Thanks for correcting me I had not taken data direct from company’s website so her are chances that I missed something. i had put a small effort You are welcome correct me as I am still learning

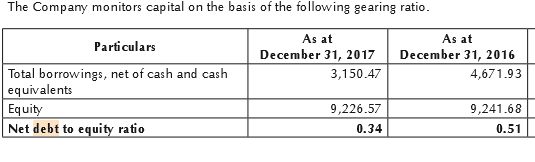

As per page 184 of AR-2017 Gearing ratio improved

Total Outstanding shares 336345679

share Price as on 5-2-19 103.5

Market capitalisation= 34811777777=3481.18 Cr

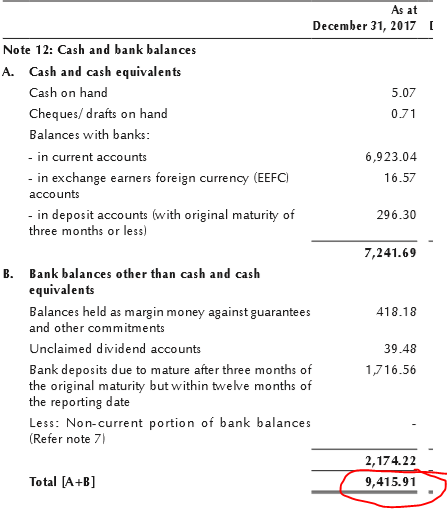

So total Cash and other equivalents = 9157.35+1281.31=10438.66 Cr

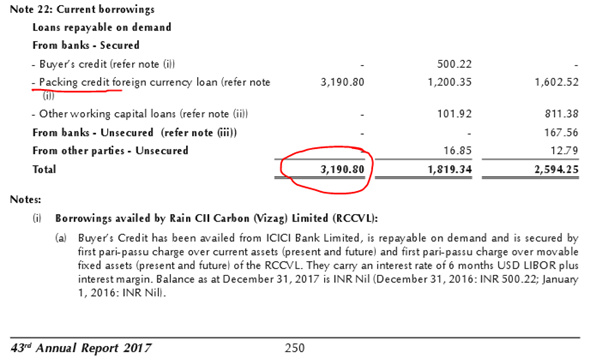

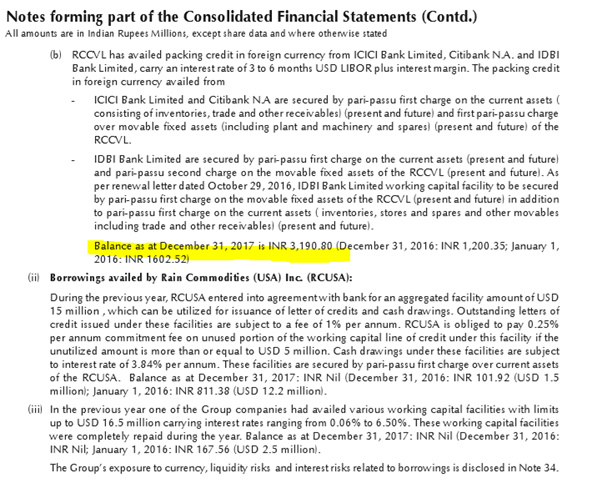

Long term Loan =3190.34 Cr

Short term loan =70 Cr

Total Loan/Debt=3260.34 Cr

Current price =103.5

With the above data I found Cash / share 310.3551094 Rs

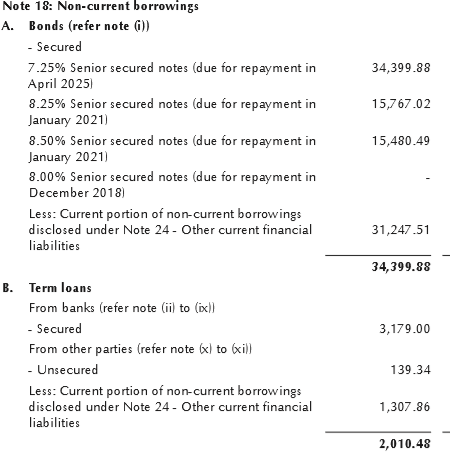

What I see the company has restricted it’s capital mix taking BOND Route amounting to Rs 34399 Cr

