Based on latest concall, the company expects 2H to be better since 1H was disrupted by planned maintenance. Outlook for Aluminium and hence the raw materials is positive given low inventory levels. Further a few Al smelters on N America and Europe are expected to be released started. Further due to China emission norms supply side of raw materials is tight. Based on latest con call the company plans to reduce debt to 3x EBITDA in the near term. And they are planning to add new capacity in AP.

As of the last 2 days - it would appear that Goa Carbon is hitting the upper circuit. Apparently the prices of Calcined petro coke are shooting through the roof but the company had also posted as you mentioned a strong set of numbers for Q1

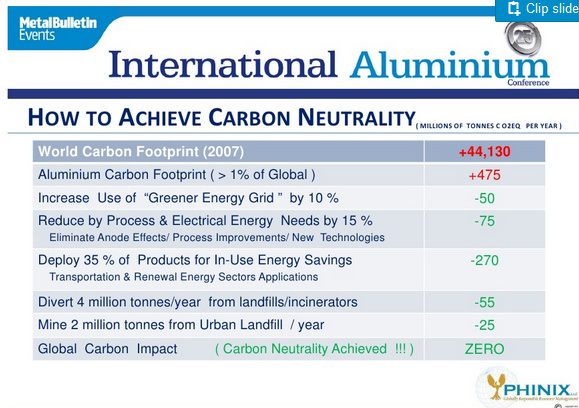

Interesting article future looks bright for Rain Industries & HSCL. The global demand for aluminum will only increase from here on as Aluminum can achieve carbon neutrality and thus push for it’s use by countries:

Price trend for aluminuim: ( thus the up move in NALCO ? )

{Price of aluminum is also rising due to increased cost of CPC, so I think this will impact industries using a lot of aluminum thus gives a good shorting opportunity. }

Is Rain industries trading very cheap and there is lot of value to be unlocked?

I see a lot of demand for Rain products

CPC (Calcined petroleum coke) Application:

i) Aluminum smelters

ii) Lithium Ion batteries for EV (Graphite anode requires CPC as raw material)

iii) EAF Manufacturing of steel (HEG and Graphite run into crazy valuations because of this) Competition:

i)Goa Carbon

ii)Graphite India

Rain is having its plants strategically located in various parts of world to take advantage

2. CTP (Coal Tar Pitch) Application:

i) Aluminum smelters

ii) Lithium Ion batteries for EV (Graphite anode requires CTP as raw material)

iii) Refer to Himadri thread for further details of application of CTP application Competition:

i)Himadri Specialty chemical ltd

Considering Rain has done lot of capex in past and realization is likely to start in the coming quarters, I am seeing lot of value even at current price that too when compare with competitors(Goa Carbon, Himadri, Graphite India) which are trading at astronomical valuations. HEG and Graphite India are in great demand because of Graphite Anode shortage all over world but you need CPC and CTP as a raw material to produce Graphite. I am of the view Rain is moving but not moving good enough as much it deserves. So I am seeing a disconnect in company prospects and price action. Please correct me, if I am wrong. Would be helpful to have your views on this.

Ref: http://www.asbury.com/ppt/CarbonsForSteelmaking.ppt https://www.oxbow.com/Products_Industrial_Materials_Calcined_Petroleum_Coke.html http://amcarbon.com/products/cathodic-protection/graphite/manufacturing-process

Note: There are also other products of Rain which I did not mention here as my focus is confined only to this 3 way demand which is very much the hot trend.

I am also invested in rain from 92 levels (30 K shares) for all the reasons you have mentioned… I am building my theory around exit targets and I guess your documents would help me in framing my variables… … thanks, Mukesh, NYC

Akshay - in my opinion, rain is not performing to the potential owing to

general lack of awareness of cpc/CTP as these were not widely tracked until very recently.

Other possible reasons could be management not marketing the company well. If you listen to the concalls most of the analysts are from abroad…so little coverage from Indian analysts.

other reasons cud be high debt and management seem to be ok with maintaining it at same levels and putting 80m$ CapEx

Overall , I feel next 2 qtrs would being lot clarity on how CPC and CTP shortage are impacting ebidta. And then we could see treating. I feel there is a long way to go for this global leader.

Rain Ind has performed very well in last 2 years. I had added at 35 about 2

years back expecting a cycle reversal. Did play out. Added more at 45

levels again last year and 110 sometime back.

Q2 should be good and Q3 even better, is what I think.

Right now, cycle is in a sweet spot. So planning to stay invested for

sometime.

Hi Jiten, wanted to know what is the deciding factor in investing at levels of 45 and then at 110.

I am new to investing and your input will help me, trying to figure out the right entry point is a challenge.

one big factor no one is factoring in is that fact that rain has a lot of profit pool emanating from its US operations. if the tax reforms pass, corporate tax rate might come down from 35 to 20 per there which will help improve the PAT nos a lot.

Shortage in coal tar in China is causing coal tar pitch to move up. Cyclically, both coal tar pitch and calcined petroleum coke margins have risen as witnessed by Goa Carbon results. Rain - well-poised

Can some of the experts compare the three companies valuations and tell which is better taking into consideration growth prospects, current valuations, promoters holding and equity, public holding, etc.

Phillips Carbon

Goa Carbon

Rain Industries

i personally feel Rain Industries looks most expensive of all…views invited