Hello,

I have come across this stock, and started researching on it, i have not find the thread on this stock so starting it.

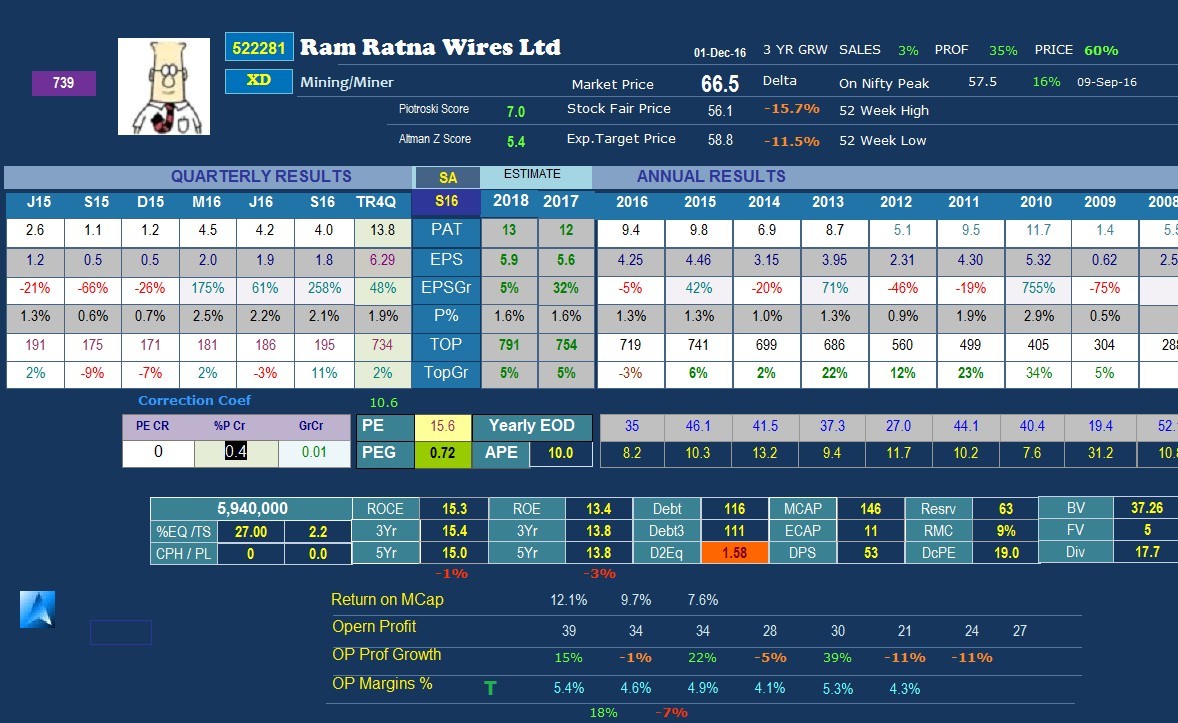

(BSE Code: 522281) (CMP: Rs.66.50) (FV: Rs.5)

Company Background: Ram Ratna Wires Ltd (RRWL) is headed by Mr. Rameshwarlal Kabra who has nearly 48 years experience in the enameled copper winding wire and cable industry with its leading and trusted brand RR Shramik in winding wires. RRWL is leading manufacturer and supplier of winding wires to the electrical equipment industry in India Gulf, Africa and Europe. The Company has set up a joint venture (JV) with RR-Imperial Electricals Ltd in Bangladesh to manufacture enameled copper wire, cables and enameled strips and has 10% stake in the JV. It also holds 2.15% stake in RR Kabel Ltd.

Products: RRWL’s products are utilized in various electrical equipments such as transformers, cables, transmission lines, switchgears, capacitors etc. Its product portfolio comprises sixteen products that broadly fall into five categories - enameled copper wire (ECW); enameled copper strips (ECS); submersible winding wire (SWW); bare copper strips (BCS); and enameled aluminum wire (EAW), fibre glass covered strips and enameled fibre glass covered and varnished strips. Its end products meet Indian and international standards including IS, IEC, JS and NEMA.

The Company operates in the transmission and distribution (T&D) industry and is the first choice for large original equipment manufacturers (OEMs) and top electrical companies in India as well as MNCs. Through its dealer-market nationwide, it also caters to thousands of small manufacturing and repairing units of electrical equipments in the country. Thus, it has an equal share of the organized and unorganized market spread across the country. RRWL continues to develop value added products like corona resistant wires and triple insulated wires as per customer requirements keeping pace with developments across the world.

Production & Technology: Its two state-of-the-art production facilities located at Silvassa are equipped with the latest machinery and have the expertise for manufacturing all types of winding wire – copper and aluminum, round and rectangular. Its production systems are customized to the client needs. RRWL focuses on production of more value-added items like enameled aluminum winding wire, fibre glass insulated wires and strips and paper covered wires and strips which have recorded a substantial increase in production. Even though an economic slowdown had plagued the power sector, the Company enjoyed a record production over the last couple of years. Its expansion plans are in the pipeline to meet the growing potential in the industry.

RRWL develops, processes and supplies RDSO specified high-tech products like corona resistant enameled wires. This product has the capacity to safeguard electrical equipment from the danger of premature burning of coils of equipment like motors which are fed from inverters. Likewise, triple insulated wires manufactured as per Japanese specifications (JIS:3005) and UL Safety Standards 60950 is ideal for items like power supply units in Electrical and Electronic equipments.

Sector Outlook: The demand for winding wires is directly linked to the growth of the power sector. The Union Budget 2016-17 focuses on accelerated growth within the power sector with an increased outlay of Rs.79884 crore. This combined with programs like ‘Make in India’ and ‘Skill India’ will boost the domestic production of electrical and electronic equipments which in turn will boost the demand for winding wires.

Winding wires and strips form a very important segment of the Indian electrical equipment industry, which includes both power generation and T&D. If the coil of any electrical equipment like generator, motor, transformer, relay or switchgear, domestic appliances etc. burns or fails, the equipment goes dead and hence winding wire/strip is often referred to as the ‘heart’ of the equipment. These products are used in almost all sectors such as Railways, Defence, Agriculture, Infrastructure etc.

Valuations: The promoters hold 73% stake in this closely held company. Its share book value is Rs.35 and dividend payout ratio is 21.62%. With TTM (trailing twelve months) sales of over Rs.700 crore, its RoE stands at 15.63% and RoCE at 16.95%. With improving OPM and profits in the coming quarters, RoE and RoCE are bound to improve.

RRWL will benefit from falling copper prices and weak USD as copper is the Company’s main raw material of which 32.74% of the total consumption is imported along with state-of-the-art machinery for quality production.

RRWL is expected to post an EPS of over Rs.9 for FY17 as against Rs.4.25 for FY16. Currently, the RRWL share trades at a P/E of just 7.8x FY17E earnings as against the industry average P/E of above 16.6x). As projected by the Union Power Ministry, every home in the country will have electricity by 2020. Moreover, the Union Budget 2016-17 has also given prominence to the agriculture and rural sectors apart from infrastructure. All these factors will boost the demand for electrical equipments in the country and domestic consumption in the rural sector, which in turn will result in huge demand for winding wires.

M Cap : 146

Disc: Investing for short term, in view of Budget Meeting to held in FEB.