so what does tht mean ?

Vedanta has declared their quarterly results

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=e40065af-480c-47ec-804d-b5ef34b110a6

There has been a solid growth in top line from Aluminimum segment during Q4 (qoq- 16%, yoy- 66%). Expect, raw material suppliers to Aluminium industry like Rain should continue to benefit from this uptick in Aluminium sales (have read that even Alcoa in their conf call mentioned that raw material prices are firming up).

Disc- invested in Rain from lower levels and added further to my position in last 1 week. Not a buy/sell reco. Pls do your own due diligence.

1 Like

Koppers in its carbon business reported EBITDA which was double the prior quarter level and almost 7x versus the prior year quarter. They mentioned strong pitch, naphthalene and carbon black feedstock demand as the main drivers. Their business competes with Rain’s distillation business (Rutgers). Also, a CP coke competitor in the US reported a very strong quarter. By extension, if Rain is able to achieve similar margin, it would imply a strong quarter as well, perhaps around Rs 11 to 12/-

3 Likes

A simple explanation of Rain price action https://twitter.com/prashmundu/status/993910425229066240

5 Likes

Apple invests $10 million in carbon-free aluminum production project.

Not sure if they mean that CTP/CTC will not be used for producing aluminium. The technology will be available in 2024 as per the article.

It appears material used anode of the new technology is different from conventional method

If it works out, it is going to replace CPC anodes (and CTP too if I am right) used in aluminium manufacturing process. The anode will be replaced by some inert anode made from undisclosed material. In one of the articles it is mentioned that Alcoa is already using this method sine 2009. They themselves are setting a target date of 2024, with lot of unknowns. The cost of manufacturing the new inert anode is going to be primary. Since the carbon anode is made from byproducts of other manufacturing processes, the carbon anodes are cheaper (my estimate). They did not mention anything in press release about cost factor of new process.

If it works out, it is good for the world and Bad for carbon companies like Rain, Himadri etc. The investors need to keenly watch the developments on this front over next few years.

Disc: Invested & is significant part of PF

2 Likes

Results announced , seems ok to me , why stock falling 7% …I dont track this company. Can any one please analyze the results and share your views

exactly, results are not that bad either… the profit seems to have declined due to tax expenses which were very less in previous quarter (could anybody please explain me the reason for this?) … Rain is right now down by more than 15+ % at the time of posting this message.

1 Like

Pretax net profit is still higher than last quarter

406 crores vs 322 crores (Ending Dec’17)

Deferred tax costed them 140 crores this quarter

(which is a one time factor)

So a net profit of 265 crores this quarter

There was one time accounting benefit in Q3 which increased the overall after tax net profit

Barring the deferred tax this quarter result looks very good IMO, considering the fact that this is the highest pre tax net profit ever!

Revenue is also up from 3147 crores to 3306 and carbon segment revenue is also up

Only cement sector didn’t perform well

Again good results for me

1 Like

Investor presentation -

Press release providing detailed information about Capex plans and Debt situation

Q3FY17 had one exceptional item which brought down the pre tax profit. So, ideally profit wise, Q3 was best quarter.

The CPC volumes were down marginally due to extended negotiations with indian customers over import duty (from presentation). The current quarter’s tax % would be standard going forward (my guess not sure though). The US and Belgium tax reduction benefited rain to reduce tax by about 3-4%, thus bringing it down from 34% to abt 30%. There are some oblique pointers regarding China. Finance cost reduction qoq is good. The inventory increased by 500 cr qoq is also good if demand stays intact.

From presentation management is optimistic abt rusal sanctions and Brazil alumina company’s production coming back to normal in 6 months.

New CPC capacity to come online in 1and half yrs from now.

Market is seeing something which we don’t know of. The apple, Alcoa could be one.

1 Like

That would explain the sudden 17% drop.

@naruto : If you see the trade value, they have sold stock only after it went down more than 15%. So, that may not be the reason.

