Company Background

Redington is a leading distributor of IT and non-IT products in India and Middle East.

It has progressively evolved from a single-product distribution company to an

integrated supply chains solution provider with capabilities across distribution,

logistics and after sales services. It services 100+ brands in India with channel

strength of 30,000+ partners and 88 warehouses. In the Middle East, Turkey and

Africa (META) region it services 80+ brands with channel strength of 11,000

partners with 22 warehouses. Geography wise, Redington derives 59% of revenues

from the overseas region, while 77% of the total revenues are from the distribution of

IT products.

Redington (India) Ltd. (Redington), which commenced operations in

1993 as a single product distributor has now evolved into an

integrated supply chain solutions provider. As of 2015, it is the

second largest distributor of IT and non-IT products in India. It has a

diversified product portfolio across 170+ brands in different

categories, with a strong distribution network spread across India,

South Asia, Middle East, Africa & Turkey supported with adequate

warehousing facilities.

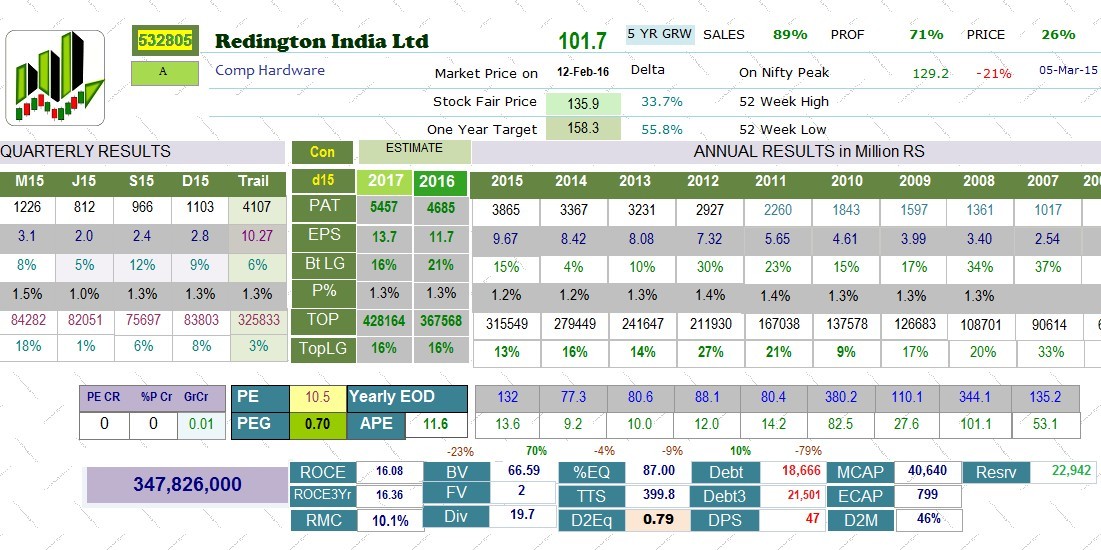

Particulars 2014–15 2013–14 2012–13 2011–12 2010–11 2009–10 2008–09 2007–08 2006–07 CAGR

Total Revenue 31,622.67 28,005.09 24,210.38 21,222.02 16,722.66 13,277.65 12,375.99 10,542.53 8,853.90 17%

EBITDA 761.89 719.61 684.20 633.40 471.65 365.72 329.57 259.04 198.47 18%

PBT 555.46 485.11 462.41 450.33 351.00 275.92 219.02 177.06 127.25 20%

PAT @ 386.53 336.65 323.11 292.74 226.00 184.33 159.66 136.07 101.70 18%

Networth 2,374.17 2,021.29 1,640.68 1,322.48 1,255.32 1,075.72 1,002.20 721.49 625.61

Capital Employed 4,446.83 3,993.84 3,947.11 3,477.61 3,186.28 2,464.57 2,226.51 1,505.44 1,226.88

EBITDA / Revenue 2.41% 2.57% 2.83% 2.98% 2.82% 2.75% 2.66% 2.46% 2.19%

PAT / Revenue 1.22% 1.20% 1.33% 1.38% 1.35% 1.39% 1.29% 1.29% 1.12%

Return on Average

Capital Employed* 17.22% 17.23% 17.69% 18.44% 16.01% 14.59% 17.23% 18.86% 18.19%

Redington India

FY15 R: Rs 31,555 crores

Segment

India R: ₹12,937

crore RS: 41%

Overseas R: ₹18,617

crore RS: 59%

Middle

East RS:

~68%

Africa RS:

~8%

Turkey RS: ~19%

Others RS: ~5%

Geography Distribution Strength

IT R: ₹24,297

crore RS: 77%

Non- IT R: ₹6627

crore RS: 21%

Services R: ₹631

crore RS: 2%

India Overseas

Brands: 100+ Channel Partners:

30,428 Warehouses: 88

Service Centers:

70

Brands: 80+ Channel Partners:

11,000 No. of countries:

21Warehouses: 22

Service Centers:

30

Key Investment Highlights

Leading distributor of IT and non-IT products

Redington’s revenues have grown at a 5 year CAGR of 18% to ₹31,555 crore driven

by consistent expansion in scope of operations through product and brand additions

and expansion to new geographies. The management has indicated that it will

continue to tap new verticals, product categories and geographies to fuel growth. We

expect Redington to clock a 2 year revenue CAGR of 15% to ₹41,524 crore in FY17

driven by:

10% CAGR in the IT distribution segment on the back of steady demand for

laptops

29% CAGR in the non-IT distribution segment driven by the rapidly increasing

demand for smart phones

In India, the IT distribution space is dominated by Ingram Micro and Redington,

which together account for ~70% of the total industry. The remaining players are

relatively small in size and lack pan-India distribution network. In Middle East too,

Redington Gulf FZE, the wholly owned subsidiary of Redington, is the largest player

in the IT distribution space.

a research report

I have done a basic DCF valuation. Please let me know how to attach excel.

The strengths I see in the business:

- Strong historical performance

- Market Leader

- Growth Options in few business segments

- Reducing debt leading to lower interest and hence better PAT margin

- Ability to grow without leveraging

- 13 Rs cash per share on books

- Benefit from e-commerce and GST (still not able to understand e-coommerce part, please check management address in annual report 20125)

- Local and assembled players falling market share

- Management guidance on loan reduction, using cash for capex for future growth

- 20% profit sharing as dividend

- No equity dilution in last 5 years

Risk:

- Working capital management is key to business and any issues with have strong impact on profit

- Middle east countries performance due to oil and terrorism

- Not sure but e-commerce may have some negative impact though management says it is favorable

- Apple opening its own stores for certain product lines

- Stagnant PC and desktop market

Currently trading at Rs 100, approx. 9.5 P/E