Quick background: I started saving in equities only in the last 2 years and prior to that was primarily saving via FDs/PPFs. Started investing in mutual funds since 2016 via SIPs and started looking at equities only in the last 3 months. This is my portfolio that I have as of today (most of the bets seem to be post the correction except a couple here and there). Would love feedback.

Notes:

My stock portfolio is only about 2-3 months old and I intend on investing aggressively in this. About 50% of my monthly savings goes into Equity MFs and remaining 50% into Stocks. The bonuses go into PPF and whatever is left again into equities. As of now debt accounts for 55% of my portfolio and I intend to trim it further down to 35% over the next year (allowing me to have cash to deploy in market in the next 6-8 months apart from my monthly savings).

Reasons for stocks:

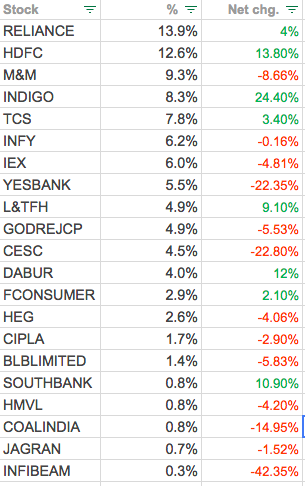

As you can see, my biggest holdings are in blue chip stocks since I am new and my only strategy was to pick a few sectors like IT, Auto, FMCG, BFSI and find some of the top companies there and invest. It’s only recently that I have started to look at midcap stocks.

Reliance: Due to Jio. Though worries that Mukesh bhai has taken too much debt. But hopeful that Jio will figure out monetization.

HDFC: Got it at a dip. Every mutual fund in the country has this stock, and thought can’t go wrong with this, exceptional management team.

M&M: Bought when the stock fell by 200 Rs (though it fell further). Believe that they are going to play a big part in electric vehicles, tractors etc. And because of good management.

Indigo: Possibly the only airlines out of India which can become a major international player and yet remain profitable. Fantastic track record of execution. Will probably hold unless there’s a major oil crisis.

TCS/INFY: Feel both these companies are embracing digital well and an increasing portion of their revenues are coming from these higher margin activities. Good management teams.

IEX: This is a long term bet on the fact that eventually all energy will have to come onto an exchange (as of now only surplus energy is traded here). This business has virtually no competition and has a 70% EBITDA with 30-40% PAT. The only issue is how quickly will the market come on board. It’s a matter of time.

YES Bank: Was too mesmerised by the price drop

L&T Finance: Hoping it will be a turnaround story. Management focusing on a few areas instead of doing everything like they were doing earlier leading to better profitability ratios (and hopefully reducing NPAs due to reduction in wholesale/infra lending).

FMCG buys like Godrej, Dabur, Future Consumer because felt these are innovative businesses (Future/Godrej more than Dabur), but Dabur has a strong rural presence and was hoping with the upcoming elections, it would fare well for Dabur. Future Consumer because of their added advantage due to their retail store presence which will aid distribution.

HEG just because feel the China opportunity will last another few years. It’s revenue/profit growth has been staggering over the last years.

Rest are just random buys (which I will divest in the next few months, except South Indian Bank, where I intend on increasing shareholding).

As of now my portfolio is about breakeven (actually a slight profit, since there’s additional shares from the CESC demerger which are yet to be priced)

I have a very high tolerance for risk, since I am around 30 and plan to invest about 40% of my equity portfolio in small/midcap stocks which are on a growth trajectory.

Thank you @1.5cr , really appreciate your inputs and advice. So as of now, my MF portfolio is about 2.5x my Equity portfolio. Would you suggest that I liquidate a portion of my MF portfolio (viz > 1 year) and put the into equity (till it’s 50-50). My MF portfolio is more or less at break even as of now. Do do you suggest continuing building my equity portfolio only via SIPs/bonuses?

My thinking is somewhat in line with what NPS (aggressive mode) defines as per age. Till 35 age, 75:25 and after each year reduce slightly the equity portion and increase the debt portion.

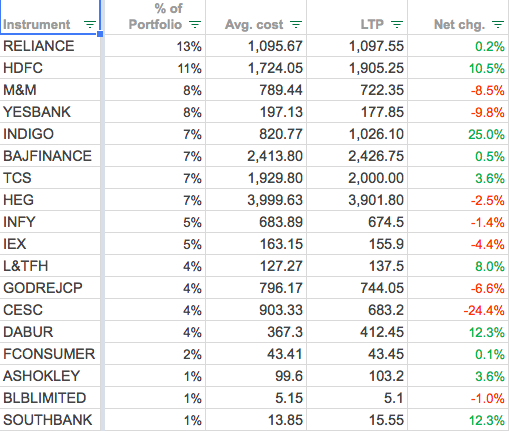

Changed the portfolio by selling the small cap which had < 1% shareholding. And consolidated the portfolio by investing in some of the companies like YES Bank.

Picked up Ashok Leyland since its at such low PE multiple, has shown improve in OPM as well as steady 30% revenue growth in TTM. Infact I intend to pick up more and bump it up to maybe 6-7% of the portfolio.

Also picked up Bajaj Finance.

The plan is to keep this portfolio for the next 5-7 years atleast. And keep adding during dips. I intend to soon sell CESC, BLB Limited.

Indigo- airlines is a space that most fail at making long term sustainable profits. You can read into the same and study further. In my view there are better ideas in the market.

HEG - Be careful it is a cyclical things go to zero overnight. With 7% weight I would cut it since it seems to be a momentum gamble for you. Take it to 3%.

