Revenue grew by 14 % to 34.9 Billion compare to 30.4 billion same quarter last year

2.9 billion or 14.6 % increase in revenue from carbon business segment

1.4 billion or 17.1%, increase in revenue from Advanced Materials business segment.

EBITDA decreased by 1.1 billion or 16.7% compared to last year same quarter with carbon decreasing by 1.0 billion and cement decreasing by 0.1 billion.

Advanced Materials segment margins was weaker in the third quarter, primarily due to increasing raw material prices, the impact of U.S. tariffs on some Asian sales and a few technical issues at customer facilities.

Gross debt was $ 1,130 million which includes $62 million of working capital debt.

During the year the company has invested over $34 million in the working capital required to run the business in the current high-priced environment. Despite this increase the company’s working capital borrowings have only increased by $12 million and the rest was funded with internal cash generations.

Company used $38.7 million towards long-term debt repayments during the refinancing that was completed in Q1 2018 and spent $120 million on capital expenditures for the nine-month period ended 30th September 2018. This included expansion capital of $24.1 million for hydrogenated hydrocarbon resins production facility being constructed in Germany and $5.3 million for the vertical shaft calciner company building in India.

Company ended the quarter with a Net debt position of $ 1,011 million and net leverage ratio of 2.6X based on LTMQ3 Adjusted EBITDA. With $ 101 million of cash on the balance sheet and unused credit limits of $ 144 million, the Company is comfortably placed to meet its obligations and continue to make the required investments to meet market demands.

Finance cost decreased to 1.1 billion compare to 1.5 billion last year same quarter.

Interest rate increase decrease to 5.3 % compare to 7.6 % last year same quarter.

Segmental Performance

Carbon business segment

Revenue grew by 14.6 % to 22.8 billion compare to 19.9 billion same quarter last year.

Average blended realization increased by 35.8 % after considering the favorable impact from the appreciation of the US Dollar and the Euro against Indian Rupee by 8.9 % and 7.9 % respectively.

Sales volumes of CPC and CTP decreased by 21.1% and 13.9% respectively partially offset by 1.4% increase in other carbon products.

The decline in CPC volumes was largely due to the timing of shipments, curtailments of few customers and delays before the calcining industry gained an exemption from the Supreme Court of India.

The decrease in CTP volumes was primarily driven by disruption in the production at customer facilities.

Advance Materials business segment

Revenue grew by 17.1 % from 8.3 billion to 9.7 billion rupees.

Sales in petro-chemical increased by 37 % which is offset by a decrease in sales volumes of engineered products, naphthalene derivates and resins by 2.9 % , 9.1 % and 8.1 % respectively compare to last year same quarter.

Average blended realization increased by 14.5 % along with the favorable impact from the appreciation of the Euro against the Indian Rupee by 7.9 %.

Cement Business

Cement sales realizations decreased by 5.6 % compare to last year same quarter and that was partly offset by increase in volumes by 6.1 %.

EBITDA decrease by 0.1 billion due to increase in operating cost and lower cement clinker ratio.

Company is working on reducing cost various efforts like

Installation of the waste heat recovery power plant at our Kurnool and Nalgonda facility to enable the plant to produce approximately 7MW & 4.1MW respectively of electricity from the waste gases generated in the manufacturing process. All the electricity generated by this unit is consumed at the plant itself.

Company has upgraded a cooler in Nalgonda Plant at a cost of ₹ 156 million to achieve energy efficiency.

Company is undertaking technology upgrade at our Kurnool facility to improve the efficiency.

Demand is increasing in various states and it will keep increasing due to housing and infrastructure projects.

Key Highlights

Factor affecting Performance

After 12 month company raw material prices were lower compare prices of finished products so it is a return in typical market in the quarter. Raw material prices costs caught up with average sales prices which has topped out and even declined and that was the reason for reduction in QOQ EBITDA.

