I feel , Repco result will be flat because of Severe drought like situation in TN for last 3-4 months and in fact in Q4 concall itself, they mentioned Q1 2018 will be flat. Repco’s main problem unlike Gruh, 62% of its business comes from TN. May be market is pricing it

2 Likes

I think we will need watch both revenue growth and asset quality. Management said they will set up a task force for improving asset quality. Will be interesting to see how the actual progress on the ground is, based on the Q1 results.

Repco is not a top notch HFC in my opinion. I had large holdings in 2014-16 but now exited completely. Apart from one state concentration there could be asset quality issues as their LAP portfolio is not small. Need to wait for the results. It is better to concentrate on Gruh/Canfin or PNB in the HFC space.

3 Likes

Repco business model is different from others. Their Key focus is Non-Salaried People. They are very clear that LAP portfolio should be of 20%. Their NIM is consistently 4+. On NPA, their average Net NPA is .5% in the last 15 years.

Now on LAP, just FYI, Bajaj Finance in its recently Q1 concall mentioned tha they are increasing their LAP exposure. In case someone remembers in Q3 2016-17, mentioned they are reducing LAP exposure as market is risky and then market started shorting Repco.

But except of over concentration in TN, I don’t see any major risk unless general market tanks. Finally results matter

I am expecting book value of Repco in 2017-18 in range of 195-205. We need to see. I am not expecting Q1 to be great. But overall management is good and well proven.

1 Like

The efficiency numbers have been top notch but what the market is looking for in repco is growth. If you look at efficiency ratios of canfin, repco would beat them but the growth (loan book and disbursements) has been muted for repco for a while now. Unless they can get back to earlier levels of 25% growth, the stock should remain range bound.

2 Likes

They promised 20-25% growth this year and TN Property registration issue

also resolved in March this year. Q1 Number and management commentaries

will be important. I am not expecting a great Q1.

Repco’s NIM and spread will be higher compared to Canfin which lends to mainly salaried class. In terms of business model, Gruh is closer to Repco. It is also growing at 20%. For Repco to grow at 25%, they have to go for LAP, which is higher risk.

In my view, it is both the consistency in growth and asset quality that market is looking for. Even after taking in to account of the parentage, Gruh is valued twice Repco.

It’s business model is quite different from Canfin and PNBHF due to customer profile. Non-salaried is far less crowded space. The question to me is whether it can achieve consistency with both growth and asset quality.

Disc- invested and waiting to see how FY18 turns out.

1 Like

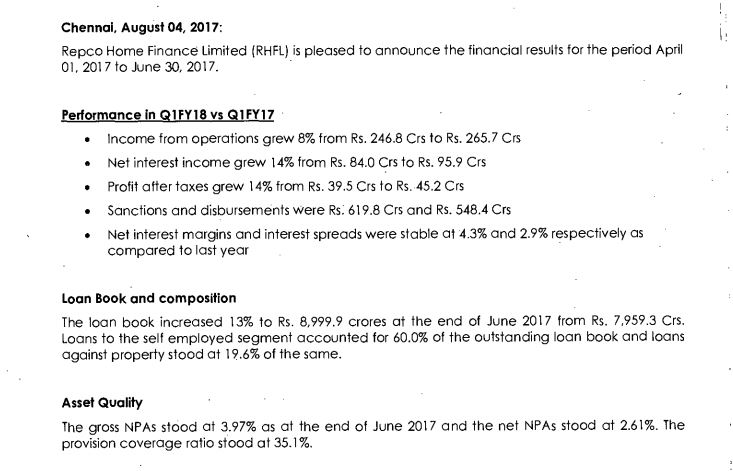

Result disappointing. Significant spike in NPA. Higher than after Demon time. Just saw Last Year Net NPA was less than 1.4 around in all quarter

actually repco june NPA always ho higher due to seasonality june14: 2.2, june15: 2.2, june 16: 2.2, and it comes down by in later qtrs: march 15: 1.3%, march 16: 1.3%

but after demon , gross NPA went higher to 2.6% and that because of same seasonality has gone up to 3.97%.

that said, two key concerns: increase in NPA is higher than historical NPA increase and mgmt has not been able to bring down early NPAs reported till march 17. we will have to wait til mgmt con-call on tuesday to get clarification on the same.

I can relate well with Lakshmi Vilas Bank result. Both of whom heavily

concentrated in TN. LVB- spike in NPA because of SME sector. Same being

reflected in TN. Unless Repco diversify geographically faster,no point in

paying higher Book Value. There are other good opportunities emerging

Another point , need to understand how affordable housing playing ? It is

playing for Gruh pretty well.

