http://www.rain-industries.com/pdf/corporate-announcements/ril-analyst-call-intimation-q1-2018.pdf

Posting this initial thesis (based on this report Mohnish Pabrai invested in rain ind in the year 2014) again for the benefit of the people who did not go through from the start of the thread.

It has great amount of details regarding the Rain’s products, company’s background, valuation etc.

Disc: Staying invested. Avg buying price about 200.

Not recommending the stock for buying. The price may go down further from here too.

My novice opinion is it is about 20% cheaper than fair value.

1 Like

The above report seems to be 2012 or 2013 report

From the con call transcript:

Short term negatives:

-

CPC volumes have come down last quarter due to prolonged negotiations with Indian customers over passing on Import duty. This shows the supply demand mismatch existed during China’s winter cut does not exist any more tilting the balance slightly towards Aluminium smelters. According to management, during winter, the aluminium production did not go down. The CPC production was curtailed, which is coming back onstream after winter.

-

The high grade GPC (very low sulphur content), which is raw material for CPC, prices have gone up substantially, which they were unable to pass on to indian customers. US there is no such problem.

-

The Q2CY18 is going to be subdued too because of above reasons and also they are planning maintanance shutdowns this quarter as it is relatively dull with respect to demand.

-

Russel sanctions & Brazil’s Alunorte effect would be there indirectly, although not substantial, it will affect Q2CY18 in minor way, which is already turning out to be weak.

-

The new indian CPC capacity getting delayed by two quarters.

-

Crude oil price rise would impact the transport costs in minor way.

-

The last two major acquisitions (bigger than the size of the company’s size; funded by huge debt) spooked investors. The management gave hints that they might do an acquisition. Hope this time, the acquisition would be smaller.

Short term positives:

-

The indian rupee depriciation will show positive impact in Q2CY18 and further as long as it is weekening or staying at current 67.5 rs/$.

-

The Advance carbon material division which showed subdued performance during Q1CY18 due to shutdown and repairs, would run at full capacity in Q2CY18 and repair expenses would not present in other expenses.

-

CTP is doing well and will have no problem this quarter too.

-

US companies restarting aluminium production capacities would increase demand for CPC over next one year. This if it happens as planned would be significant positive for Rain in next 1-1.5 yrs.

-

The management is suggesting the advance carbon materials would see robust growth due to Engineered products going into Li-ion batteries. The contribution from this is very small (10-15%), so the impact overall is not going to be very significant.

-

The management says demand pick up for cement is visible in Andhra & Telangana regions, which would help with cement revenues (10% contribution).

-

Management sees robust demand for Hydrogenated Hydro carbon Resins (white water resins) and investing $66mln, which would start production in Q1CY19. The new CTP capacity (via debottleneck) would also come onstream around same time. The new 4.1MW power plant too would come onstream around Q1CY19. These would improve revenues and profitabilty.

-

The tax might be lower by 20-25 cr next quarter onwards (not sure though) compared to Q1Cy19.

Long term positives:

-

Rain’s focus on continued cost reductions would help it over long term. It makes it more resilient during negative cycles. With comfortable cash position, they might go for small acquisitions to augment more carbon products.

-

Over the next 2-3 years, as the size of the company grows, the net debt would come down and debt would look smaller, which would make institutional investors take notice of Rain.

The Chines production capacity cut which triggered Rain’s substantial re-rating is looking like coming back online, which might be reason for price going down.

Disc: staying invested with 2-3 years time horizon

3 Likes

The CPC volumes reduction may be marginal. The company wants to rationalize the inventory to reduce the working capital requirement and hence the possible outages but not with the prime focus to reduce the CPC volumes. As I can make it out though it’s not clear, that some sale meant for Q1 fell in Q2 this time too.

Hi all new entrant, disclosure - I have dabbled in this stock in the past but am currently not holding it. Most people on this thread seem much better informed than me so it would be great if the other participants can validate my initial thoughts on this.

I have gone through & appreciate all the detailed discussions on aluminium capacity expansion and also RM integration/ price variation etc but my feel was that the main story in the stock was the closure of Chinese capacity which would have led to shortage and increase in realizations that would have gone directly to the bottomline (akin to what is happening in HEG or Graphite).