1 Like

Thanks for correcting.

Good quarter but probably expectations were high. Stock sell off could be due to lack of pricing power in CP coke. China exports are again a factor. But China is also starting new aluminum smelting capacity, so exports could decline. Comments made that volumes and margins will be maintained. Should be ok if that comes true

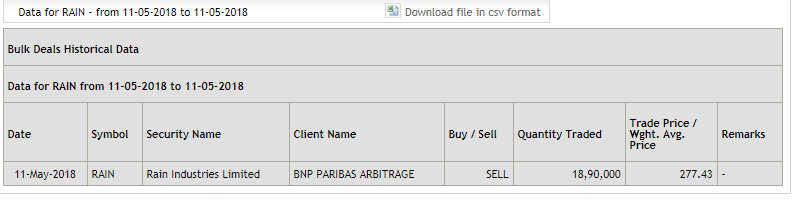

This Bnp Paribas fund entered recently only as it was not in shareholding pattern of Dec 2017. The fund manager did something similar in fortis healthcare. It bought fortis in feb end at 155 and sold in March end at 123. 123 was the bottom of Fortis stock. It seems the fund bought rain in first quarter of 2018 and sold today. It is an arbitrage fund with very poor returns in last 1 year.

3 Likes

Few points from the con call

-

Reduction in CPC volume: Due to the import duty hike by the govt of India and the lengthy negotiations. Unable to pass on the increased duty to customers which affected the margins.

But the demand for Aluminium in the US is expected to increase. So, the flow will increase to the US. Also, Gerard said a few times that their focus will be on the profitability rather than the

volume. Since the current CPC inventory level is high, they may reduce the production of CPC to reduce the raw material cost and cut inventory, also reducing the working capital.

In the meanwhile, still ironing out the recapture of import duties and trying to shape that up for the second quarter. Hopefully things will sort out. -

GPC Prices - GPC prices increased by more than 10%. But now since the CPC production is going to be reduced, GPC prices will also soften a little bit.

-

CPC prices - CPC price plateaued in Asia, but still rising in the US.

-

Loan repayment - No plans to repay any loan in the next 12 to 18 months. The cash available in the books will be used to fund the capex projects. Any future cash will be used for capex.

Don’t want to take debt for any new capex projects in the future. -

CPC Capex in vishakapatnam - Earlier (until Q1 con call) the plan was to start production in Vishakapatnam CPC plan from Q1 2019. But now it has been postponed to mid of Q3 2019.

That’s because of the delay in technology portion that we were supposed to receive from China. -

Other expenses - It increased significantly. It was majorly due to the products manufactured in Europe and sold in other parts of the world. Since the raw materials were bought in Euros

and sold in dollars/rupees, and since Euro is appreciating against dollar/rupee, losing some major amount there. Also, 2 to 3 plants were down for maintenance. And 2 to 3 million euro was

spent on that. That’s 25cr rupees.

-

Crude effect - Crude has no impact on the materials. Crude is not linked.

-

What’s good? Aluminium deficit or more aluminium production? The more aluminium produced the better it is for RAIN. Because it’s not linked to LME. It’s only linked to aluminium production.

-

Effective tax rate in FY2018: It’ll be 33 to 34%. It’s 200 to 250 basis points lesser than historical rate.

-

US Sanction on Rusal - Exposure is only 4% of the total revenue. No major impact if there will be change of ownership.

-

New capex announced for 66 million USD. That will be white-water resin. The production will start in FY2019.

To me, the results are good, though not the best. If other expenses were low, and no tax provisions made, numbers would have looked better than the last quarter. But maybe in the short term, the share price may be beaten down because of the bad sentiments that I sense over the net.

7 Likes

277.43 is weighted average price. So, there is a possibility that BNP Paribas started selling above 300, price started falling, kept selling, and kept selling more around 270, thereby bringing the weighted avg to 277.43.

1 Like