When they declared Fy17 results, management did mention that Q1 is going to be slow. Hence 14% net profit growth isn’t very surprising. What is worrying though is that the asset quality continues to be bad.

I learnt a big lesson in Repco - it is better to stay with the leader in an industry/segment. I sold Gruh, while keeping Repco 2 years back. My thinking was both had huge scale of opportunity (small ticket housing loans), with less competition (again due to small ticket loans to non-salaried class) and Repco was much cheaper than Gruh. I guess it was cheaper for a reason!

We need to wait for the management commentary to get further insights.

4 Likes

I exited few months back after learning a lesson. It is all about the segment it operates. If you follow their concalls over the last few quarters, analysts were particularly worried about LAP and informal economy. Due to DeMo and GST informal sector will continue to face pain. Long term would still be ok due to sector tailwind but high NPA might slow down their near term growth.

2 Likes

i shifted from repco to L&T fin holdings after the former’s CMD was

arrested by investigating agencies. conviction in the latter was higher due

to management’s commitment to increase ROE.

shiv kumar

Gruh on any day is leader of the pack in terms of Financial Metrics

1 Like

Gruh current numbers are also very good,look at their disbursement numbers are excellent , I think this is the first company that getting advantage of pmay . I feel that growth rate could trend upwards of 25%. Disclosure 30% portfolio, and will add more looks like it could reach 100000cr market cap, or is showing signs of it

Hi All,

Did anyone attend the Repco con call today? If so, can you please share notes / key highlights.

Also, did the management share any insight on:

- reasons about the deterioration in asset quality - what led to it and how long is it expected to last?

- increase in competitive pressure? I had asked the management post Q4 results if they are facing the squeeze, and their reply was no. But the slow down in this quarter and the migration of loans to other HFCs seem to indicate otherwise.

Will be helpful if any member can share the management views from today’s call. Many thanks.

Yes. Management was pretty transparent and shared all the possible sliced and diced numbers, analyst asked for

2 things affected them majorly

- TN registration issue which got resolved in end June + TN Sand non-availability that affected Pvt developer

- LAP loans ticket size 1 cr-3 cr

Rest of the Key points

- They are sticking to yearly growth of 18-20% and net NPA of 1.5%

- They are getting good responses in affordable housing in MH (25+), Telengana (20+) and KA

- All of their growth are coming from affordable segment

- They are expecting things to improve next Qtr onwards.

- In order to comply RBI 90 days rule, some accounts moved to NPA category where dues may be 1-3 EMIs

- They are expecting TN to pick up now and they deployed special team for rec0very

- Given their key segments are self-employed, because of cash issue, NPA gone up

- In TN, because of registration issue, many Accounts could not sell alternate houses to settle their accounts

4 Likes

Hi Nil,

Thank you very much for sharing the notes – really appreciate you putting in the effort to do that.

Some of the issues seem transient (TN, LAP [hopefully]); however, the increase in competitive intensity seems to more structural in nature. The management has been pretty sanguine about it so far, but I think it merits close monitoring, when coupled with the geographical concentration of Repco’s book.

Repco income will be always be lumpy in nature. We need to understand , its NIM is one of the industry highest, 4.4%. Also they have reduced Fresh LAP disbursement last qtr. Also they are not in unsecured lending. Their NPA in last 16 years, average .7-.8% ( you can verify data).

Given all these, investors need to have patience. One thing- yesterday Management did not hide any data and was extremely transparent, which I really like.

In LAP, they are reducing ticket size from earlier against property 1 Cr to less than 50L now.

1 Like

Annual Report of REPCO for FY 17 is out. Check it out

Major Takeaways:

- FY17 was a year of one-offs with state elections, Madras High Court order and demonetization driving loan growth to a 10-year low of 16 % YoY.PAT forFY17 was up 21 % YoY to INR1.8b, with RoA/RoE at 2.2 %/17.4 %.

- Management expects good growth in Maharashtra, Telangana and Karnataka. Management intends to open 10 new branches in FY18, across Mah., Guj., AP and TN. 2017 was an exception

- Management endeavours to achieve 1.5-1.6% GPA ratio by year-end. Effectiveness of the constituted task force needs to be closely monitored

- The mismatch of loan book growth and high NPA’s needs to be evaluated in the upcoming quarters

1 Like