It was indeed an inside bar.

Conf call going on now i guess.Anybody attending?

It was indeed an inside bar.

Conf call going on now i guess.Anybody attending?

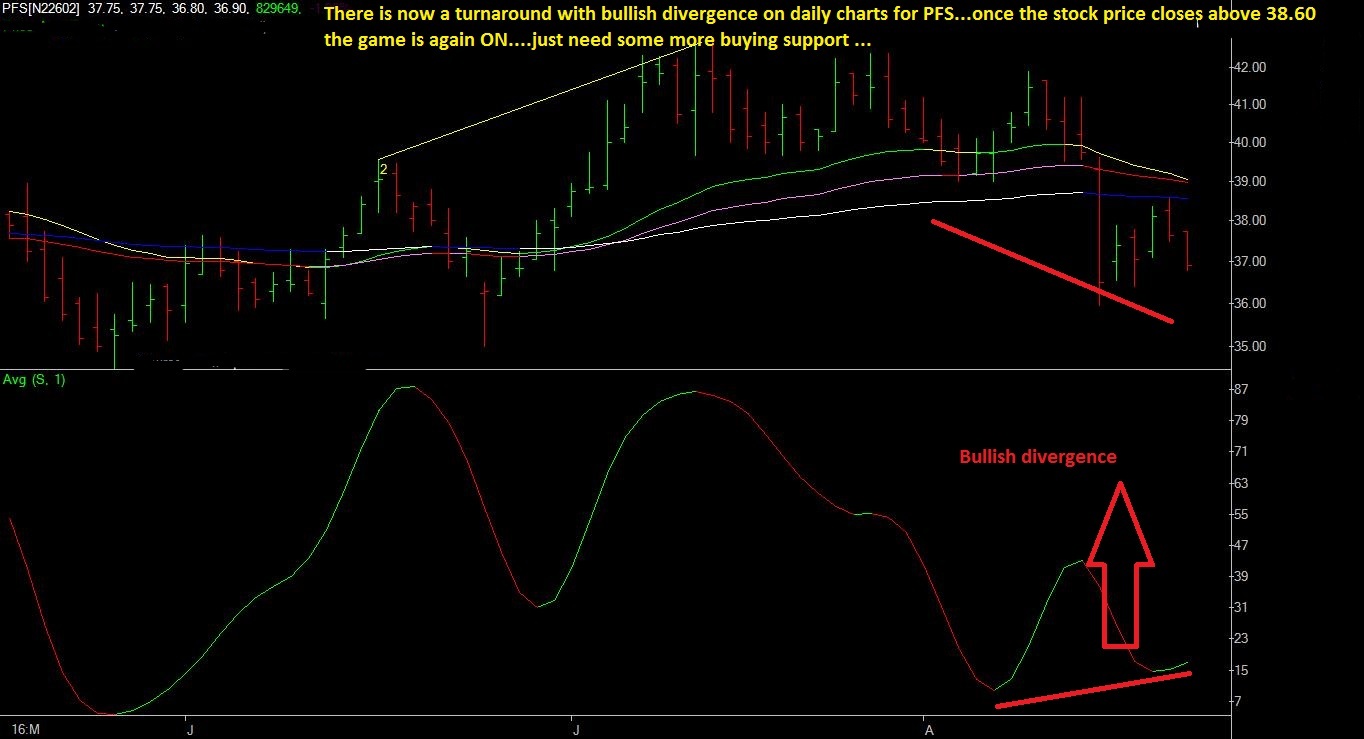

Would advise the investors to buy PFs only on close above 38.60…

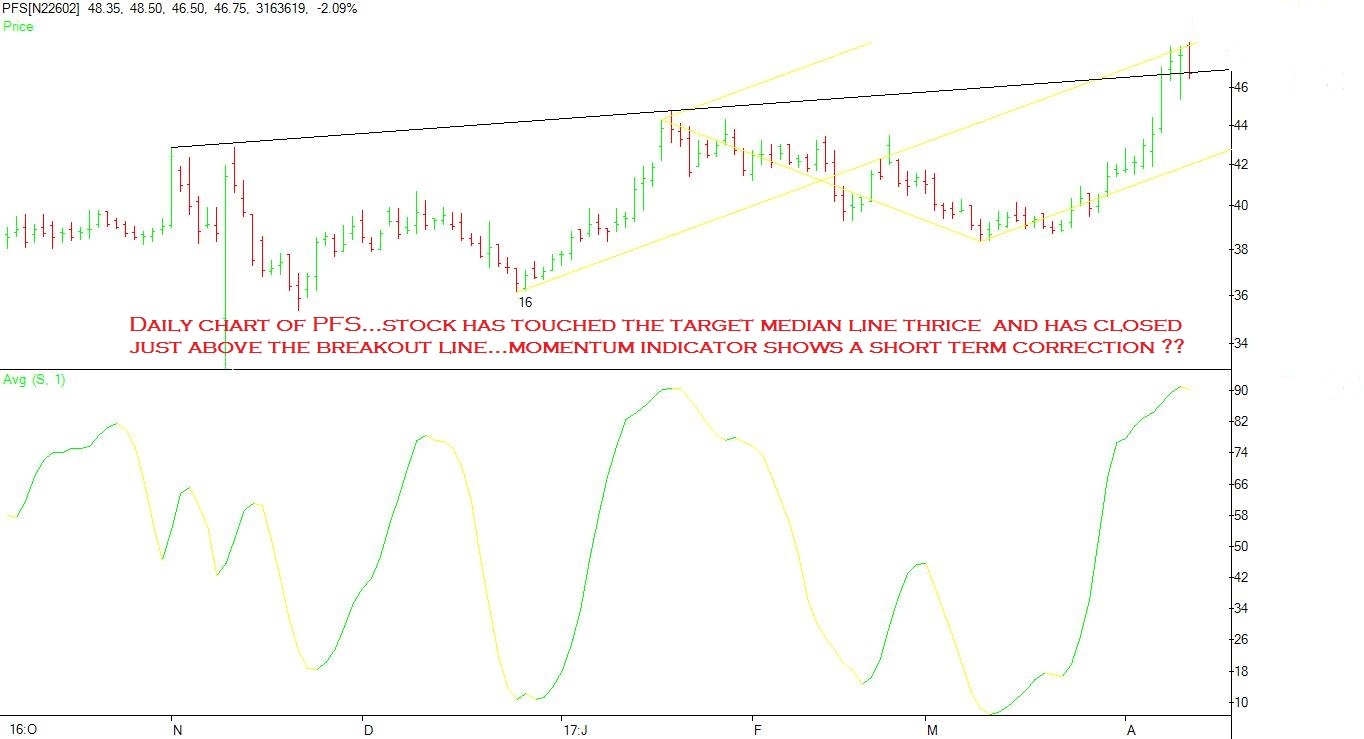

Multiple resistance from 38-42. Any fresh entry should be made only above 42 break of which will lead to immediate targets of 50-52. As of now…it is looking bearish and all set to do 35.

Hi Valuepickr Boarders,

I tried comparing the profits of PFS which are increasing on yoy basis(obviously eps as well  )…with operating cashflows which are decreasing yoy which is giving me a different view.

)…with operating cashflows which are decreasing yoy which is giving me a different view.

For the past 10 years(from 2007…was using screener.in) cash from operations was never positive and the cash from financials was always positive.

Is it like all the dividends which company was increasing yoy is not funded by operations

Tried to check with L&T financial holdings (as i see this company has started increasing its portfolio in renewable energy…agree that its more diversified than PFS) even here as well its the same case -ve operating cash flows and +ve financial cashflows…

Am i missing something …or should i be evaluating NBFCs in a different way…

Appreciate your views…

thanks in advance

Disc:invested<3% of portfolio and planning to increase based on further evaluation.

Hi Madhu,

You’ll have to think differently for financial companies.

These companies give cash (lend) to their borrowers and that is their core operation. They usually give out more and more cash each year (as their lending book grows). They earn interest on it but that is a small percentage of the loan given (what is usually called the yield on loan assets). Hence the cash from operations will be negative.

