Quick heal is at very attractive level after 50% correction from top…interestingly its like fixed cost model…additional topline directly adds to bottomline…q4 is always good for the company…it will blast if they are able to scale up enterprise business…

Quick Heal going for buy back…

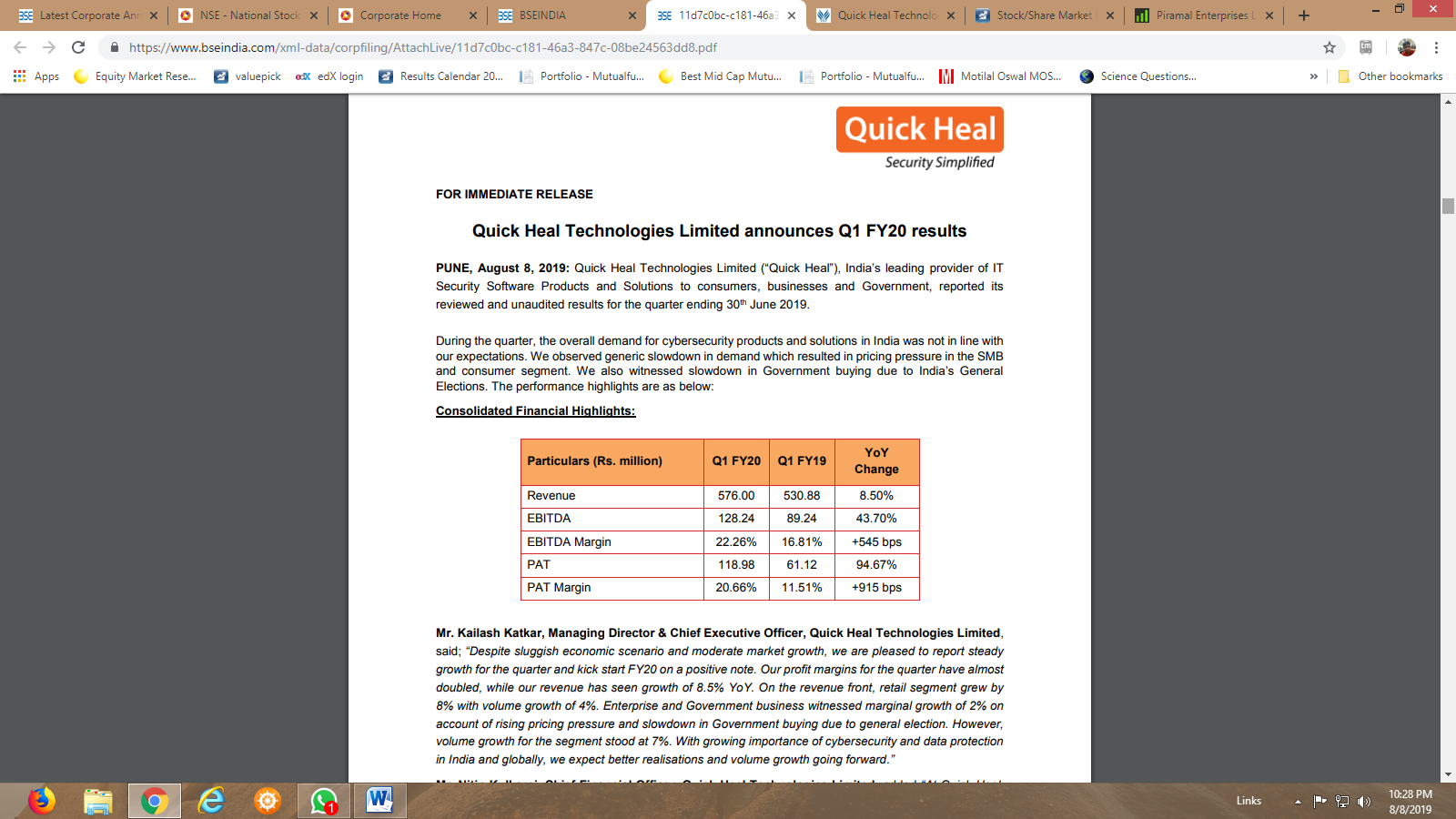

Quick heal promoter holding 72.33%, FY18 Topline 316Cr PAT 79Cr , 9MFY19 Topline 346Cr & PAT 103Cr,as of December 31, 2018, Quick Heal has cash

and cash equivalents along with investments and mutual fund, tax-free bonds and fixed deposit of

Rs.5,114.31 million as compared with Rs.4948.54 million at the end of September 2018, net

addition of Rs.166 million during the quarter. Cash balance includes IPO money of Rs.1,179

million, invested in fixed deposits.