There was drop in volume by 83 thousand metric tons , 117 thousand metric tons from carbon segment which was marginally offset by an increase from Advanced Materials and Cement segment.

Logistical cost was increased due to lower water levels on a major European transportation route. Then situation was further complicated by some customer outages and exacerbated by the India pet coke ban.

Company is shutting down factories in Germany which do not meet investment and return criteria. A $2.9 million expense was taken for associated costs incurred during the quarter, and company will spend the remaining restructuring costs during the subsequent quarters. Beginning in the second half of 2019 restructuring to yield an annual run-rate savings of $4 million after considering all the effects of the restructuring.

Company anticipate further impacts in fourth quarter from the resetting of prices, transportation disruptions and the India pet coke ban.

Due to Ban of importing pet coke in India company has to radically shift production schedules and reroute raw material and customer shipments, while simultaneously working to gain an exemption to the import ban. Due to ban company has to use high cost of Inventory during the quarter in India.

There was very little growth in aluminum production compared to the prior year.

This is primarily related to delayed restarts in the United States and a decline in production from China. United States aluminum production was further impacted during the quarter by two technical disruptions that caused plants to come offline. U.S. market outlook for aluminum continues to be bullish due to the tariffs that have been implemented.

Chinese aluminum market grew by 5.5% last year; however, in 2018, the market appears to have contracted due to a tightened supply of alumina and higher costs, especially for energy. It has become harder for the higher-cost Chinese plants to compete due to falling SHFE pricing and the three-month lows on the LME for exported aluminum, as well as a weaker Chinese economy

On a global basis during the last quarter, the aluminum market has been fairly turbulent due to conflicting signals related to sanctions, labor disruptions and plant closures, as well as reduced car sales in Europe.

Pet coke shipments bound for India received special permission to be stored at the port once they arrived in Vizag, resulting in unplanned storage costs. The petcoke ban also resulted in unanticipated import tariffs on GPC and CPC that had been shipped to Vizag for blending prior to the court’s ruling. Before July 26th company intention was to export much of that calcined and blended material back out of the country to customers in the Middle East and elsewhere so that company can avoid expensive import tariffs, since the CPC would not remain in India. Instead, since the import ban cut off company ability to resupply the Vizag plant. Company has to curtail exports from India to ensure that company have the inventory of CPC required by company aluminum customers in India until this situation could be resolved. This also meant that shipments that would have been exported from India would now be coming from company own calciners in the United States, resulting in incremental costs related to storage, import tariffs and legal fees in India, as well as some costs that will impact fourth-quarter earnings.

On October 9 – two and a half months after its original ruling – the honorable Supreme Court of India provided an exemption to calciners, allowing industry to import up to 1.4 million metric tons of green petroleum coke per year as a feedstock in the production of calcined petroleum coke. The court also provided the aluminum industry an exemption to import up to 500,000 tons of CPC with a sulfur content of 3.5% or below, which is manageable. Absent from the ruling, however, was an exemption for CPC imports by the calcining industry. At vizag plant company have imported as much as 250,000 metric tons of CPC in a year from U.S. plants and other global sources for blending to support Indian Aluminum industry and export markets.

Total domestic Indian CPC requirements are 1.6 million metric tons per year, and the domestic aluminum market requires approximately 1.4 million metric tons of CPC per year based on current production volumes of approximately 3.4 million metric tons. It appears that the court has aligned the exemptions with current calcination and aluminum production requirements. Unfortunately, this leaves no room for the expansion of either industry. Company is approaching the Indian Regulators to permit import of (i) CPC for blending and re-export of CPC to Customers outside India; and (ii) GPC for its Greenfield CPC Plant under construction in the Special Economic Zone (SEZ). Although SEZ plants have certain additional privileges for importing Prohibited or Restricted Items.

Q&A

Is the Q4 CAPEX of debottlenecking petro-tar plant is on schedule and what would be the capacity utilization there ?

It is on schedule and expect that to complete by December and the capital expenditure for the petro-tar debottlenecking is $10 million.