That angle which was being marketed by the research reports (& perhaps the management also) is clearly not happening as per the last concall. In spite of the supposed winter closures Chinese production is up and talk is more on shifting the plants to less populated areas rather than any closure as such.

In such scenario, the fundamental business is probably not too attractive; cyclical, very capital intensive, bad RoCE, high debt (absolute levels still high even if cost is down after refinancing). On the flip side PE ratios are low and yes demand is strong so even if outlook on price is as good as expected realizations should be steady.

Also the way the stock has crashed last week kinda indicated that some of the strong hands may be exiting. The BNP paribas theory makes no sense as it is an arbitrage fund, so if they sold on NSE, they would have levelled elsewhere. More likely one of the institutional chaps or some HNI like Dolly Khanna may be on their way out. So broadly i feel if you got in at the beginning it’s still ok but not much risk/ return advantage from these levels. Any thoughts???

1 Like

@lastgenesis, all your points are well thought off, however it is difficult to interpret the dynamics of china aluminium production and curtailment in either direction because of the limited information available on many things. It was widely perceived that with China curtailment on aluminium production there will be Al shortage in world and will thus boost aluminium demand and production elsewhere which will increase the demand of CPC / CTP thus benefiting Rain. However we have seen that the China Al production has not dropped but increased marginally and China aluminium exports to USA have increased marginally despite Trump Import duty. This Trump import duty which has also become a variable has made Al production much more viable in America. There is enough information available to suggest that aluminium is going to be in huge demand going ahead and we have heard Smelters restarting in America.

There are also calciners units in China and their products CPC/CTP also needs to be consumed. These will be consumed by Aluminium industries in China else these may have to be exported in higher volumes than what is being done normally creating imbalance in demand and supply. These calciners were also targeted for partial shutdown / curtailment alongwith Aluminium smelters however we don’t know the proportions and scale.

Since rain don’t export to China, we are only concerned with what’s comes out of china, whether its aluminium or CPC/CTP. We certainly don’t want CPC / CTP coming out in abundance from China. Therefore restarting smelters in China may not be that bad. Having said that the demand of Aluminium is more than enough for everyone to have a good share of pie. Not to mention winter curtailments will be back.

Coming to exits by HN1. MP had said it multiple times in late Dec and early Jan that he wont exit as there is still some steam left. This was when Rain was around at 380plus something. No changes in his holding in Mar qtr and most unlikely to be in June Qtr else 2+2 will no longer be 4. For DK she entered in Mar qtr again and why would she leave unless there is change in fundamentals of the company which is not. Q1 result was good though may be not be as exceptional as few expected. But these biggies don’t exit on result day just because it was below some notch. Tell me what has changed against the company since the time these guys have entered. Potential and moat is still visible. Demand of aluminium has increased, price of CPC and CTP are on rising trajectory, cheap funding, lesser tax, redefined products, new profitable avenues, capacity expansion. All the geo political factors are going to have limited impact and will settle down soon as clarified by the company. With time when the sentiments improve this stock should start its next journey, how well it will be only time will tell.

The above is my limited uneducated analysis derived from whats available around.

2 Likes

If you have listened to the latest concall, it was clearly explained for the subdued performance of CPC. The price of CPC is in flat trend with downward bias.CTP is doing well with firming up of prices and reorganised devisions are expected to contribute inthe coming qtrs. Agn the Q1CY18 is tipid due to the Euro appreciation and closure of some units for maintenance and also payment of 34% tax.Going forward with the uptick of US Aluminium smelters ramping up the capacity with the restarting of old shut down capacities and expected new capacities, augurs well for the buoyancy in prices of CPC n CTP. With the new product for Lithium anode coating is expected to fowell considering the intension of world to move towards EVs.With the capacity expansion planned over next couple of years will keep topline growth as well as margin growth.Of course the debt is going to stay due to capex.

In view of the above, there is no deceleration in the growth trajectory planned by the company and with their intention to not to loose profitability for topline growth, they are expected maintain their earning growth. Price will sooner or later will catch up with the reality. Good luck.

Discl: Forms 5% of my PF with the intension to add more with stabilisation of price.So my views are biased.