To give out cash they need to either have it or they need raise funds. This they do by either ploughing back profits or by raising additional debt or equity. If the company raises funds by issuing debt or equity then that gets classified as cash from financing. Thus cash from financing will be positive. For the debt it raises it pays an interest (what is basically known as cost of funds). And basically, these specialised finance companies live off the difference between the interest paid and interest received.

PFS gives out dividends from the net interest it earns on its loans. Many companies do give out dividends from capital raised but that doesn’t seem the case with PFS yet.

PFS recently raised additional equity by issuing shares to its parent company. In FY17 annual report, this will be seen as cash from financing.

Hope this helps.

@Mehnazfatima ji your technical views regarding PFS at current levels. Would really appreciate your read on it.

There is a breakout in PFS today…it has one more resistance @ 42.15…once the stock closes above this level, then we can see an uptrend in PFS…todays breakout is supported by the fundamental news with regards to stake sale, as per the declaration filed by the company. We can expect a good jump in the eps for Q4…

PFS is now positive on all time frames…quarterly, monthly,weekly and daily…I think that makes it a good time and price to buy PFS for investment purpose. The emphasis of Modi sarkar on renewable energy (PFS is dominant in renewable financing)is an added bonus…

Those interested in long term, may have a look at the quarterly chart of PFS with Andrews Picthfork and Momentum indicator showing a turnaround…

The macro case for PFS is as follows…

Modi sarkar has a renewable target of around 60000mw for wind and 60000mw for solar power by 2022…

If we take 5crores per mw as the base price, then the investment required is more than 3 lakh crores by 2022…

And PFS is a dominant player in renewable finance…and also has an advantage that renewable power supplied through auction is to be purchased by its parent PTC…

HENCE the growth potential is humoungous…makes PFS a good long term holding…very bullish technicals is an added bonus.

