@Mehnazfatima - Do you reckon the bullish technical setup is negated? or is it neutral at the moment. Do you still hold?

Thanks!

Niranjan

@Mehnazfatima - Do you reckon the bullish technical setup is negated? or is it neutral at the moment. Do you still hold?

Thanks!

Niranjan

Unfortunately, it is negated.

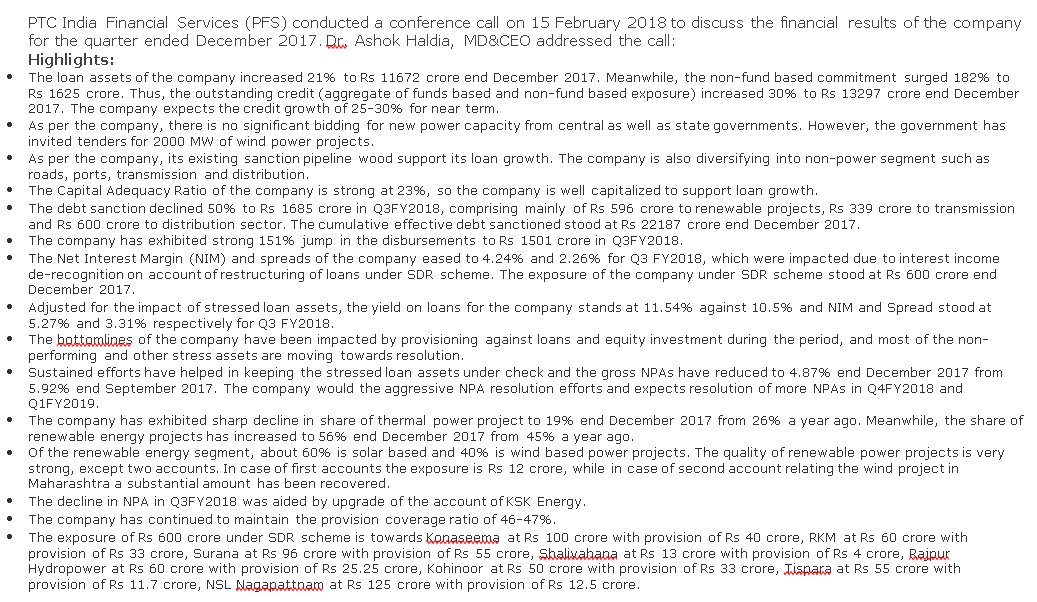

Attended the Q3FY18 Conference Call. Gauging from the number of people asking questions (only 3 folks) I’m tempted to say that the company is off the radar of Dalal Street or maybe the conference call scheduled at 2 pm (instead of the usual 4 pm) was not worth missing the joy of lunch.

Few highlights:

In my view the next 2 quarters are going to be important. The change in RBI norms is likely to lead to quicker resolution of problematic assets and so one will get a clearer picture of how much the book value of PFS is going to be depleted due to the NPAs soon. Once that Rs 1600 Crore (NPA + Restructured assets) overhang clears the valuation may see some shift.

Discl: Invested since IPO

JPrasun,

4.87% Gross NPA (of 11672 Cr) = 568 Cr. Restructured accounts per con call are 600 cr. So total stressed assets roughly 1200 cr. This number is not tallying up with the 1600 cr number you stated.

Also my 2 cents on the risk management of the company. They have roughly 5% of GNPAs and thermal are 19% of the total assets. I think in the beginning almost all of there assets were thermal. So assuming all GNPAs are thermal, roughly 25% of the projects they funded went bust. If this is true, then that is poor risk management. What is the guarantee that this may not repeat in renewable assets or the other avenues they are seeking like roads etc.?

Yes. If I remember correctly what was asked was how many crore of assets are not earning any interest for the company and the questioner himself totalled it up to Rs 1200 Crores but the Director, Dr. Pawan Singh, corrected that figure to about Rs 1600 Crores. I’m not really sure why additional Rs 400 Crore of assets are not generating any income, should have asked him then! It is possible that they are servicing the interest but there are lot of rules about income recognition such as meeting of commissioning deadline. It would be a good question to address to the company.