I agree with most except price trend of CPC. The CPC price were flattish in India but higher in America. Besides CPC prices are expected to rise 500 plus from around 450 in 2018. So CPC price trend is definitely not having downward bias. To my understanding it’s the volume of CPC which was relatively less and higher input costs due to rising GPC prices which have been stablised somewhat.

Due to winter closing of Chinese smelters, excess qty of CpC is sloshing around. This demand supply mismatch is driving the CPC price trend in short term. ( This is as per Mr Gerard of Rain IND.). As u hv pointed CPC price will firm up once US smelters become operational. Rain’s enhancd capacity is also expected to be commissioned in 20/21.Their new products such as HHCR is well received by mkt which is fetching good margin. It is a growth stock n short term price zyration shd not cloud our judgement. Of course One arbitrage fund has played a spoil sport to destruct the price structure. This shd hv been anticipated when we know that one arbitrage fund is holding substantial qty.

Carbon Products segment margins used to be $60-80/t now $125-130. Now the question is how high can this go. My guess, we are more near the top, than mid cycle.

In Mar 2018 qtr, one of the clients bargained hard to keep CPC prices lower. We need to consider that alumnium companies (end clients) are now struggling with high alumina, CPC and CTP costs. although CTP is tigher, CPC not so tight (Chinese exports rising), I dont see big margin improvement hereon.

The company is expanding into value added products (right strategy) instead of expanding CPC/CTP or even paying off debt.

All put together, only pros are cheap valuations (7x CY19 PE on peak-cylce earnings?) and some volume growth. Dont see big returns for the stock in coming year or two, although dont see any downside too.

Lastly , I would like to reiterate Jiten Parmar sir’s strategy that in a cyclical u buy at a high PE (when earnings are depressed) and sell at a low PE (when earnings are at peak).

Disclosure: Sold my holdings and hence views may be biased.

2 Likes

It should be noted that of the growth in US smelting capacity that management mentioned on concall, more than half of the increase is by Alcoa which restarted its own calcination plant in US to supply CP coke to its smelters. So there will be some demand growth for independent calciners like Rain but not as much as the growth in smelting capacity would suggest.

The other question is what CP coke margin can be defended. Sequentially the carbon products ebitda/ton fell slightly from Rs 8432 to Rs 8344. But this included a big 30% jump in CT pitch realization which probably masked what actually happened in CP coke. It’s difficult to really isolate that because lower volumes certainly hit the margin but it would be safe to assume the cpc-gpc spread contracted

I agree that from here it is more about maintaining margin than expanding it. Also growth investors were attracted to this scrip because of sequential earnings growth while the spread was expanding which has ceased at least for now. The big sell off in the shares probably reflects those investors exiting. From here how does the stock go up? Will the value investors who missed the last run enter here? Or will they avoid it because of the lateness of the cycle?

The bull case is that China is starting a lot of new aluminum smelting capacity this year and next year. Some consultants estimate 4 million tons in 2018 and 2019 combined which would require 1.6 million tons of cp coke. That could soak up Chinese cpc exports and resume earnings growth for Rain. On the other hand, if all the new China smelting capacity doesn’t tighten the cp coke market we will know that there is shadow capacity of cp coke which has not been accounted for

2 Likes

The Aluminium demand seems to be strong.

1 Like

hi VP’s

Money is the blood line of any business ,The sole reasons of investing is for wealth creation measured in terms of money .

A peny saved is the Penny one earned .

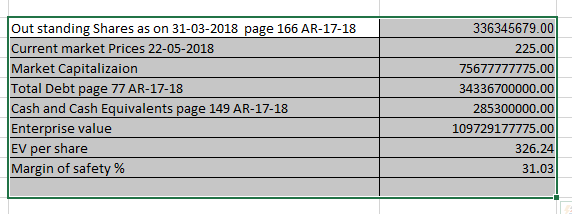

I find it is really time to relook in to the rain industry with exciting steps the mangement had implemented , some excerpts from AR 2017-18

also one can have optimum saftey margin ,Please correct me if i have done wrong calcultion to find out enterprise value per share

Disc: i may be bullish as iam holding the stock .This si not any stock recomendation .investor must dne his/her own research before, to look out for the various risks.investing

I don’t think your calculation is right. How can you include debt in calculating value per share? If you do it for any high debt company like Bhushan Steel / ESL / GMR etc they will be much much more discounted than Rain.

