Thank you, So much. that makes decoding the figures easy.

interview of MD:

Can some one explain following?

1 Like

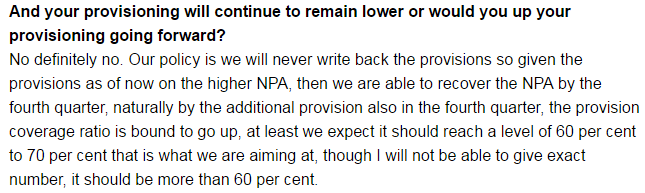

What this means is Repco has set aside 43.6 Cr for suspected 100 Cr of potential NPAs (Provision coverage being 43.6%) on the higher NPA base stemming from demonetization.

So with collections recovering in Q4FY17 and additional provision in the same ratio would see Provision coverage go up - say 43.6 Cr on 90 Cr potential NPA (or 48.44%). Company will never write back provsions, and going forward with better asset quality with the same provision would help attain a coverage ratio of 60-70%

3 Likes

thanks. it is clear now.

Housing sales fall 31%, launches dip 40% in Dec quarter: Report

The stock of unsold houses however fell marginally by 1 per cent to 4,53,592 units in Gurgaon, Noida, Mumbai, Kolkata, Pune, Hyderabad, Bengaluru and Chennai from 4,59,067 units in the previous quarter, said PropEquity, a real estate data, research and analytics firm.

I doubt about reliability of HFC rally ?

Don’t think that assumption is correct. HFCs need rising income and affordable housing stock to do good business. Data on large inventory is backward looking and in any case will ensure stable prices. We need incomes to rise for housing loan demand to continue. There is no concept of inventory in rural and semi-urban centres.

2 Likes

I disagree but I could be biased since I own HFC stock.

I dont think there is a direct correlation between the data you show and HFC loan growth. Most grew last Quarter in-spite of the reports like the one you attached. I think most people who go for loans wouldn’t have had any major issues because its white money and generally would have benefited with some softening in price. With so much money in the system now rates are lower thats additional advantage for a guy who goes for loan. And especially if the loan is below Rs 20 lac, govt is offering interest subvention and budget has been generally good for people who are paying taxes.

1 Like

You can have excellent loan growth in any landing bussiness but the most important is asset quality and NPA over period. Current loan growth without improvement of borrowers repayment capacity could result in NPA. Don’t forget RBI’s 90 days flexibility to recognize NPA. Q4 and Q1FY17-18 will show real picture

Bank GNPAs may rise to 16-17% of loans in 1-2 yrs: Credit Suisse

At the end of Q3, a whopping 41 percent of corporate debt is with companies whose earnings are less than their interest outgo. Credit Suisse’s MD and Head of Research Ashish Gupta shares his detailed analysis with CNBC-TV18’s Latha Venkatesh on a special show - Indianomics.

1 Like

15 Likes

Rudra, insightful data backed observation. My compliments.

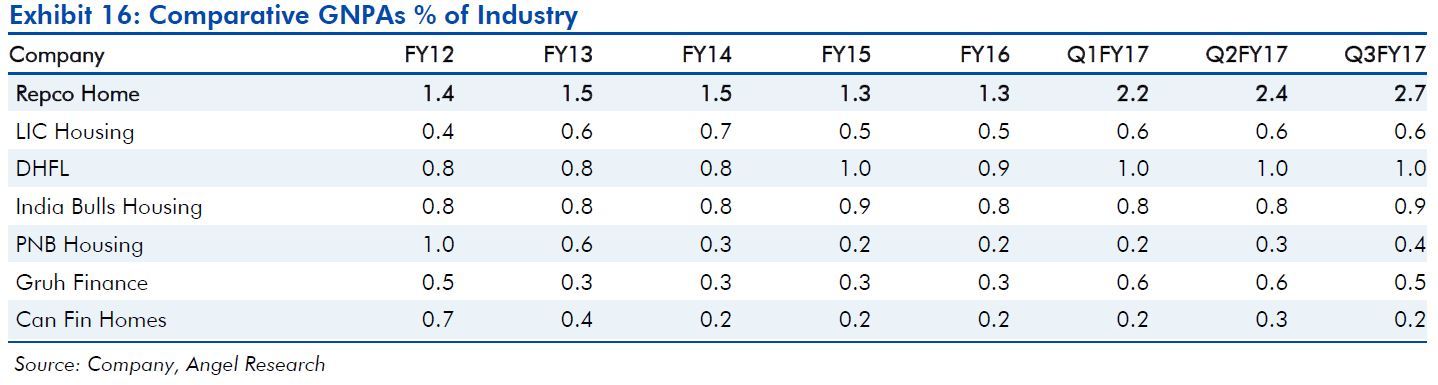

I wanted to shine light on some subjective aspects. We are coming out of demonetization effect and by now it is clear that one of the most severely impacted from this move were the small time self-employed people. We all heard about the issues of re-collection by bunch of MFIs, increase in the provisioning by some and subdued growth (if at all) by almost all MFIs. My sense is Repco’s main customer base is just one notch above the MFI’s customer base. And so like many MFIs they were also severely impacted. I do understand that the data shown by you is excluding the RBI time waiver scheme but the recovery tends to speed up only towards end of the quarters and so that damage from the GNPA perspective was probably already done in the 40 days of Q3.