On the risk management aspect that you highlighted, I sort off agree with you. But you should also consider the state of the industry and the various issues that make this business inherently unattractive in comparison to say housing finance lending. I am equally concerned about their ability to assess projects and the fact that about 45% of their current assets are yet to start operations leaves lot of room for nasty surprises. Some of their equity investments have done very well and a few of them have gone entirely bust.

Having said that there are two reasons I am still holding on to the company (I could be dead wrong in my reasoning):

My plan is to watch the company over the next 2 quarters to see how their loan book shapes up. According to them some of the NPAs should reverse and some of the restructured assets will also get classified into standard assets. That should improve the ratios and hopefully the valuation.

any update on confirence call for Q4

Here’s the transcript.

PFS - Con Call - Q4FY18.pdf (295.9 KB)

The Management seems to be cognisant of the concerns and expects a turnaround in the business (NPAs) in couple of quarters. The stock price continues to poke holes in their confidence balloon.

Q4 & FY19 results don’t have much to be excited about. Full year PAT is Rs 184 Crores. GNPA stands at 6.04%, NNPA at 3.12%. Assets of Rs 13,321 Cr vs Rs 12,816 Cr as on 31/3/18. Yield on loans is at 9.96% and cost of funds is 8.61%.

The company now looks like a dullard. Growth has slowed down. Recovery of bad loans is happening slower than hoped. There isn’t much spread left.

Only saving grace is the valuation. Current P/E is 5, P/B is 0.5 and dividend yield is 5%. Unless the company shows growth in assets or recovery of bad loans I don’t think the stock price is going to go anywhere.

There is recovery taking place with company getting Rs 145 crore from Prayagraj Power Generation Company Ltd (PPGCL). mention of recovery of close to Rs 1000 Cr.

The stock has also moved up from the lows, but still does not seem expensive

In the article they have mentioned that around 1000 cr stressed asset they already addressed. Is it mean that only 600 Cr left to resolve(as total was aroun 1600 cr around 2018 time)?

Hope to see improvement in NPA number this quarter/financial year.

PTC india in the process of selling 65% stake in PFS. Valuation seems to be low on lower side. Generally what has been the P/B multiple for deals in the sector?

Have they announced any price for offloading the stake? The price should be atleast more than the company’s Networth.

Hi All,

Management is quite hopeful of resolution of good part of NPA though the promise is there for some time now. NIMs are improving and management is promising 15-20% increase in loan disbursement.

Another factor is planned divestment by PTC. Dont see much progress on that front on Google search. PTC may want to wait a bit for better valuation particularly as the business does not need immediate equity investment. Though most banks/NBFCs are not focused on retail, someone may see value in renewable franchise available at 0.6X book value.

The valuation is critically dependent on loss incurred on NPA. How do the boarders see the risk of increase of NPA and/or delay in NPA resolution.

Disclosure - Not invested. tracking closely.

I held this company for many years but sold off all my shares at a loss recently. Though the company is probably getting into better shape what I find infuriating is the company’s reluctance to not share NPA numbers upfront. They issue 3 or 4 page press reports but don’t write the GNPA, NNPA numbers!

Thanks @jprasun I agree. I found that they had different set of companies as NPA in 2015 -17 period and now which indicates that while there is some NPA resolution, the risk of new companies defaulting is still there.

I am tracking the company without initiating any investment yet.

Key takeaway from recent concall -

I would love to know views of fellow boarders.

Disclosure - Earlier interested in company primarily due to my interest in PTC India. Now considering buying the stock.

Resignation Letter Notice from 3 Independent Directors (bseindia.com)

There seems to be some major corporate governance issues in the company as alleged by the IDs in their resignation letters. This might stink like ILFS. Investors in this company do note this development.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=cee3e539-b448-4b00-bc4c-5dff3945df62 Reschedulement Of The Board Meeting Scheduled To Be Held On 08Th April, 2022

Bad corporate governance is continuing at PTC India Finance as at 5 PM on the day of Board meeting we learn that the meeting is rescheduled without giving any reason for rescheduling the meeting and giving next date for Board meeting.

Disclosure - invested in PTC India so views are biased.