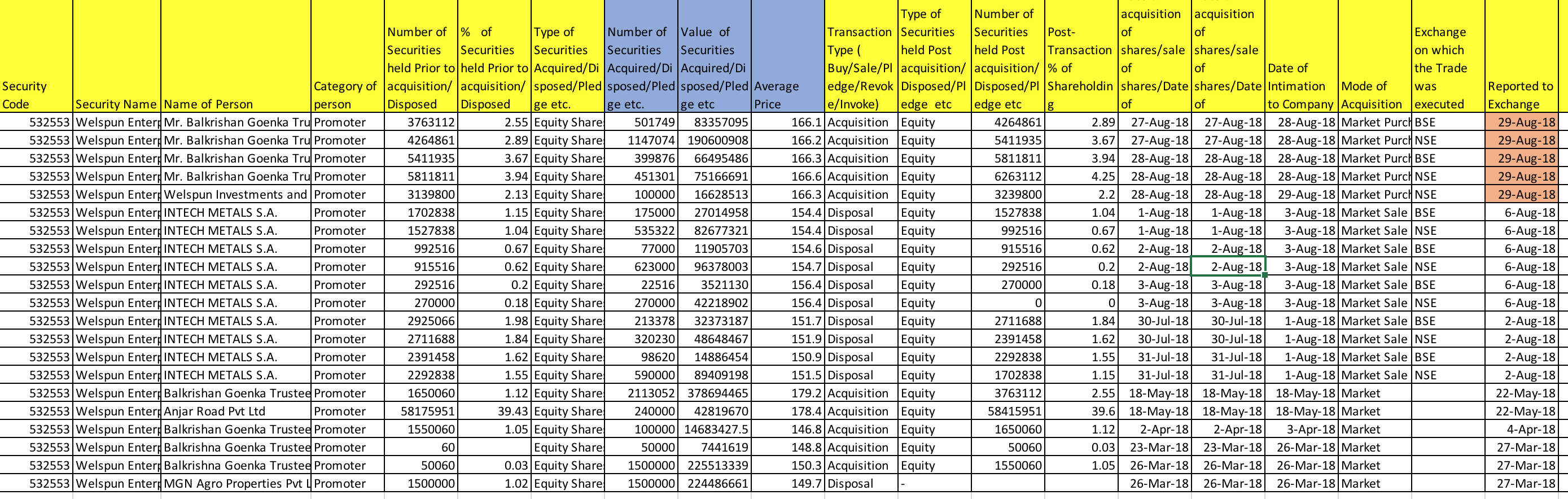

Guys, get Welspun Enterprises on your radar if not already. Promoter is buying decent quantities:

Disc : Invested

1 Like

HG Infra is the recently listed company undertaking road projects.

Highlights

a.As of June 2018 it was having orderbook of 5300Cr.

b.It used to be a subcontractor and now graduated as main contractor and qualified for bidding NHAI and other govt entities directly

c.This year FY18-19 sales may cross 2000 Cr as per the last concall.

2 Likes

I was wondering , why inspite of excellent order book and great quarterly numbers why market is not interested in Road Infra companies.

I attended couple of Infra companies (Welspun Enterprises, HG Infra and Sadbhav) Con Calls and here are the common things I could infer:

- Management is confident of achieving earlier declared Annual Revenue for this Fin year

- They got financial closure in Q2 at about 9.75 % interest rate

Concerns

- NHAI didn’t declare projects in Q2

- Companies hoping Q3 to be significant in terms of NHAI projects declaration

- Due to current conditions in financial markets, NHAI may provide majority of projects in EPC model and less of HAM

IMHO market is waiting for NHAI actions in coming quarters as election and Financial mkt conditions are major headwinds for this sector.

Disc : Invested in Infra sector via basket approach. Overall bullish on this sector for next couple of years.

3 Likes

Welspun Enterprise: Promoters acquired 30 lakhs shares recently. Avg price is 160. Total expenses on acquisition of shared 48 crores.

3 Likes

Was reading this short research Report by CRISIL “HAM in a Jam” : https://www.crisil.com/content/dam/crisil/our-analysis/reports/Research/documents/2018/november/crisil-opinion-ham-in-a-jam.pdf

As per this report, HAM projects awarded for 800 kms in FY18 face execution risk. Total 3400 Kms of HAM projects were awarded last year.

Basically highlights some of the problems with HAM : land acquisition delays, financial closure delays (as banks are cautious towards lending to the sector), regulatory clearance delays.

Pace of road construction (in terms of execution) could be ~10 kms/ day from 8.4 last year.

Though HAM is said to be a better model than EPC/BOT from a longer term perspective.

Welspun Enterprises results link

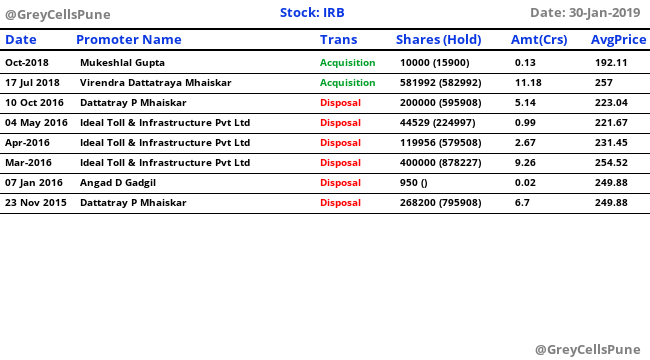

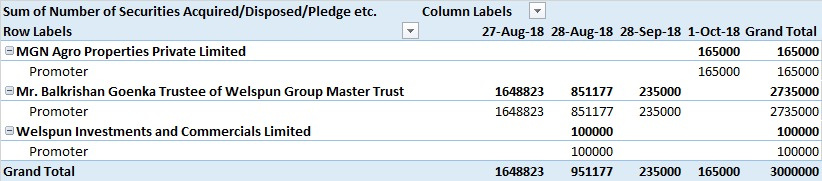

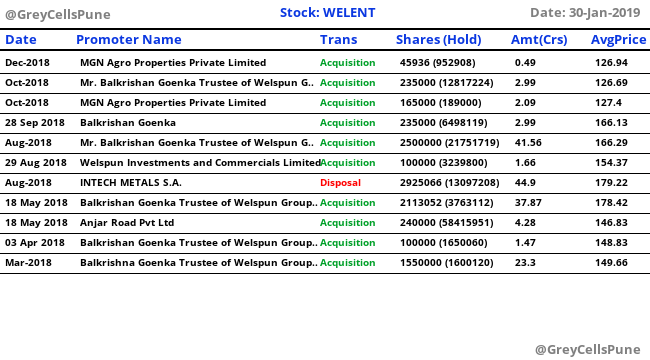

Uploading the promoter buying and selling details again for Welspun Enterprise

IRB