Reproducing key extracts from the presentation made by me in VP Kolkata meet last Sunday:

Construction is the 6th -largest economic segment in India, accounting around 8 % of the country’s GDP in FY2016-17, the second-biggest employer (after agriculture), with about 35mn people engaged, and the second-largest recipient of FDI after the services sector.

FM in Budget 2018 continued to put a strong thrust on infrastructure development by increasing Government’s estimated budgetary and extra budgetary expenditure on infrastructure to Rs. 5.97 lakh crore against estimated expenditure of Rs. 4.94 lakh crore in 2017-18

Key Positive Policy Announcements in last few years:

Premium rescheduling for stressed projects

Bidding of tenders only after 80% land has been acquired

5:25 scheme which allowed longer tenor amortisation of the loan (upto 85% of economic life) say 25 years with periodic refinancing of balance debt say every 5 year

100% exit for developer after two years of project completion both for pre-2009 and post- 2009 projects

Cabinet approves Hybrid Annuity Model (HAM) for construction of highways

Government’s decision to pay 75% of arbitration amount to construction companies which have won arbitration awards against PSU .(HCC has been a key beneficiary)

Aggressive Bidding in Projects: Aggressive bidding in earlier BOT Projects had put majority of the grand old names in the sector in Financial Distress. This remains the major risk for all the players in Infra Sector also and key monitorable. Delay in Execution of the Projects: Project delays are quite normal in construction Projects (e.g. due to delay In LA etc) which result into imposition of Penalties by Client, increased interest Burden and overhead. Delay in Payment by Client: This results in High Working Capital Requirement and consequential higher Interest Cost Excess Leverage : BOT Projects require significant amount of debt funding. Hence any deviation from planned execution will lead to ill effects of leverage . Political Risk/ Influence : Public Sector being the client in majority of the cases , one has to live with it.

Discl: I am not a SEBI Registered Investment Advisor/ Research Analyst.I am invested in some of the Companies mentioned in this Presentation .

Will post more insights into the industry; Views invited

Construction, Development, Real Estate and Property Development are great sub-sectors. Problem is finding the undervalued asset. I am in a few names, but all of them are sitting quite high. But, the theme is good and finding good options is the name of the game. CHD Developer and Anant Raj are two names that are low priced and have not moved much, but then they are small caps so risky.

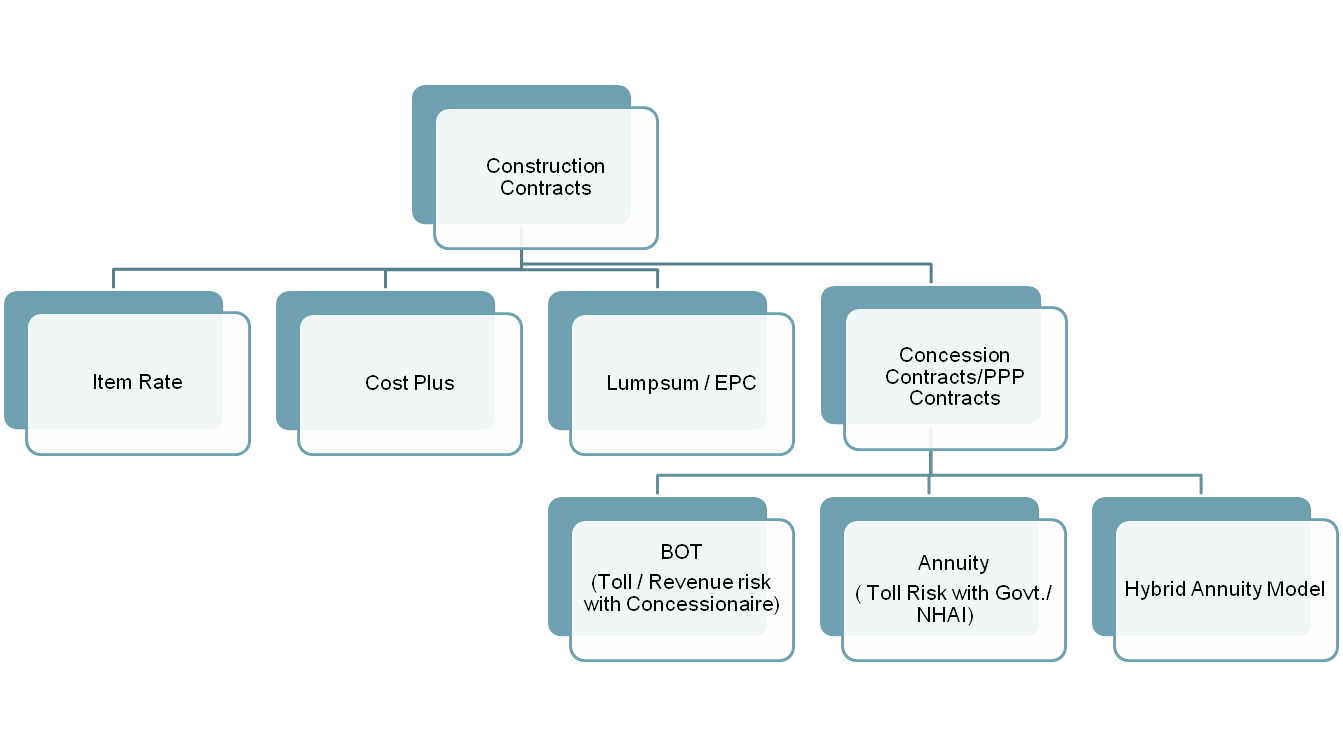

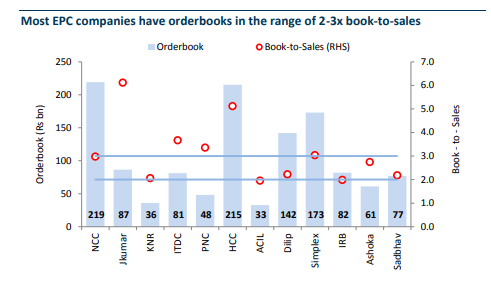

What is the breakup of BOT v/s EPC projects ?

