ofcourse you can say its applicable for ceramic companies like cera where people going to letrin will be same. But that industry is consolidated and only few are dominant leaders. The ceramic industry is not unorganized.

1 Like

ofcourse it will. when economic activity picks up, the pyramid of consumers get an absolute upliftment. people who today sit on ground would aspire for furniture and people who buy cheapest chairs would aspire for brands. its the normal process and now in this plastic industry there’s a lot of scope to take away the pie from unorganized player. if you think housing would boom then everything related to that has to boom. also the cermic industry is highly fragmented and along with it anything to do with housing is highly fragmented be it bricks, cement, plywood, tiles, etc.

A 20% UC today… three days back icici direct released their research report on prima -> http://www.moneycontrol.com/mccode/news/article/article_pdf.php?autono=1323946&num=0

looks like its getting into lime light now.

Another 20% UC today and this time on even higher volumes. It’s just a matter of time that the 52 weeks high is taken out.

Today created a new lifetime high for itself on strong delivery volumes.

Hi,

We have been studying this company for a while now. Their JV @ Cameroon is doing very well and hence financials of Prima look attractive. Below are some of the points we could gather on Prima -

Promoter - Dilip Parekh is nephew of Nilkamal’s promoters

JV in Cameroon (Prima Dee-Lite Plastics Pvt) - JV partner was erstwhile dealer of company in South Africa. That dealer convinced Dilip to set up a local unit as market was attractive and there were some benefits of tax savings, which continue to happen till today.

- Prima sells moulded furniture and woven sacks through this JV in Cameroon

- Investment in JV - 1cr equity and 11cr in debt with recourse to Prima (debt is fully repaid now)

- JV has been able to maintain EBITDA margins of ~33%, five years back they were ~37%

- Management says there is not much competition in Cameroon so far

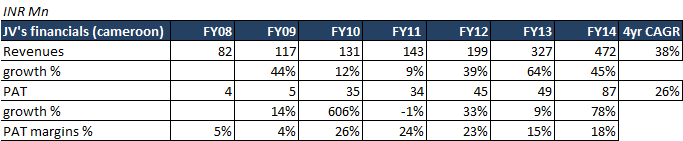

below is an yearly snapshot of financials of JV -

For 9 months FY15, JV has done sales of 60Cr. On an annualized basis it converts into growth of 70% over FY14.

India business – current op margins of 6-7%

o Margins are expected to increase up to ~12% after hiving off its ACP division and also to benefit from low crude prices flowing into COGS

- Good presence into Kerala, Daman, Puunjab, Hyderabad

Revenue mix for last 9 years -

Impact of falling crude prices - there might be some inventory write off in Q4’15

Tax rates - Prima will have to pay MAT in India and will keep on getting 50% concession in Cameroon (for next 4 years perhaps)

Future plans/outlook -

- Prima intends to enter Latin America on similar lines as Cameroon

- Focus is on exports and foreign operations. Domestic sales will keep on growing ~10%

Growth triggers -

- High growth JV operations in Cameroon

- Entry into newer geographies such as Latin America

Below is what I like and what I do not like about the company -

Positives -

- Closing down of ACP division speaks good of management. This should lead to better profitability and return metrics

- Improving profile of business on the back of better revenue mix in favour of JV and export sales sounds good.

- Strong balance sheet -net D/E at ~0.2x

Negatives -

- JV operations are earning super normal profits in such a commodity business. Their sustainability will be threatened once new competitors come

- Net working capital is very high at 5 months, over last 9 years company has been able to convert only ~80% of its profits into cash. Receivables are poor in domestic markets, while in foreign markets company operates on average receivables of ~15 days. On suppliers side, company does not have any bargaining power to get good credit days. Its suppliers include Reliance, Indian Oil besides some local ones.

- related party transactions with promoters’ entity is discomforting

- No hedging strategy in place, all forex exposure is left open

Few open questions -

- What is leading to high growth and high profits for Prima in Cameroon. Why is new competition not coming up

- Need to understand its LatAm plans in detail

Look forward to your views.