Capacity utilization will be 85-90 %.

Over how many quarters the reorganization cost will be spend in European facility and what will be the quantum ?

$ 3 million is the cost that company incurred in September quarter. May be company will have a similar expenditure in December quarter again.

In Carbon division the average price and volumes are down so what is the reason for this ?

Volumes were expected in the third quarter to be down compare to second quarter from a customer demand perspective. Volumes were impacted based on the current ban and product moving around.

Company see four quarters of very strong margins where sales prices were outstripping raw material advances and during the third quarter the sales prices did top out and, in some instances, did decline while raw material prices did continue to advance. So, there is a shared responsibility for the fall in profitability between both the volumes and the margins related to the quarter.

What kind of volume company is expecting in Q4 because company is now having good knowledge of how much volume company loose because of disruption in India in the CPC ?

Volumes should be stronger but company is still working off the inventories and dealing with the pet coke ban disturbances that have taken place.

Why company do not try to sell CPC direct to customer where company may not have ay restrictions ?

Company is working with that but that is a more time consuming affair because the material what normally company get is not calcinable directly, Company bring in kind of little higher sulphur and higher metal coke and then blend in India. So if company sell direct material which is compliant with aluminum smelter requirement the cost would go up. So it would be more profitable. Company can bring in lower materials that actually doesn’t need importation of GPC into the US. Company make materials with whatever materials which is available in US so that keeps company cost under control. So direct sales aluminum smelters is not very remunerative for company.

Does the impact of ban of pet coke will be for a longer period ?

No there are certain rules in the DGFT and company can bring it under advance authorization so company will get a resolution on that matter.

Does the problem of Germany related to low water level in the river will be a recurring problem for company in December quarter also ?

Basically, the river Rhine which is the lifeline for all the inland shipping in Germany between company and customers is very low. So company is able to ship materials which is about say 50% of the barge capacity because of the very low level. So of company customer can even take material but company is able to ship which means company is moving material through trucks and other alternative modes. There are rains in upward in Switzerland and other places. It is also impacting every large company in Germany.

On aluminum side prices have crashed to around $1950 and there are articles, almost 40% of the European capacity of aluminum might be cash negative. So does client is facing some problems with regarding to their cash losses and do company expect aluminum production to be impacted in the coming quarters maybe which impact company production as well in European facility ?

The discussion over the amount of aluminum capacity or the current production that maybe under water. The majority of that is in China and there is only smattering of production that are in high cost areas that really at current level maybe under water. They are fairly isolated. Company is not greatly concerned because company have not seen any report or talk regarding production coming off and certainly none of company current customer are affected by this.

The fundamentals on aluminum still remain very strong , production and demand estimates are still remaining strong and seem to be in a time lacked area of weakness related to the reported industries. It will not last over the medium term.

What would be the stable margins going forward and how company will manage the cost inflation ?

In market raw material adjust downward , consistent with finished product prices come off as well. So company is comfortable with its ability as company have to reset its cost consistently to protect margins. Particularly company was enjoying higher margins on the CPC side over last four years. Now company don’t expect that margin to come back but company will be able to protect standard margin in the Industry and adjust raw material cost consistent with the lowering finished product prices.

Company was having networking capital of $228 million which is now up to $430 million. So a significant chunk of money is in working capital so do company see networking capital to drop and to leave some cash for operations ?

$400 million will be the typical capital that company will be having in the business going forward. There could be $30 million reduction.

Around $ 200 million from almost 18-20 month is incrementally stuck in inventory and receivables. So is thar relatively to stay for $ 400 million as company guided ?

The raw material prices and finished products prices as compared to 2016 have almost increased by 60 to 70%. So as the value comes down basically the value of the net inventory capital net current assets will be coming down and inventory cost will come down. So actually, all the cash will be rerouted back to the operations basically to the cash flow. Company is hoping that once the prices do come down, that is an advantage in the business is when the prices are going up the margins improve but the problem is it also consumes lot of working capital but when margins are coming down or basically when the prices are coming down a little bit, all the cash will come back into the system. So that is one of the good things about this business.