Disc: Not invested.

1 Like

Agree Varun. The calculation by Yourraj is flawed.

Imagine a company with 1 cr shares at market price of Rs 1/share. Debt of Rs 99 cr.

MCap Rs 1 cr

Debt Rs 99 cr

EV = 100 cr

EV per share Rs 99

Thus margin of safety is 99%???

1 Like

Hi varun , apreciated your opposing view ,

Capital-intensive industries will trade at very low EV/EBITDA multiples because their depreciation expense and capital requirements are so high

EV is basically a modification of market cap, as it incorporates debt and cash for determining a company’s valuation.It is represinting the theoretical takeover price if a company to be bought.

To certainextent you might be right as EBITDA is useful for valuing capital-intensive businesses with high levels of depreciation and amortization.

EBITDA = recurring earnings from continuing operations + interest + taxes + depreciation + amortization

in the case of rain

for this multipe you can refer to What Is Considered a Healthy EV/EBITDA ?

If you have som other means so i would request to share how should one calculate the EV in case of capital intensive industries like petrochemicals ,Power industries or oil or gas or Mining and metals or the one you mentioned it will be great to learn from you .

regards

It’s true that Enterprise Value and EBITDA are good measures for taking over a company. True that it is theoretical take over price, just control premium needs to be added. However, being an owner, I have to pay the amount due to financiers. I can not count that part as mine.

I would say, replacement cost can be a good measure to value such companies. I am no expert in this industry, so I generally stay away.

Also, personally I do not solely rely on comparative multiples. For me, first of all, the company should be fairly valued in itself. Then I would compare it with respect to industry finding more reasons why should I buy this company vs others in the industry. Many times, industries in themselves are overvalued due to optimism eg. housing finance last year, maybe insurance sector also. So, if I do not have MOS from the company’s fundamentals itself, it’s useless comparing it with industry multiples.

The link might look like I placed it in a wrong thread.

I am trying to guess what would be the impact of China’s shift towards EAF from blast furnace.

I have very very limited knowledge of all the basic stuff about steel manufacturing or CPC or CTP, please consider this post as a “food for thought” rather than for coming to conclusion on anything. Also, the content in article could turnout to be entirely untrue (only by 2020, we can tell whether their projection will be right or not). The counter arguments and facts to prove my basic premise to be wrong are most welcome.

It seems China is limiting the capacity of steel manufacturing from current level and allowing only new EAF capacity (less polluting) to replace the old blast furnace capacity (polluting). Since Chinese infra is at “maintenance stage rather than growing stage”, they will be getting more and more steel scrap every year which will be used in EAF capacity.

If I am not wrong, the Coal Tar (raw material for RAIN’s CTP production) is a by product of steel manufacturing via blast furnace method where coal is used. Assuming no major draw down in Aluminium production in China or proportionately (with respect to Blast furnace capacity) lower cut down in aluminium production would probably ensure less Coal Tar to CTP generation. Even though there is no export of CTP from China to other parts of the world (since CTP markets are localized due to specialized logistics needed to keep CTP in molten state at high temperature), the CTP prices are mainly influenced by Prices in China (I guess this is due to China being largest producer of CTP). Like graphite electrodes (forms 1% of production costs), CTP forms 5% of production cost in aluminium and can grow sufficiently before becoming unviable.

With China trying to use up more scrap domestically (it is mentioned that they put in 40% export duty on scrap), the scrap might become bit more expensive making the Blast Furnace production competitive across the rest of the world.

Counter point:

Again, Rain is just a converter and may not enjoy the gains due to pricey CTP, as Coal Tar price would have gone up due to supply tightness in china.

========================================================================

Another point to ponder:

The ban on Pet coke as fuel in india (whose raw material is also green petrolium coke) affecting the fuel pet coke price to come down (no idea whether prices have come down or not), which would further bring down the prices in GPC? The low price GPC is good for Rain’s working capital as well as decreasing production costs in case more low sulphur GPC is available.

Disc: invested @avg price of about 200 rs and staying invested. The above points are not part of my thesis for staying invested.

1 Like