The other thing is if you look at the GNPA numbers at year end then the trend is flattish downward from 1.4% in 2012 to 1.3% in 2016. The point that I am trying to make here is that at the year-end Repco has historically managed to bring the GNPAs under 1.5%. If you would look at the mid quarters in these years the GNPAs were almost always higher but in Q4 they were brought down. With demonetization impact almost completely waning off, I have no reason to believe why Repco would not be able to repeat history.

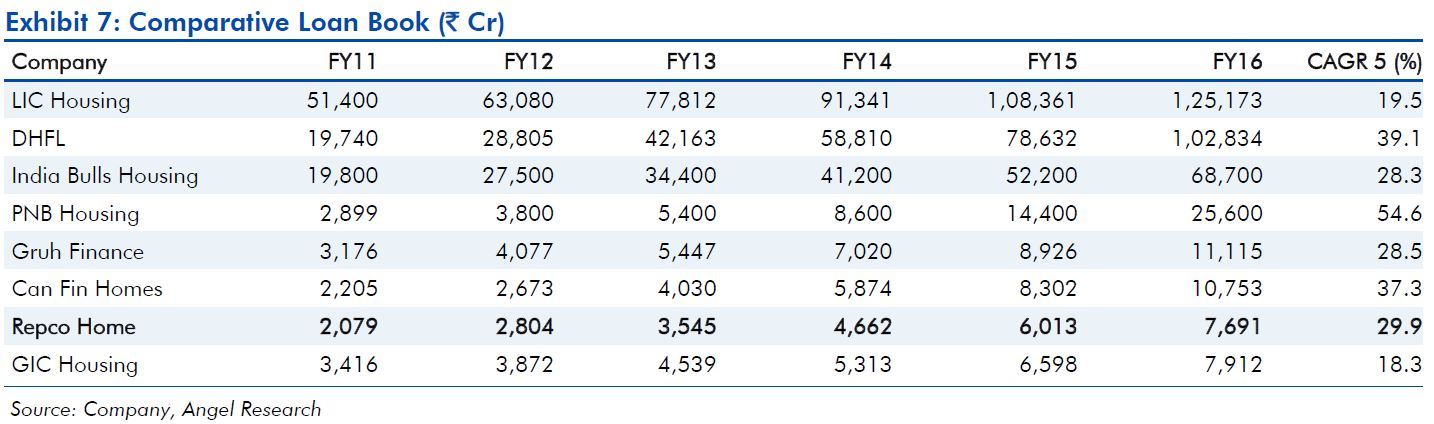

No comments on loan book growth except that 29% is good and with whole lot of tail wind for affordable housing I expect things to get better in couple of quarters.

Cheers,

Krishna

7 Likes

People need to read about Q3 Concall transcripts for better unerstanding what Repco management conveyed on NPA. They mentioned in Q4 m 2016, they brought it from 2.5% to 1.3 %. Repco’s NPA for the last 16 years average is .06%. They mentioned this number in many public forums

Disc Invested

And the most important aspect is that we cannot “really” compare Repco vs a

CanFin.

Repco is primarily targeted at the non-salaried segment and not the

salaried segment. The CEO clearly mentioned that the salaried segment is

too crowded and that they are not going to be “another player” there.

My 2 cents.

In case Repco started focusing on Salaried part, its unique positioning is gone.More than demonization , I am more concerned its over-dependance on TN (62%) and also significant drought like situation in entire south india

1 Like

80% of Repco loan book to be under affordable housing scheme,also provides details of how interest subvention would work

1 Like

DSP Black Rock Trust Fund has increase stake to some thing more than 7% as per the latest disclosure.

3 Likes

Q4 results out. YoY loan disbursements declined. Gross NPA at 2.6%.

Results on BSE

Company Presentation: https://www.repcohome.com/upload_image/fy17/RHFL%20FY17%20Earnings%20Presentation.pdf

Earnings call on Monday, Invite below:

1 Like

Key takeaway from Repco con-call:

- Loan growth to be subdued in Q1 FY18, to pick up from Q2 onwards, expect around 22% growth from Q2 onwards, overall 20% loan growth for FY18.

- co has created task force at Head office as well branches with NPA and focus is on to bring gross NPA from 2.6% to historical average level during FY 18. repco has given up on RBI dispensation and recognised NPAs

- tamilnadu property registration under Panchayat issue almost resolved and normalcy in loan disbursal from Q2 FY18

- company managed to perform well even after 3 key issues in FY17: tamilnadu election, demonetization and property registration in tamilnadu

- cost to income to be stable around 16%-17%

- plan to increase PCR to 70%

- disbursed loan for 500-600 cases under govt CLSS scheme

- PMAY : still projects needs to come on stream

- 75%-80% of current book eligible under CLSS, 50% of fresh disbursals shall be eligible

- dont expect credit rating to improve in FY18

11 to open around 15 satelite centers and covert existing one to branches., plan to consolidate presence in maharashtra and MP

12 mgmt doesnt anticipate any negative impact from job losses in IT sector as they are not targetted customers for repco. - branches being sensitized on opportunity of PMAY/CLSS. mgmt may revise loan growth no after Q2 depending upon ground realities

- to reduce portfolio exposure from 62% in tamilnadu to 50% in long term as they have been reducing slowly since many year. this is reduce the single state level risk in portfolio

- incremental cost of funds at 8.5%

6 Likes

Any update on Repco?

inspite of entire market and HFC having tailwind, this one some how is not participating.

if it is for right reasons? which are those reasons?