Did company will be go for CAPEX plan of CPC business or holding it for some time ?

Company is proceeding as company is having all the approval for that including all the environmental and all the necessary approval and it should be operational in Q3 FY19.

Is there any problem in coal tar suppliers for company plants ?

No issue with raw materials

What is the plan for German restructuring ?

Company will shut couple of plants because they are not adding much to margin. There is also some people restructuring so there will be some additional cost indicated. Plants will get shutdown permanently . It is going to be value accretive starting Q2 2019.

Did company CPC volumes will be on normal level of 450,000 in CPC from Q1 onwards ?

Company do expect but not in this Q4 because company still want to get some clarification from supreme court and once company have it volume will start increasing.

On CAPEX projects, are they on track or any further delays? When is the Visakhapatnam CAPEX coming on stream?

In third quarter of 2019 there will be two or three months of delay

Did company have any plan for debt reduction ?

Yes company will not take further borrowing.

On CAPEX plan of 140 million how much is spent and how much is left ?

Company have spent $ 30 million till now, balance $110 million we will be spent in next year.

In European facilities which facilities is going to closed ?

Two plants in Advanced Materials segment is what company is planning to shutdown , partly in Q3 and some of them will be closed in Q4 of 2018.

For how many quarters does the reorganization cost will continue ?

This will be there in Q3 as well as Q4 similar amount expecting. There could be employee restructuring which will result in annual saving of $ 4 million from mid of 2019.

Out of $ 140 million CAPEX what is the capacity expansion in carbon and chemicals ?

Expanding 40,000 tons in hydrogenation plant. that is going to cost about $65-70 million and then company will have about $ 65 million shaft calcining facility being built at Vizag in India, it is 370,000 tons CPC plant with 15 MW cogeneration plant and then company have $ 10 million for debottlenecking of distillation facility to enable process petrotar which will increase chemicals production by 60,000 tons.

On Vizag facility did company will put it on hold and after getting clarity on the regulatory environment and then maybe go ahead with this project?

All CPC plants are rotary kilns, this particular plant is a vertical shafting, this produces a different grade of calciner petroleum coke which is needed by the customer. So company is going ahead of with the project. There is no going back and stopping of the project. There could be minor delay of two months or so in completing the project because of the pet coke ban and special economic zone will have certain privileges to import even prohibited or restricted items

What is the pricing trend in pitch?

From the pitch perspective, the pricing trend has been flat to weakening as seen on CPC side as well.

On CPC or Coal tax pitch business did company expect some more cost to increase in subsequent quarters?

The inventory has been purchased and company is working off those inventories. Company will work off that inventories the replacement values are in line with where company need it cost in order to protect margin.

After the Supreme Court fiasco that has happened, what about the customers that company is serving outside of India but in Asia, does company is able to export CPC out of India ?

Export to CPC has no restrictions. Company also have capacity so there is no issue in exporting it.

Do company have surplus GPC and CPC and does company servicing the quantum available ?

1.4 mt of GPC is permitted. Last year for example in 2017, the total imports of GPC were only about 1.35 mt of GPC into India. So, whatever that is there will be sufficient for meeting the requirements of all the Indian calciners whoever import. Where the issue is going to come in is, for example, in last year Rain imported about 250,000 tons of CPC, that is not permitted. So company may have some issues in meeting the Indian age forth commitment and company is trying to redirect it from US facilities to meet export commitment.

There is no growth in production of Chinese aluminum so whatever CPC capacities are available in China, are those directing towards exports and does company is surplus in CPC and hence margins to be subdued ?