Mcap FF 4162.3 million…buyback board meeting tomorrow…will closely watch if they are aggressive.

Sorry…9MFY19 Topline is 229cr & PAT 64Cr…

Very positive announcement…Buy back @275/- that too through tender offer…to spend Rs.175Cr to buyback 9% equity…

1 Like

Thanks for sharing - I could not easily find it on bseindia.com; Indeed it is great news - Fundamentally, I am still confused on potential of this company. It is operating in a space which has huge potential. At the same time, it competes with global players and hence subject to threats. Sales are very flat too in the recent couple of years.

1 Like

I have the same dilemma as you do! When I check on Linked in or Glassdoor I see some comments that are not so good both in content and form. I worry when someone who struggles to write passable English writes code that is expected to protect me from all evils out there !

From a technology standpoint, I have not fully assessed where QH is, but from some of the comments on GD and LI, it does not appear to be very cutting edge. I need to dig in more to come to any conclusions.

3 Likes

Promoters of Quick Heal are also participating in the buyback, no wonder why stock price has not reacted so much. I think they could have just done buyback from open market.

They would not go through regulatory approval without participating…their stake would go up to 79.5% if they won’t participate…regulator won’t approve promoter shareholding going up above 75%…

2 Likes

Thanks, I missed this point. They have to take money home to keep stake under 74%

Excellent analysis by Dr Vijay Malik. I learnt some useful info.

Some notable points that I learnt from this article.

- Rising receivable days.

- Lower R&D expenses in recent years, but that has been obfuscated in QH’s latest presentation by comparing 2019 R&D expenses with that of 2012.

- Pending tax litigation that may impact cash reserves, if decision is adverse.

Disclosure: invested.

4 Likes

Good show in gloomy economy…

Receivable down by 22 Cr…

Granted US Patent for Anti-Ransomware Technology by the United

States Patent and Trademark Office…

Retail segment revenue up at Rs. 457 million as compared to Rs. 423 million in the corresponding

period of the previous year…

Enterprise and Government segment revenue up at Rs. 146 million as compared to Rs. 144 million

in the corresponding period previous year(It was election quarter…soft govt. business).

1 Like

Is Quick Heal a Value Buy or a Value Trap?

- Price (12 June 2020) – 104 | Market Cap - Rs 666 Cr

- Operating Revenue - Rs 286 Cr | Total Revenue - Rs 317.6 Cr

- EBITDA - Rs 122.99 Cr | PAT - Rs 75.6 Cr

- Operating Cash Flow (OCF) - Rs 70 Cr | Free Cash Flow (FCF) - Rs 59.24 Cr | Cash + Investments - Rs 389.88 Cr

The Positives

- Valuations seems very attractive - Net of cash & investments, Quick Heal is available for Rs 276 Cr (as per current valuations) that translates into 4x current OCF; 4.6x current FCF and 3.3x EV / EBITDA

- Quick Heal is Debt Free

- COVID & increasing work from home options could potentially trigger demand for home based IT / network security solutions offering growth triggers

Concern Areas

- Sales are Stagnating – Operating Income - Rs 286 Cr in FY 2015 | Rs 315 Cr in FY 2019 | Rs 286 Cr in FY 2020 (can attribute a dip due to COVID, as per management Q4 always the strongest quarter, Q4 FY20 affected by COVID).

- Quick Heal’s Revenue Mix is Retail 79.21%; Enterprise 20.29%; Mobile 0.5%. IT / network / cyber security / protection solutions have moved online and instant as compared to Quick Heal that seems to depend on a distributor based stock & sell retail model. Industry has moved away from the physical retail model. Not sure what percentage of Quick Heal’s business is online?

- There is intense competition in IT / network / cyber security including from large global players. Delivery models are online, low priced or free solution, especially for retail. Prices are falling and it is shaping up to be a volume driven and low-margin business

- Management has been guiding on focusing on Enterprise solutions. Realisations are low in this segment and competition is also intense

- IT / cyber security solutions are pre-loaded and offered bundled as part of hardware / operating system especially for the retail category, Quick Heal does not seem to have any partnerships with hardware OEMs & operating system software majors

- Receivables going up year-on-year

Questions

- Online model is low cost, opex light and generates instant cash flow. Has Quick Heal been able to scale up the online model?

- Growth and sustainability of existing business also depends on recurring R&D investment. What is Quick Heal’s R&D strategy and in which areas? What is the effectiveness of Quick Heal’s R&D program?