Do younger players with healthier balance sheets stand a chance in bidding for BOT against distressed biggies like HCC, Ramky etc. ?

On what basis are projects awarded?

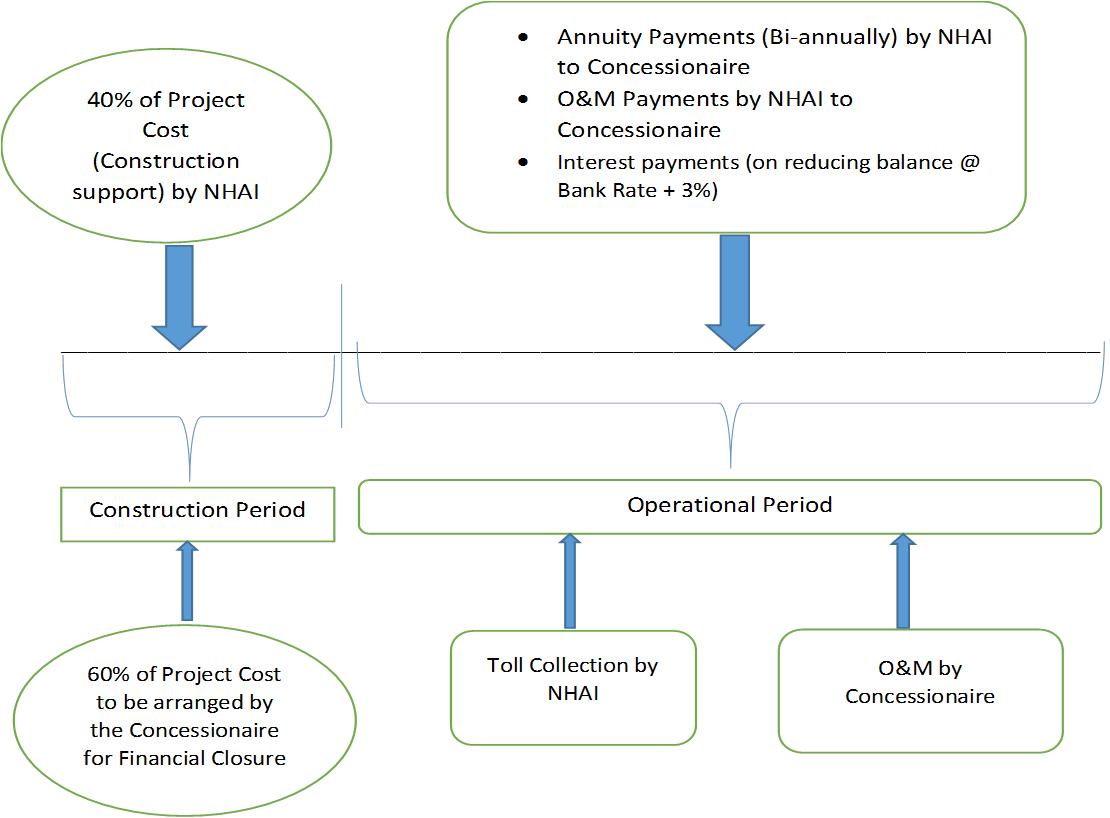

Since BOT was not successful in India due to inherent gaps in its model and implementation, NHAI is now resorting mostly to EPC Contracts and Hybrid Annuity Model (HAM). HAM is a much better model than BOT since the toll (revenue) risk is not with Developer and much lower equity requirement (since 40% of the cost is funded by Govt.)

Most of the new contracts are being awarded to newer players like Dilip Buildcon , PNC who have much better balance sheet and execution capability.

In HAM Bids are awarded to the developer quoting lowest NPV for project life cycle cost. Project life cycle cost is defined as NPV of the quoted bid project cost plus NPV of the operations and maintenance(O&M) cost for the entire operations period.

The Infra sector has moved up well and expected to continue their journey well into the 2X territory from a Capitalization size by this time next year. The number of construction projects are huge, backlog is good, sales is a bit slow/sluggish, and of course rates are rising, but they will improve as our rate structure environment start improving. Cement stocks, Real Estate stocks, Construction stocks, Land banks, Engineering companies have started to move, although with the flash-crash on 21/9/2018 is really showing confidence.

Why JKumar again!!! Locked in 20% lower circuit yesterday!

BMC issue in 2016!

Shell company in 2017!

And now SEBI doubting authenticity of documents submitted by JKumar pertaining to an order 10 years back!

What happened: SEBI has passed an interim order asking exchanges to appoint an independent auditor to conduct a forensic audit on J Kumar Infraprojects.

Attended the concall, key takeaways: See comments section