Thanks

rajat

7 Likes

first of all a very good summary writeup. let me just give my thoughts on your concerns and open questions:

- Yes, and this is expected to continue in the near future. They are making a lot of money because a. they have economies of scale 2. limited competition. c. a very strong understanding of this business in general. The competition is there, but not at the scale of Prima. There are numerous small sized competitors but they dont have the financial muscle to grow. One of the reasons Prima has done well is because its JV partner is a well connected guy. Ofcourse the competition would come but not immediately (as on date). Also, this risk is slightly mitigated by their plan to enter newer geogrophies. The PAT margins are expected to be around 13-15% in the long run, which i think is very good.

- yes you are right but it should improve moving forward. Also, noone of the plastic furniture companies have any bargaining power to get decent credit days, even wim plast doesnt.

- yes, but what i know of promoters - this, hopefully should not be an issue.

- I agree, now that they are growing so big, its important to think about hedging as it would give predictability.

by the way, how did you get the JV’s earnings for FY15? is 60cr for 9month or 12 month as their FY ends in Dec.

1 Like

Thanks @j2eeprofession_

JV earnings - this is for 9 months ending Dec’14. This is as per promoters.

Could you please tell us more about the promoters which gives you comfort around RPTs?

Thanks

Rajat

9 months earnings should be sep end not dec 14 end as dec 14 would mean the entire year for the JV since it follows Jan-Dec FY… i do not think its correct information.

Since there was no explicit mention of time period I will not say anything firmly but I interpreted it to be till Dec.

ahh, in that case its very difficult to take a call on the performance of the subsidiary just as yet

“Prima Plastics Ltd has now informed BSE that the Meeting of the Board of

Directors will be held on May 29, 2015, also to consider & Approve

project to set up a moulded furniture project at Nicaragua (Central

America).”

The above BSE announcement is encouraging for the medium term.

Prima Plastics is again in upper circuit.

let’s hope that tomorrow it closes above 72-73 levels after touching a new high, then it will be a major breakout.

prima has confirmed the breakout and now huge upside opens up… in the next couple of yrs one could easily strong upsides in next couple of yes

profitability in their JV declined sharply as per my calculations. JV posted a growth of ~35% and PAT is almost flat. Company does not report this number, i’ve done my own calculation so i might be wrong.

Major puzzle for me is how can they sustain such high profitability (18%+ PAT margins).

Though its expansion plans in Cameroon and Nicargua bodes well for future growth.

the last time their JV company suffered very heavy inventory losses and therefore, it bought down the profitability. 10-15% volatility in crude in a month is still manageable but 50% decline in a couple of months is way too much for any company. Anyways, i am told that it was a one off event as no such sudden volatility is expected (even by those to track crude)… lets see now. market clearly knows something here as this breakout should lead to a very fast price appreciation

Excellent Numbers by the company -> http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/730AA4CD_DC57_4FC2_9E26_6765EB0EF6A3_194354.pdf

Closure of ACP unit now kicking up the bottomline as it doubles YoY.

Thanks for the update. Closer look at YOY segment comparison…figs rounded and in lakhs

PMF segment revenue 1911 vs 1716, (11%) while PBT 136 vs 115 (18%)

ACP segment revenue 18 vs 202, (-91%) while PBT (-16) vs (-45) (-64%)

Interest and Finance Charges 8.2 vs 35.6 (-77%)

PBT 127 vs 60 (112%)

PMF Returns on PBT 3.4% vs 3.55% (-15 bps)

ACP Returns on PBT (-3.2%) vs (-4.94%) (-174 bps)

While PBT has almost more than doubled YOY, most of that is due to lower losses in ACP unit and lower interest cost while growth in PMF is only marginal. Even return ratios in PMF are yet not so encouraging. How sustainable is this growth going forward and is it profitable?

Profit margins in PMF are very weak given how much margin expansion Nilkamal had during the quarter. For Nilkamal EBIT margins in the Plastics division increase from 6.2% to 11.7% on account of benefit from decline in crude prices. So either Prima is taking cash out or we can give them benefit of doubt and expect them to show the margin expansion in the next quarter.