Dabur is not the cheapest FMCG company You are paying 50x for a roce of 28% or so. In my view there are better companies like ITC at 30x with a higher roce of 35% and the ability to grow with a larger investments. You have jyothy labs who seem to know how to rebuild brands and they could do very well going forward as mgmt seems quite good. I would reconsider Dabur on that front. IF you are paying such a high valuation then you might as well pay slightly more on PE and buy a Nestle or HUL and hold onto it. You seem to be open to forgoing a few years of returns so why not consider the others. Nestle and HUL generate more cash. Dabur trades at Price to free cash of 82x or so, Nestle at 60x and HUL at 75x. So in essence Dabur is expensive and not cheap. Do not look at PE in isolation. That is what I keep telling @jamit05…

why would you think you have to exit yesbank…please see the yesbank thread…

I believe RBI has gone over board

No bank is saint here… even the likes of most expensive bank like hdfc bank

I may be biased have few K’s below 180

Simply because there are better places to be invested. You do not need to go through all these issues.

There are no extra medals for taking on extra risk. And in many cases extra risk doesnt mean extra return as in the case of yes bank.

It is not a debate as to which bank is a saint and which is not. HDFC Bank will always remain the gold standard this is not due to governance alone there are other factors as well.

Whether or not RBI went overboard is irrelevant to my reason.

For investors like us who lack information and access. We need not bet on Yes bank. Will you make more than 20% cagr in yes bank over the next 3 years? If the answer is no you really need to rethink your investment. The market does not forget corp governance issues easily.

Im not debating on Yes Bank or the RBI. I hope im wrong for investors sake. Im just saying that as an investor you dont need to own yes bank there are other opportunities for you to consider. Dont get hypothetical and say that even Asian paints can fall prey to misgovernance because it is not relevant to today’s investment universe in India. Today Asian paints is clean and Yes Bank? There is too much of smoke with regards to Yes Bank so why venture into it if you are not going to make abnormal gains…

Again not debating Yes Bank’s innocence. Simply saying there are better places to be invested where you can make perhaps better returns over the long run.

One question, I was able to get Indigo for cheap and at the same time feel that it’s got almost 40-50% market share is only going to grow. With more and more people going to take airlines over railways, don’t you think from a 4-5 years perspective Indigo is a good bet? They also have a moat in terms of the number of aircrafts they have and no other airline will be able to catch up in the short term right? And now they’re looking to go international.

I agree. But with 40-50% market share how much more can they garner? It is safe to assume that Jet issues will slowly get resolved and the airline will start operating on a fair level again. Vistara is taking things seriously. Spicejet have got renewed hope now. I do agree with you, in the short term they could grow nicely but bottom line is dependant on crude. And nobody knows what crude will do. The theme is great, the company is great the industry is not. From an investment point of view the cash sitting on the balance sheet lends lots of comfort. I would say since you have done research and bought early on. If you could tell me why and how Indigo will bypass this crude issue and pass on costs to the customer then that would make them a wonderful idea.

I feel Dabur and ITC are incomparable. ITC is cigarettes business in essence with very little profits and small percentage of revenues from FMCG as of now. It is great company to own no doubt but because of its conglomerate nature it is not comparable with a pure FMCG play.

You have pointed very interesting metrics of price to free cash. Thanks. Dabur is a rural India FMCG play and each company Nestle, Dabur and HUL are excellent businesses with their own great brands and strengths. HUL and Nestle being MNC, I am always little doubtful to own them as major part of portfolio. I maybe missing out (so far missed out) on them but never able to trust indian subsidiary of an MNC with major part of portfolio. I am aware corporate governance etc will be top class but vision for the indian subsidiary of the parent is what I am not sure in long term. Glaxo got sold and luckily for them, HUL was the buyer. Let me know your views.

Exited South Indian Bank (at 3% Profit) and Spencers.

Increased stake in HEG to average out (it was available at 2000) from 3499 to 2901 since feel there’s still some juice left and the price was extremely low.

After looking at some of the earlier posts by @Donald , have segregate the above portfolio into two parts, one is a long term portfolio (which I will hold on for 5+ years), or rather, just invest and forget. And the second will be for either:

a) Companies which I don’t feel yet are long term bets

b) Opportunities bets

For example, something like Ashok Leyland or Indigo I am not sure if it’s a long term bet or not and so will be type a) , where as something like HEG is a clear Opportunistic bet, which is just relying on the short term to see if it will rally and if it hits a certain numberI have in mind, I will exit.

Yes, I have enough cash to re-invest, since my current asset allocation is 12.5% equities, 10% MF (PPFAS/Index Funds) and rest in cash/liquid debt.

I have gone with defensive stocks with the logic that as and when the economy starts coming back up, the first companies to benefit are going to be the NIFTY 50 ones, since that’s where the institutional money is going to end up first. And since these companies also have a good 10-15% CAGR track record (of both earnings. (DMART is one that I am worried about since they are slowing down their pace of opening new stores).

I have been trimming off Indigo (it was at 17% of PF and now at 10%). I booked some profits (since it had gone up 50% from the time I had first invested). I’m thinking of trimming further, till it’s maybe 5% of PF. I’d still like to keep it since it has > 50% market share and feel that the airlines sector is bound to spring back up in the next 6-12 months.

As for the others, basically, I got rid of the non performers in my PF (Godrej, M&M, Yes Bank, Ashok Leyland) and tried to double up on the blue chips from healthcare and FMCG