- Can Quick Heal continue to generate Rs 60-70 Cr Free Cash year-on-year

- Quick Heal has made strategic investments of Rs 2 crore in Ray, a Singapore based start-up specializing in next generation networking and wireless technology, and Rs 2.1 crore in Israel-based cyber security startup L7 Defense. L7 Defense specializes in Next Generation Web Application Firewall (NG-WAF) and Application Program Interface (API) security to safeguard businesses against Botnet and distributed denial of service (DDoS) attacks. How does Quick Heal plan to utilize these partnerships to integrate Ray & L7 solutions within Quick Heal or integrate Quick Heal’s solutions within Ray & L7 and what are the potential upsides, if any from these investments?

Other Perspectives

- Quick Heal bought back 9% of the equity in July 2019 @ Rs 275

- Institutional holding in Quick Heal down from 8.14% in March 2018 to 2.34% in March 2020

- Sequoia Capital holds around 5% in Quick Heal

Though the opportunity is significant in IT / cyber & network security, overhang around stagnating sales; sustaining free cash flow generation; business model (stock & sell); lack of partnerships with OS & hardware OE majors, could potentially limit growth and Quick Heal could be a potential value trap

Happy to hear from other investors on their thoughts & perspectives (especially alternate views)

Disc: Evaluating investment

4 Likes

One of the key concerns that I understood while evaluating the company was the very high competitive intensity in the computer/mobile security software industry and presence of global giants (Symantec, AVAST, Kaspersky, Trend Micro, Sophos, etc.) - Please refer to pages 17-19 of the DRHP filed by the company as attached. Quick Heal - DRHP.pdf (5.6 MB)

Also, Microsoft has now integrated its security offering (Windows Defender) right into the operating system (beginning Windows 10), which means that for most non-enterprise users, there is no need to purchase security software separately. It is also highly rated by independent testing agencies such as AV-Test (Test antivirus software for Windows 10 - February 2022 | AV-TEST)

Based on the above, this space is not for me to invest!

Disc: Not invested

6 Likes

Any latest update on Quick heal.

Please share some insights or notes for analysis.

Hi, Is any one tracking it. The company has around Rs. 400 crore of cash. Importantly, they have announced buy back yesterday at Rs. 245 which is 30% more then the prevailing price yesterday (around 180, it already run up around 11% post announcement). As per announcement, proposal to buyback upto 63,26,530 Equity Shares of the Company, being 9.85% of the total paid up equity share capital of the Company.

Will promoter participate in buy back? As they own more than 72%, will they end up being biggest beneficiary? Any thoughts?

This is my understanding and I can be missing important points. It will be great if boarders can comment on same. Thanks in advance.

Disclaimer: Invested

1 Like

Finally, digitisation playing out in cyber security space…one of the best quarterly result…will have to watch next few quarters. MCAP 1012Cr Cash in hand 481 Cr. ROCE increased from 9.7% to 17.5% ROE increased from 10.4% to 15.3% Second buy back in 2 years 40% dividend…good management …all @ 11.4 PE…what is missing here??

2 Likes

Yes results looks very good. I am only concerned about litigation pending around service tax.

1 Like

Their enterprise arm seems to be growing and taking a large portion of revenue. They recently hired 2 senior talent from Cisco to run the enterprise arm.

Promoters keep doing buy back of shares without participating so they definitely are returning money back to shareholders.

Anyone here has any insights into their enterprise business? What are their products to enterprise. Are they cloud based and offered as SaaS like another cybersecurity start up from Pune does(Druva)?

I believe the enterprise arm of the company can certainly drive the company forward. Retail cybersecurity is pretty much dead, with inbuilt anti virus in Windows and Mac, no one needs an added antivirus, esp. when McAfee come pre installed for one year with every PC purchase.

3 Likes

Promoters are and have to participate in buy back…otherwise their holding will cross 75% limit…regarding free and paid antivirus softwares… Free Antivirus softwares are limited in the protection or security of a Windows PC. The paid versions of Antivirus softwares come with full features like Firewall, Spam protection, Ransomware protection, VPN, etc.

Proof in the pudding is their no. of retail subscribers and also competitor’s…this perception about antivirus software maybe giving poor valuation but any business that satisfy need of the customer will survive and thrive…just few days back Colonial pipeline paid $5M USD ransom to cyber attackers…

About their product info you can go through latest presentation…quick heal.pdf (4.2 MB)

DISCL. Holding miniscule…about 2% of portfolio.

1 Like