Company have seen more volumes this year and company had reported the same thing during the second quarter that more volumes of Chinese coke available for export and that is consistent with the lower aluminum production numbers. Company don’t see them dumping product on the market as it was in 2012-2016 period as far as the CPC prices. They are though responsible for the volumes they have been exporting or responsible for the pricing weakness seen in India as well. Company is not too terribly concerned about continued drop in CPC prices out of China supported by strong GPC cost on them as well. They were responsible really for the price drops that and this trend will not continue.

How long it will take to inventory adjustment and how brutal it would be on for the margin for a one particular quarter because it has happened in past also where one quarter would just disappear in terms of profit, it will go to zero because there was a sharp movement in the prices and it took one quarter for the margins to up so does company see such kind of situation or it will be something similar in terms of margins that company saw in Q3 ?

Normally the inventory gets adjusted over a period of time, basically depending on how the prices move. But the prices are going up of CPC first and second in GPC . When they are coming down, the same thing happens is basically the CPC prices come down first and then GPC prices slowly follow. It takes time to stabilize. Once they stabilize, then actual benefit of inventory reduction will be seen. It will take 6-9 months for the inventory reduction to actually happen.

In term of overall industry capacity is there over capacity. or it seems to be more or less balance again? What would be company plan from a three to four-year perspective ? where do company see in terms of CAPEX , capacity additions or balance sheet deleveraging, how would the management like to see the company three or four years down the line?

On an oversupply situation company don’t see a rapid change. From CPC perspective company is seeing more availability out of China. If China continues to cut aluminum production, exports from China could become an issue again; however there are other issues also like the sanctions, the tariffs and such, that are disrupting normal trade routes. Industry will digest it and move past it.

Company remain very much confident of future demand of aluminum industry and looking out four years. There is still very strong expectation that in today’s cleaner, greener, lighter, faster world, aluminum will remain the light metal of choice. As long as that outlook remains, that macro trend remains company want to maintain leadership position in supplying the aluminum industry with the carbon needs and that is the reasoning behind the aggressive growth CAPEX plan that company have in place. There is nothing fundamental over the long-term saying that less aluminum demand and less aluminum production will be out there in the world for company to see and company want to maintain its position doing that.

What was the reason for fall in CPC prices ? How much production would be hampered due to blending facility not operating in the India plant also and in the US plant also?

Company is not operating 1.5 Kiln around 10,000 tons in the second half is impacted.

What is the reason for the fall in revenue fall in prices of CPC and CTP ?

It’s a market determined prices actually. The gap has been increasing for last two years or so and now they have started moderating

There is no major decline in the prices of CARBORES. It could be the change in the product mix because when company sell to different customer industry, different prices will be charged, but overall there is no major decline in the prices of CARBORES.

Management Comments

Long-term aluminum demand remains bullish in today’s lighter, greener, faster world. Company new product pipeline remains robust, and global operations are positioned to fill the needs of industry going forward.

There is some truth in adages…There is some element of truth in this one as well… Markets can be irrational longer than you can remain solvent. Depends where you stand and how much u can absorb. Market tempts…Markets always surprise…Consensus is end of market.

US to withdraw sanctions on Rusal. This means more supply of Al in the market, which should in turn increase demand for CPC manufactured by Rain.

Please correct if I’m wrong.

CPC rates in upswing. It claims to be worlds largest CPC producers. Ban lifted on usage of petcoke in India recently. Being a commodity its always be looked as risky business.

Stock PE - 3.89

Dividend Yield - 1.57

Mcap to sales at 0.31 (this year already did 13746 cr topline. Mcap is 4273)

Debt to equity - 1.86 (Risk)

5 Year Free cash flow to mcap - 0.80%

ROE - 24

ROCE - 17

However, this is negative for aluminium prices which are already struggling. Ideally, when aluminium cycle is on an uptrend, CPC and CTP business dynamics will be good. But off late, metals cycle has entered a downturn with China slowing down. I dont see any commodity businesses and hence stocks (including Rain) performing. Time to wait and watch and lighten position

Could you please help us understand the business cycle for Rain?