you can see this at page 246

Hi I am a new entrant to value pickr. I find all the discussions on this platform useful. I have one doubt on Rain industries. It has equity of around 3500 crore, debt of 6000 crore and goodwill of 5600 crore which means Goodwill is more than the net worth. Goodwill is only useful till that time company is making money, moment it stops making money value goodwill is nothing. Could anyone please guide here.

Then 2nd doubt is I don’t find much info about Rain on net, is it really a world leader in its domain.

Hi, Does anyone know how much of business will be impacted due to court decision? I think only India business will be impacted and global(US and Europe) business will not be impacted due to import issue. But I might be wrong.

Company which has potential to pollute weather (emission generating), society (liquor/cigarette)…get penalized by law…day by day low become more stricter…hence long term good CAGR return is very difficult unless people want its product at any cost!!

As clean and green world ask more cleaner company and its product…better to invest company which solve the pollution problem and make society healthy and happy

Valid point but can you imagine a world without aluminium. CPC produced by RIL is critical to produce aluminium under the only existing commercially viable process. Once Apple or Rio come up with better process, we can change our stance.

Only Indian business is impacted, which is a small portion of overall pie. But considering that they were expecting expansion in India and accordingly have already invested, this would be short term negative.

Overall the business is stable and under good management/promoters, so believe they will try to make the best of situation. Let’s have some patience.

Investing in RIL (like other companies) is a Test match play, lot of investors invested thinking 20-20 considering its run up. Unless you have long (many years) time horizon, RIL would be disappointing for your portfolio.

Thanks Vivek. I have patience to stay invested for long term. Reason why I was asking about India business is to see overall impact on the company and understand if this is the opportunity to buy more stocks since stock is at 2-3 pe now. Are there any concall/video having recent management interviews? I couldn’t find any. Even 2018 annual report is not there on screener.in probably I have to check on rain industries website to get the annual report. But Supreme Court order came in oct. so there will not be anything related with that in annual report.

They used to import cpc to blend as per customer requirements which dey wont b able to do due to ban. Hence not sure if only indian operations will b affected

Jagan Mohan Reddy has resigned as the MD and N. Radhakrishna Reddy appointed as MD for 3 years. JMR seems to be paying full attention to the Rain’s Carbon business going forward.

More details attached.

RIL reported the biggest net loss in the past four years in October-December quarter (Q4CY18), mainly due to lower operating performance and higher other expenses hit bottomline.

The company posted a net loss of Rs 139 crore in Q4CY18 against a net profit of Rs 307 crore in the year-ago quarter. Earlier, in December 2014 quarter Rain posted a net loss of rs. 200 crore.

Revenue from operations in Q3 grew by 9.5 percent to Rs 3,444 crore, compared to Rs 3,146 crore in corresponding quarter last year.

At operating level, EBITDA (earnings before interest, tax, depreciation and amortisation) plunged 82.9 percent year-on-year to Rs 118.1 crore and margin contracted 1,850 basis points to 3.4 percent in Q3.

Other expenses increased sharply to Rs 906.6 crore, against Rs 653 crore in year-ago.

Did any one attend the conference call, if yes can someone post the details, I couldnt find the call recordings or the transcripts yet in their official website.

Thanks for the link, however I tried to listen but the audio just stops at 0.00 and doesnt go ahead. Wanted to know if you managed to hear or am I the only one facing this problem.

This has been highlighted by management too in their previous press releases/ notifications to stock exchange. I am still holding Rain only based on this point. In case there are no exemptions for banned raw materials in SEZ, then their whole capex would be a mere waste and it would be a challenge to service the debt…! Hope the SEZ gets this exemption. In case anyone has more info on this matter, please share.