PTL Enterprises Ltd. (PTL), was incorporated as a company in 1959. It became an associate company of Apollo Tyres Ltd (ATL) in 1995, when Premier Tyres’ tyres and tubes manufacturing facility in Kalamassery, Kerala, was acquired by Apollo. This facility began commercial production in September 1962 and currently the plant is leased to Apollo tyres on long term basis. All production is done by Apollo Tyres. On a larger platform, PTL Enterprises is the holding company for Artemis Health Sciences.

–

PTL has a paid up capital of Rs 1324 lakhs, and is listed on National Stock Exchange, Cochin Stock Exchange and Bombay Stock Exchange. There are about 7000 shareholders of the Company.

PTL Enterprises is the holding company of Artemis Health Sciences Ltd. In 2007, a state-of-the art tertiary care hospital called Artemis Health Institute (AHI) was established in Gurgaon. The super specialities of AHI focus on Cardiovascular, Oncology, Orthopedics and Minimal Invasive Surgery in additional to others. Artemis offers to its patients, a technology-backed world –class healthcare delivered by leading medical professionals with certifications of international medical bodies.

Healthcare has become one of India`s largest sectors - both in terms of revenue and employment. The industry comprises hospitals, medical devices, clinical trials, outsourcing, telemedicine, medical tourism, health insurance and medical equipment. The Indian healthcare industry is growing at a tremendous pace due to its strengthening coverage, services and increasing expenditure by public as well private players.

.The share of healthcare is set to rise to 2.5 per cent of GDP in the 12th Plan from 0.9 per cent in the 11th Plan. The plan focuses on providing universal healthcare, strengthening healthcare infrastructure, promoting R&D and enacting strong regulation for the healthcare sector.

Company has two segments

For its tyre unit company get rental of around 40 crs year .

While business in subsidiaries is in hospital business which has around 300 beds & it has plan to raise capacity to 500 beds.

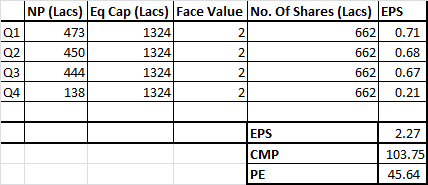

Consolidated sales of company has risen from 77 crs in 2009 to 410 crs in 2015 which is very encouraging . at the same time net profit of company has risen sharply from 2.1 crs in 2010 to 33.53 crs in 2015 on equity of 13.24 crs

Total debts of company is reduced from from 181 crs to 115 in last two years

Interest expn reduced sharply further in current year 2nd qtr from 2.25 crs to 1.21 crs which indicate debts reduced further in current year.

The Company had taken 20.78 acres of land on 90 years lease w.e.f. 24.05.2007 at a premium of Rs 519.50 lacs and the premium with other capitalized cost is amortized over a period of 90 years. Monthly lease rental, lighting expenses, water charges etc. are debited as revenue expenditure.

The Company has leased out its plant to Apollo Tyres Ltd. The lease is extended for a period of 8 years up to March 31,2022 vide agreement dated May 1,2012.The lease rent , which is renewable annually as per the lease agreement at a rate to be mutually agreed, amounting to Rs 4,000 Lacs for the year,

Average ROCE of last five year if around 21.5 % while company is distributing regular dividend of 50 % for last 5 years .

Tyre project of company is situated at land of 21.36 acres out of which govt of Kerla took 1.5 acre for Cochi metro project & offered company 24 crs which management has not accepted as fair value might be higher this amount onced realised likely to reduce debts further.

Average p/e ratio of healthcare hospitals is around 45, while at eps of 5 thus PTL enterprise is trading around 17, while current year estimated eps likely to be 6.5

Technically stock need to sustain above 92 levels for upmove

SBI MUTUAL fund hold around 409120 shares in its schemes as on November 2015 compared 364866 in the month as on Sept 2015

From this year lease will be 50 cr per year till 2022.

Valuation looks very cheap.

If anybody knows more please share.

Negatives-Not yet found.

Disclosure- Bought small tracking quantity.