Typically, for cyclical businesses, when earnings and margins peak up PE will be low and similarly when earnings and margins are depressed, PE is high.

Successful cyclical investors always say ‘buy when PE is high and exit when PE is low’.

Is anyone aware of the litigation filed against Rain Carbon and few other companies in US? Need to validate if it is true. I can’t find any news on this elsewhere.

Its a tough Question , with so called High PE buy can only be done in dec-14 or in dec-17

in former case you would have still got 3 bagger and in latter case draw down of 70%. So i dont think one rule applies all …

Coming back to fundamentals, there are lots of factor which are outside the control which has happened last 6-8 months

i) Supreme court ban and subsequent lift only for existing capacity

ii) Rhine river water level receding , there by they could not ship the RM instead tehy had to transport to road increasing expenses

iii) The biggest of what i see is the Aluminium demand did not pick as expected in US and excess aluminium being dumped by china into other countries . Infact overall aluminium demand has reduced

iv) I am hearing some case in US but which is again doesn’t seem to anything worthwhile but sentiments are so bad that market has brutally punished, every relevant as well as irrelevant news

But these are also the pitfalls in investing in cyclical and especially one which is spread acros geographies ,i learned the hard way that there are various factors which we cannot anticipate , infact even management cannot some of these. The company is still getting lot of free cash , if you can ride the tide , it will surely reward in future but patience is the key .

But as the video says there is a rebuttal by atleast one of the firm and no impact on price of the shares of other firms that were listed. It video also claims that any liabilities on account of pollution may not be borne by Rain but the original owners it acquired from (though the narrator is not very sure).

Is Rs. 1000 crores of net profit sustainable? If the company is generating free cash flows, why the debt levels are still so high? They have recently undergone major refinancing exercise in FY18. Repayments till FY24 are minimal in the new debt structure; however, there is a bulk/bullet repayment in FY25. Why doesn’t the company utilize free cash flows to deleverage?

@ranjank The debt is at very low cost ~3%. As long as the cash can be deployed at >8% return the promoter will delay repayment.

Also - the company was in the doldrums in 2014 (low CPC prices). it was still able to generate abut 150 Cr of free cash to equity. (WC changes not considered). They are well positioned to defend the debt position until 2025 bullet repayment.

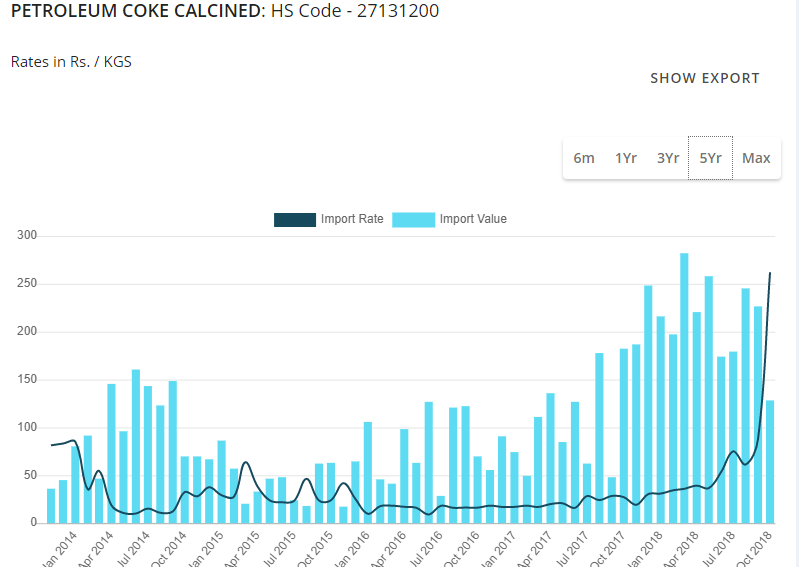

This stock is a cyclical play on prices of CPC. we have been seeing a consistent rise over the last 4 years. Is the trend down-wards now? Does anybody track this?