Any growth story will eventually run into problems…i think the same will happen to renewable theme after 3-5 years…

Till then enjoy the fruits of this growth by investing in PFS…after that we jump ship…and scout for new story…

I think we are in the first stage…where invedtors are looking only at the problems in renewable power and are not looking at the growth prospects…therefore, this is the ideal time to buy PFS…after a few years, they will look only at the prospects but not at new problems…hence that would be te time to exit from PFS

DISCLOSURE…invested in PFS.

Does this apply too all loans it disburses? Then why there are 1000 cr NPAs on its books at the moment? This is a huge number and mgmt seems like downplaying it.

Curious where did you get 1000 cr NPA number for PFS? Share Khan Research report of Nov 2016

reports GNPA around 402cr and NNPA at 26.5cr.

Appreciate if you can provide the link for 1000 cr NPA.

Disc: Not invested

Pfs has risen by 20% in a short period of time. On long term charts, it’s in an uptrend. But short term charts seem to suggest an small correction within the uptrend.

Is PTC India financial services Government comapny?

Lot of progress happening in this space, interesting time ahead.

Solar Power may become cheaper than Coal power in India

India adds 5,525 MW Solar power in FY’16-17, taking total to 12,288 MW

Positive triggers for PFS

1.PFS gets around 50% of its funds from banks …borrowing at prevailing mclr rates. Due to demonetoization, the mclr has fallen by 60-70 bps and thus consequently the cost of funds of PFS has fallen quite drastically. As the mngt says PFS has been a beneficiary of the demonetization process and the positive effect will be seen moderately in Q4 and fully in Q1 fy 2018.

Renewables now account for around 50% of the topline. Since PFS has stopped loans for new thermal power projects, the renewables percentage will rise to around 60-65% byQ2 fy2018. Lending to renewables has the added attraction that on completed projects they CAR required is just 50%. Thus they get to earn twice the amount of earnings in lesser time from the same capital…than they would by lending to non renewables sector.

in the next few quarters, the following problem projects whereby PFS had made around 50% provisioning will be resolved and the profitability of PFS will be strengthened to that extent.

a) Surana Power…under talks for sale to the adjoining thermal power plant owner _KSCL …to be completed by end of Q2

b) Konasema…Gail has agreed to provide gas from ONGC and the taking over is under process

c) ikon…PFS had an exclusive charge on land…and SBICAPS has been appointed to find a buyer…land valued at 35 crores…full amunt due is expected to be recovered by PFS

d) Shalivahana…the power plant is up and running and the monthly billing is getting settled. The outstanding amounts will be cleared by Q1

e)Kohinoor…takeover talks with new investor in advanced stage…maybe 1 -2 quarters the sale will be completed

f) Rajpur…permission to take over the project already obtained from himachal Govt and now SBICAPS is in the process of finding a new buyer…

g) Wind project in Maharashtra…project is running and supplying to the grid…only PPA was not signed…now the Govt of Maharashtra has decided to sign PPAs and only a few procedural undertakings have to be signed by the promoter…almost as good as completed.

I think these multiple triggers is causing the stock to be rerated and the stock is already in uptrend…it may keep going up as the eps gets better and better…the worst may now be behind PFS…

Now we have all the main ingredients which make PFS a good investment

Sectoral tailwinds

near term and medium term triggers

very good technicals,bullish on long and medium term charts

good Mngt

strong balance sheet …26% capital adequay ratio

good presence in a niche area (renewables)

Q1) Does anyone know when Q4 numbers will be out?

Q2) What is the impact of lower cost of production (now Rs 2.62 per unit from Rs 4.6 last year) on PFS?

Based on past experience, one shouldn’t expect the company to declare their results until May end or early June.

Mr. Haldia was asked about the Rewa tariffs (similar to these) in their last results’ con-call. According to him, PFS would be very cautious when looking to fund these projects. They are well aware of the risks involved and the wafer thin margins at such prices. Having said that, for these projects a lot of things are provided for/assured by the government. For eg. land, power transmission & evacuation facilities etc. So the risks are marginally lower.

Due to these rock bottom tariffs there could be some risk to current PPAs signed at much higher prices. There have been instances of long term PPAs being scrapped. That’s a regulatory risk.

Board meeting on 22nd May to record the results and announce the dividend if any